Permian gas-pipeline debottlenecking advancing at full speed

Key Highlights

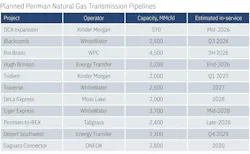

- Major pipeline projects like Hugh Brinson and Blackcomb are expected to add over 4 bcfd of capacity by late 2026.

- Operators such as Diamondback Energy are diversifying strategies by securing long-haul commitments and integrating gas demand into power projects.

- Growing Gulf Coast LNG demand and rising domestic production continue to pressure Permian egress, maintaining oversupply conditions.

- Several pipeline projects, including Traverse and Rio Bravo, are progressing towards service, but legal and environmental hurdles remain.

Permian basin associated natural gas production continues to outpace takeaway capacity, with regional gas oversupply forcing Waha hub prices into negative territory for 118 of the first 131 days of 2026.

Projects including the WhiteWater-led Blackcomb and Energy Transfer’s Hugh Brinson pipelines, are expected to add more than 5.25 bcfd of capacity by late 2026. In the meantime, however, upstream operators are adapting commercial strategies to existing constraints.

Diamondback Energy Inc., for instance, said it intends to reduce exposure to Waha pricing by securing additional long-haul transportation commitments and integrating gas demand into power-generation projects and expects its gas takeaway capacity to more than double by late 2026.

Growing demand from Gulf Coast LNG projects will continue to pressure Permian pipeline capacity from the demand side, while the US Energy Information Administration expects domestic gas production to continue rising through 2026-27, driven heavily by the Permian.

With both supply and demand surging, the Permian gas market is likely to remain oversupplied and infrastructure-constrained until later this year.

What follows are the current statuses of Permian-focused natural gas pipeline projects.

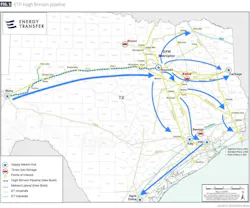

Hugh Brinson

Energy Transfer LP in December 2024 took final investment decision on its bidirectional 2.2-bcfd Hugh Brinson natural gas pipeline. The 400-mile, 42-in. OD pipeline will connect Permian basin production to multiple markets, with the company expecting initial in-service by end-2026.

Construction is occurring in two phases, with Hugh Brinson’s 1.5-bcfd Phase 1 delivering gas from the Waha hub to Maypearl, Tex., south of Dallas-Fort Worth, by that end-2026 target. Phase 1 will also include the 42-mile, 36-in. OD Midland Lateral, connecting Energy Transfer and third-party processing plants in Martin and Midland Counties to the pipeline (Fig. 1).

Phase 2 will add compression to bring capacity to the total 2.2 bcfd and could be done concurrently with Phase 1 if market conditions warrant. The majority of the project’s steel was rolled in US pipe mills, mitigating any potential tariff impacts. Overall expected project cost is $2.7 billion. Energy Transfer is explicitly targeting increased gas-fired power generation driven by anticipated data-center demand in pursuing the project, though that wasn’t the case when it was first proposed as Warrior.

As of February 2026, 100% of the project’s pipe had been delivered to pipe yards and mainline construction was roughly 75% complete, with Phase I still expected to enter service fourth-quarter 2026. Energy Transfer was also positioning the pipeline as a major US header system, enabling improved flows to the Desert Southwest, South Florida, the Midwest, and all points in between, while touting its 230 bcf of storage.

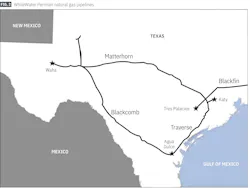

Traverse

Enbridge and its partners in the planned bidirectional 36-in. OD Traverse pipeline—connecting the Katy hub to the Agua Dulce hub in South Texas—in August 2025 increased its capacity to 2.5 bcfd from 1.75 bcfd. Traverse is owned by the Blackcomb pipeline jv: WPC (70%), Targa Resources Corp. (17.5%), and MPLX (12.5%). The WPC jv is owned by WhiteWater (50.6%), MPLX (30.4%), and Enbridge (19%). WhiteWater’s stake is owned by I Squared Capital.

WhiteWater is building and will operate Traverse, which will carry gas from interconnections with WPC’s Whistler and Blackcomb pipelines and the WhiteWater-operated Matterhorn Express pipeline, effectively completing a loop between Permian basin production, South Texas, and Houston-Louisiana destinations (Fig. 2), including Venture Global Inc.’s 20-million tpy CP2 LNG plant in Cameron Parish, La. WhiteWater expects the pipeline to enter service in 2027.

Transport between the Houston area and Louisiana would be provided by WhiteWater’s 3.5-bcfd Blackfin pipeline.

Blackcomb

Blackcomb is a 366-mile pipeline designed to transport 2.5 bcfd from the Permian basin to Agua Dulce. An 80-mile, 42-in. OD line will connect Midland basin gas processors to the line, contributing to debottlenecking Permian-area shipping.

WPC began work on the pipeline in 2024, targeting a third-quarter 2026 in-service date. Diamondback, Marathon Petroleum Corp., Devon Energy Corp., and Targa Resources Corp. each have contracted space on Blackcomb.

Rio Bravo

WPC expects its 4.5-bcfd Rio Bravo pipeline to enter service second-half 2026, carrying gas from Agua Dulce to NextDecade Corp.’s planned 27-million tpy Rio Grande LNG plant in Brownsville, Tex.

The project received its final supplemental environmental impact statement from US Federal Energy Regulatory Commission (FERC) in August 2025. Four months later, the City of Port Isabel and a coalition of environmental groups sued FERC for approving the pipeline.

DeLa Express

DeLa Express LLC, a subsidiary of Moss Lake Partners LP, last year let a front-end engineering and design (FEED) contract to Wood to build the 2-bcfd DeLa Express pipeline from the Permian basin to the US Gulf Coast. The pipeline will run 645 miles of 42-in. OD pipe from Winkler County, Tex., to a gas plant in Calcasieu Parish, La., connecting to six laterals along the way supplying markets ranging from Port Arthur, Tex., to Cameron Parish, La., including LNG plants, fractionators, and Moss Lake’s NGL export project, Hackberry NGL.

Moss Lake expects the pipeline to enter service in 2028 and was conducting community outreach for the project third-quarter 2025.

Saguaro Connector

FERC in 2024 granted ONEOK Inc. a Presidential Permit to build and operate the Saguaro Connector natural gas pipeline border crossing into Mexico from Hudspeth County, Tex. The proposed 2.8-bcfd Saguaro Connector pipeline would use 155 miles of 48-in. pipe to transport Permian basin gas carried by ONEOK’s existing 777-MMcfd WesTex intrastate pipeline and other sources to Mexico. A pipeline on the Mexican side of the border would carry the gas to the country’s west coast for liquefaction and export.

The pipeline has since been mired in legal proceedings surrounding claims that FERC had improperly limited the scope of its analysis when granting the permit. ONEOK on Apr. 1, 2026, requested a 3-year extension from FERC—to Feb. 15, 2030—to put the project’s 1,000-ft border crossing segment into service. The company said that construction had not yet begun due to a combination of the litigation and delays in construction of the 15-million tonne/year (tpy) Saguaro Energia LNG plant being developed in Puerto Libertad by Mexico Pacific Ltd. LLC.

Gulf Coast Express expansion

Phillips 66 in 2024 agreed to sell DCP GCX Pipeline LLC, owner of a 25% stake in the Gulf Coast Express pipeline, to an affiliate of ArcLight Capital Partners LLC (OGJ Online, Dec. 16, 2024). The pipeline can deliver 2 bcfd of gas from Waha to South Texas liquefaction markets.

Operator Kinder Morgan Inc.’s (KMI) 570-MMcfd expansion of the pipeline, targeting a mid-2026 in-service date, was “on track” according to the company’s first-quarter 2026 earnings call.

Trident Intrastate

KMI is at the same time continuing construction of its 2-bcfd Trident Intrastate Pipeline, including pipe stringing and mainline welding activities across multiple counties in Texas, describing it as “on track” as well. The 219-mile line will begin west of Katy and run north to the Huntsville, Tex., area before turning southeast and reaching its terminus near Port Arthur.

Plans include delivery points in Grimes, San Jacinto, Liberty, Hardin, and Jefferson counties, Tex. Both Entergy Texas, a subsidiary of Entergy Corp., and ExxonMobil-QatarEnergy’s 18-million tpy Golden Pass LNG plant in Port Arthur, will receive shipments via Trident. Entergy will use the gas for power generation.

KMI expects to place the first phase in service first-quarter 2027, with the second phase following in fourth-quarter 2028, pending regulatory approvals. Trident is expandable up to 2.8 bcfd, according to the company.

Permian-to-REX

Tallgrass Energy Partners in May 2025 executed anchor shipper precedent agreements for a new 2.4-bcfd pipeline to deliver from multiple points in the Permian basin to the 4-bcfd Rockies Express Pipeline (REX) and other destinations. The pipeline has a target in-service date of late 2028.

The company launched an open season on July 21, 2025, recasting the project as Energy Resiliency and Affordability Upgrade LLC (Transporter). Tallgrass said that Transporter was offering firm natural gas transportation service from various receipt points in the Permian basin, including in and around Waha, Tex., to destination points along a pipeline path extending to one or more points of interconnection with REX, including a proposed delivery point to REX’s Zone 2 between the Cheyenne Hub in southeast Wyoming and the Mexico Compressor Station in northern Missouri.

Desert Southwest

Energy Transfer LP in August 2025 sanctioned a 1.5 bcfd expansion of its Transwestern Pipeline. As announced, Transwestern’s Desert Southwest Pipeline expansion included a 516-mile, 42-in. OD natural gas pipeline connecting the Permian basin with markets in Arizona, New Mexico, and Texas. It is expected to be in service by fourth-quarter 2029.

The $5.3-billion project is supported by long-term commitments, and an open season held later in third-quarter 2025 drew sufficient interest that in December 2025 Energy Transfer announced it had upsized the pipeline’s mainline diameter to 48 in., increasing its capacity to 2.3 bcfd.

Eiger Express

WhiteWater Midstream will expand the capacity of its planned 2.5-bcfd Eiger Express natural gas pipeline to 3.7 bcfd, having secured sufficient firm transportation agreements to do so. The expansion will be executed by increasing the pipeline’s OD to 48 in. from 42 in. and adding incremental compression.

Eiger Express will transport gas from the Permian basin to a hub near Katy, Tex., just west of Houston, following the right-of-way established by the 2.5-bcfd Matterhorn pipeline, which began commercial operations in October 2024.

WhiteWater announced the 450-mile Eiger Express in late August 2025 and expects to place it in service mid-2028. The pipeline is owned by a joint venture among the Matterhorn jv (70%), ONEOK Inc. (15%), and MPLX LP (15%). The Matterhorn jv is owned by WhiteWater (65%), ONEOK (15%), MPLX (10%), and Enbridge Inc. (10%).

About the Author

Christopher E. Smith

Editor in Chief

Chris joined Oil & Gas Journal in 2005 as Pipeline Editor, having already worked for more than a decade in a variety of oil and gas industry analysis and reporting roles. He became editor-in-chief in 2019 and head of content in 2025.