US pipeline operators sink revenue growth into expansion

US pipeline operators used rising revenues to grow their systems and expanded plans for future growth. Oil pipeline operators' revenues surged in 2012, allowing carriers to aggressively expand their property while at the same time pocketing record profits. Natural gas pipeline operators, meanwhile, saw net income slide despite increased revenue, but greatly increased their construction plans.

The growth in planned construction reversed a 3-year trend in which planned mileage contracted each year and reflects the renewed confidence in the domestic US oil and gas sector. The resulting increased demand for the resources necessary to build pipelines, however, caused construction costs to increase. Labor remained the most expensive component, but material costs nearly doubled.

Details

Oil pipeline operators' net income continued to rise, reaching an all-time high of $6.4 billion, a 5.1% increase from 2011. The higher profits came on the back of even larger increases in oil pipeline revenues, which rose 11.5%. The resulting earnings as a percent of revenue eased from the record levels seen in 2011 to 45.86%. The disparity between income and revenue coincided with a nearly $3-billion jump in changes to carrier property, as companies began aggressively expanding their infrastructures.

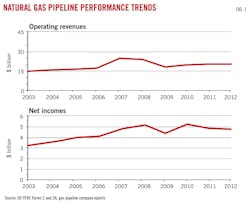

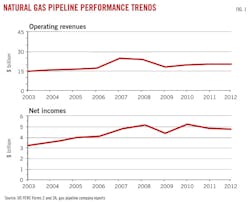

Natural gas pipeline operators meanwhile saw their profits continue to shrink, falling 2.5% to $4.76 billion, the lowest level since 2009 despite revenues rising 2.1%. (Fig. 1).

Proposed new-build mileage rose more than five and half times from 2011's announced build, while planned horsepower additions of 450,147 were 244.11% of 2011's total.

The spike in anticipated demand saw overall estimated $/mile land pipeline construction costs rise more than $1 million (32%) to $4.1 million. Pipeline labor prices remained the single most expensive per-mile item at $1.6 million/mile, but the biggest single increase was seen in material costs, which nearly doubled to $952,328/mile.

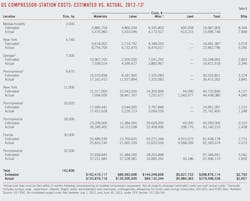

Estimated land pipeline construction costs for projects completed in the 12 months ending June 30, 2013, were nearly $600,000/mile higher than actual costs, more than $400,000/mile of which came from inflated miscellaneous cost estimates. Actual compressor station costs were 5.1% less than estimated costs for projects completed by June 30, 2013, with significantly smaller miscellaneous costs here as well cancelling out much higher than anticipated labor costs.

US pipeline data

At the end of this article, two large tables (beginning on p. 126) offer a variety of data for US oil and gas pipeline companies: revenue, income, volumes transported, miles operated, and investments in physical plants. These data are gathered from annual reports filed with FERC by regulated oil and natural gas pipeline companies for the previous calendar year.

Data is also gathered from periodic filings with FERC by those regulated natural gas pipeline companies seeking FERC approval to expand capacity. OGJ keeps a record of these filings for each 12-month period ending June 30.

Combined, these data allow an analysis of the US regulated interstate pipeline system.

• Annual reports. Companies that, in FERC's determination, are involved in the interstate movement of oil or natural gas for a fee are jurisdictional to FERC, must apply to FERC for approval of transportation rates, and therefore must file a FERC annual report: Form 2 or 2A, respectively, for major or nonmajor natural gas pipelines; Form 6 for oil (crude or product) pipelines.

The distinction between "major" and "nonmajor" is defined by FERC and appears as a note at the end of the table listing all FERC-regulated natural gas pipeline companies for 2012 at the end of this article.

The deadline to file these reports each year is April 1. For a variety of reasons, a number of companies miss that deadline and apply for extensions, but eventually file an annual report. That deadline and the numerous delayed filings explain why publication of this OGJ report on pipeline economics occurs later in each year. Earlier publication would exclude many companies' information.

• Periodic reports. When a FERC-regulated natural gas pipeline company wants to modify its system, it must apply for a "certificate of public convenience and necessity." This filing must explain in detail the planned construction, justify it, and––except in certain instances—specify what the company estimates construction will cost.

Not all applications are approved. Not all that are approved are built. But, assuming a company receives its certificate and builds its facilities, it must—again, with some exceptions—report back to FERC how its original cost estimates compared with what it actually spent.

OGJ spends the year July 1 to June 30 monitoring these filings, collecting them, and analyzing their numbers.

OGJ's exclusive, annual Pipeline Economics Report began tracking volumes of gas transported for a fee by major interstate pipelines for 1987 (OGJ, Nov. 28, 1988, p. 33) as pipelines moved gradually after 1984 from owning the gas they moved to mostly providing transportation services.

Volumes of natural gas sold by pipelines have been steadily declining, so that, beginning with 2001 data in the 2002 report, the table only lists volumes transported for others.

The company tables also reflect asset consolidation and merger activity among companies in their efforts to improve transportation efficiencies and bottom lines.

Reporting changes

The number of companies required to file annual reports with FERC may change from year-to-year, with some companies becoming jurisdictional, others nonjurisdictional, and still others merging or being consolidated out of existence.

Such changes require care be taken in comparing annual US petroleum and natural gas pipeline statistics.

Institution by FERC of the two-tiered (2 and 2A) classification system for natural gas pipeline companies after 1984 further complicated comparisons (OGJ, Nov. 25, 1985, p. 55).

Only major gas pipelines are required to file miles operated in a given year. The other companies may indicate miles operated, but are not specifically required to do so.

For several years after 1984, many non-majors did not describe their systems. But filing descriptions of their systems has become standard, and most provide miles operated.

Reports for 2012 show an increase in FERC-defined major gas pipeline companies: 93 companies of 162 filing for 2012, from 92 of 157 for 2011.

The FERC made an additional change to reporting requirements for 1995 for both crude oil and petroleum products pipelines. Exempt from requirements to prepare and file a Form 6 were those pipelines with operating revenues at or less than $350,000 for each of the 3 preceding calendar years. These companies must now file only an "Annual Cost of Service Based Analysis Schedule," which provides only total annual cost of service, actual operating revenues, and total throughput in both deliveries and barrel-miles.

In 1996 major natural gas pipeline companies were no longer required to report miles of gathering and storage systems separately from transmission. Thus, total miles operated for gas pipelines consist almost entirely of transmission mileage.

FERC-regulated major natural gas pipeline mileage fell in 2012 (Table 1), final data showing a decrease of 1,008 miles, or 0.52%.

Rankings; activity

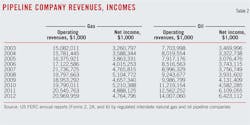

Natural gas pipeline companies in 2012 saw operating revenues rise by more than $424 million or roughly 2.1% from 2011, continuing the gains seen the year before. Net incomes, however, fell roughly $123 million (more than 2.5%), also continuing the trend begun in 2010.

Oil pipelines fared better, with earnings rising more than $314 million (5%) on the back of a more than $1.4 billion (11.5%) increase in revenues (Table 2). Crude deliveries for 2012 increased by more than 439.5 million bbl or 6.25%, outpacing a 128-million bbl increase in product deliveries.

OGJ uses the FERC annual report data to rank the top 10 pipeline companies in three categories (miles operated, trunkline traffic, and operating income) for oil pipeline companies and three categories (miles operated, gas transported for others, and net income) for natural gas pipeline companies.

Positions in these rankings shift year to year, reflecting normal fluctuations in companies' activities and fortunes. But also, because these companies comprise such a large portion of their respective groups, the listings provide snapshots of overall industry trends and events.

For instance, the growth in oil pipeline earnings was driven by the top 10 companies in the segment, for which combined income climbed more than $360 million, making up for losses seen in the rest of the segment. The top 10 companies' share of the segment's total earnings was roughly 58%. Both Phillips 66 Pipeline LLC and Enbridge Energy LP had net incomes in excess of $500 million, or combined roughly one-fifth of the segment's total earnings.

Company financial data provide a view of the ongoing condition of the oil and gas pipeline industries.

For all natural gas pipeline companies, for example, net income as a portion of operating revenues slipped to 22.90% in 2012, continuing the fall from the record highs seen in 2010 to the lowest level seen since 2007. The percentage of income as operating revenues for oil pipelines slipped from its own 2011 record of 48.63% to 45.86%, but remained well above 2010 levels.

Net income as a portion of gas-plant investment slipped to 3.35%, the lowest level in at least 16 years. Net income as a portion of investment in oil pipeline carrier property eased from the records reach in 2012 to 11.9%, still above the previous-high of 11.5% reached in 2006. Income as part of investment in carrier property in 2004 stood at 11.4%, having risen steadily toward that level from 6.8% in 1998.

Major and nonmajor natural gas pipelines in 2012 reported an industry gas-plant investment of more than $142 billion, the highest levels ever, up from $138.6 billion in 2011, $124.7 billion in 2010, almost $121.3 billion in 2009, and nearly $105.8 billion in 2008.

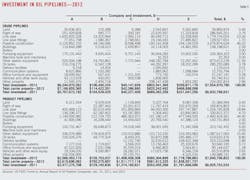

Investment in oil pipeline carrier property also continued to rise in 2012, reaching more than $54 billion after hitting roughly $49.2 billion in 2011, almost $45.4 billion in 2010, $41.6 billion in 2009, and $39.1 billion in 2008.

OGJ for many years has tracked carrier-property investment by five crude oil pipeline and five products pipeline companies chosen as representative in terms of physical systems and expenditures (Table 3). In 2003, we added the base carrier-property investment to allow for comparisons among the anonymous companies.

The five crude oil pipeline companies in 2012 increased their overall investment in carrier property by more than $622 million (roughly 9%), accelerating the smaller gains seen in 2011. All but the smallest of the companies increased investment in carrier property.

The five products pipeline companies also saw their overall investment in carrier property accelerate in 2012, adding $115 million, or 1.66%. Reflecting the smaller overall growth rate than that seen in crude oil lines, two of the products pipeline companies saw their investment in carrier property fall in 2012.

Even so, investment by the five product pipeline companies in 2012 was more than $7 billion, continuing a return to growth started in 2003 when investment of more than $4.7 billion was up from 2002's $4.5 billion level.

Comparisons of data in Table 3 with previous years' must be done with caution: in 2004, a major crude oil pipeline company listed there sold significant assets, making comparisons with previous years' data difficult.

Fig. 2 illustrates the investment split in the crude oil and products pipeline companies.

Construction mixed

Applications to FERC by regulated interstate natural gas pipeline companies to modify certain systems must, except in certain instances, provide estimated costs of these modifications in varying degrees of details.

Tracking the mileage and compression horsepower applied for and the estimated costs can indicate levels of construction activity over 2-4 years. OGJ has been doing that since this report began more than 50 years ago.

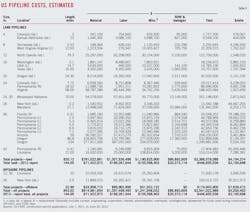

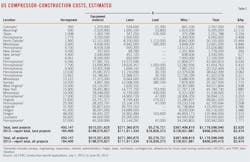

Tables 4 and 5 show companies' estimates during the period July 1, 2012, to June 30, 2013, for what it will cost to construct a pipeline or install new or additional compression.

These tables cover a variety of locations, pipeline sizes, and compressor-horsepower ratings. Not all projects proposed are approved. And not all projects approved are eventually built.

Applications filed in the 12 months ending June 30, 2013, jumped after falling for 3 consecutive years.

• More than 820 miles of pipeline were proposed for land construction, and nearly 23 miles for offshore. The land level is up sharply from the 144 miles proposed in 2012, but still falls short of the 2,180 miles proposed for land construction in 2009, the highest level since more than 2,700 miles were proposed in 1998.

• New or additional compression proposed by the end of June 2013 measured more than 450,000 hp, up from the 184,000 hp proposed in 2012 and the highest level seen since 664,775 hp was proposed in 2009.

Putting the uptick in US gas pipeline construction in perspective, Table 4 lists 26 land-pipeline "spreads," or mileage segments, and 2 marine projects, compared with:

• 11 land and 0 marine projects (OGJ, Sept. 3, 2012, p. 118).

• 31 land and 0 marine projects (OGJ, Sept. 5, 2011, p. 97).

• 8 land and 0 marine projects (OGJ, Nov. 1, 2010, p. 108).

• 21 land and 0 marine projects (OGJ, Sept. 14, 2009, p. 66).

• 19 land and 0 marine projects (OGJ, Sept. 1, 2008, p. 58)

All but six of the spreads in 2013 measured 50 miles or less, suggesting a continued emphasis on connecting new production sources to existing transmission infrastructure rather than building new large transmission lines; particularly with 14 of the total coming in under 15 miles, and 7 at less than 5 miles.

For the 12 months ending June 30, 2013, the 26 land projects would cost an estimated $3.4 billion, as compared with $447 million for 11 projects a year earlier. The 2 offshore projects for the current year were estimated to cost a total $175 million.

It is helpful to remember that these statistics cover only FERC-regulated pipelines. Many other pipeline construction projects were announced in the 12 months ending June 30, 2013, but as mentioned earlier, many of these projects involved connecting developing natural gas shale plays such as Eagle Ford and Marcellus to already operating transportation infrastructure and may have lied outside of FERC's jurisdiction.

A report conducted in 2011 on behalf of the Interstate Natural Gas Association of America concluded that the United States and Canada will require annual average midstream natural gas investment of $8.2 billion per year, or $205.2 billion (in real 2010 dollars) total, over the nearly 25-year period from 2011 to 2035 to accommodate new gas supplies, particularly from the prolific shale gas plays, and growing demand for gas in the power-generation sector. The capital investment requirement includes mainlines, laterals, processing, storage, compression and gathering lines. These totals included $20 billion of investment in the Marcellus shale region alone.

Against this backdrop, estimated $/mile costs for new projects as filed by operators with FERC rebounded from the 5-year lows seen last year. For proposed onshore US gas pipeline projects in 2012-13 the average cost was $3.5 million/mile; in 2011-12 the average cost was $3.1 million/mile; in 2010-11 the average cost was $4.4 million/mile; in 2009-10 the average cost was $5.1 million/mile; and in 2008-09 the average onshore cost was $3.7 million/mile.

The estimated $/mile costs for new offshore projects in 2012-13 was $7.6 million/mile.

Cost components

Variations over time in the four major categories of pipeline construction costs—material, labor, miscellaneous, and right-of-way (ROW)—can also suggest trends within each group.

Materials can include line pipe, pipe coating, and cathodic protection.

"Miscellaneous" costs generally cover surveying, engineering, supervision, contingencies, telecommunications equipment, freight, taxes, allowances for funds used during construction (AFUDC), administration and overheads, and regulatory filing fees.

ROW costs include obtaining rights-of-way and allowing for damages.

For the 26 land spreads filed for in 2012-13, cost-per-mile projections rose in all categories except ROW and damages, which eased for the third straight year. In 2011 miscellaneous charges actually passed material to become the second most expensive cost category and they retained this position through 2013:

• Material—$952,328/mile, up from $495,821/mile for 2011-12.

• Labor—$1,594,323/mile, up from $1,383,277/mile for 2011-12.

• Miscellaneous—$1,451,770/mile, up from $1,080,169/mile for 2011-12.

• ROW and damages—$105,953/mile, down from $141,431/mile for 2011-12.

The continued rise in miscellaneous costs was driven by companies increasing the amount set aside for contingencies in their estimates.

Table 4 lists proposed pipelines in order of increasing size (OD) and increasing lengths within each size.

The average cost-per-mile for the projects rarely shows clear-cut trends related to either length or geographic area. In general, however, the cost-per-mile within a given diameter decreases as the number of miles rises. Lines built nearer populated areas also tend to have higher unit costs.

Additionally, road, highway, river, or channel crossings and marshy or rocky terrain each strongly affect pipeline construction costs.

Fig. 3, derived from Table 4, shows the major cost-component splits for pipeline construction costs.

Labor costs fell as a portion of land construction costs, but remained the single most expensive category. Labor's portion of estimated costs for land pipelines slipped to 38.84% in 2013, from 44.61% in 2012, 44.27% in 2011, 44.61% in 2010, 37.95% in 2009, and 39.76% in 2008. Material costs for land pipelines saw its share of total costs continue to recover, reaching 23.2% in 2013 as compared with 15.99% in 2012 and 14.54% in 2011, but still well below the 31.01% seen in 2010, 35.19% in 2009, and 30.93% in 2008.

Fig. 4 plots a 10-year comparison of land-construction unit costs for the two major components, material and labor.

Fig. 5 shows the cost split for land compressor stations based on data in Table 5.

Table 6 lists 10 years of unit land-construction costs for natural gas pipeline with diameters ranging from 8 to 36 in. The table's data consist of estimated costs filed under CP dockets with FERC, the same data shown in Tables 4 and 5.

Table 6 shows that the average cost per mile for any given diameter may fluctuate year to year as projects' costs are affected by geographic location, terrain, population density, or other factors.

Completed projects' costs

In most instances, a natural gas pipeline company must file with FERC what it has actually spent on an approved and built project. This filing must occur within 6 months after the pipeline's successful hydrostatic testing or the compressor's being put in service.

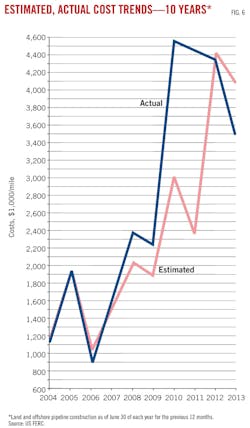

Fig. 6 shows 10 years of estimated vs. actual costs on cost-per-mile bases for project totals.

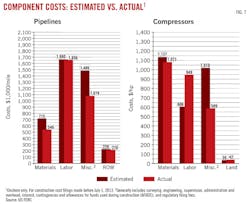

Tables 7 and 8 show actual costs for pipeline and compressor projects reported to FERC during the 12 months ending June 30, 2013. Fig. 7, for the same period, depicts how total actual costs ($/mile) for each category compare with estimated costs.

Actual miscellaneous costs for pipeline construction were more than $400,000/mile lower than estimated costs for the same projects. Overall actual costs were 14.6% lower than projected costs for the 12 months ending June 30, 2013, despite flat labor costs.

Some of these projects may have been proposed and even approved much earlier than the 1-year survey period. Others may have been filed for, approved, and built during the survey period.

If a project was reported in construction spreads in its initial filing, that's how projects are broken out in Table 4. Completed projects' cost data, however, are typically reported to FERC for an entire filing, usually but not always separating pipeline from compressor-station (or metering site) costs and lumping various diameters together.

The 12 months ending June 30, 2013, saw nearly 143,000 hp of new or additional compression completed, down from more than 700,000 hp the year before.

Actual compression costs were $136/hp (4.9%) lower than estimates, with softer than expected miscellaneous costs outweighing higher than expected labor prices (Table 8).

Click here to view the PDF of the "Gas Pipeline Companies"

About the Author

Christopher E. Smith

Editor in Chief

Chris joined Oil & Gas Journal in 2005 as Pipeline Editor, having already worked for more than a decade in a variety of oil and gas industry analysis and reporting roles. He became editor-in-chief in 2019 and head of content in 2025.