Falling Russian diesel exports tighten global distillate markets

Atlantic Basin diesel markets have tightened sharply in recent weeks as the loss of Middle Eastern barrels has coincided with a steep decline in Russian diesel exports.

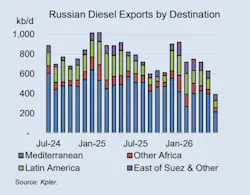

Russian diesel exports have fallen by nearly half in recent weeks, according to trade data, as intensifying Ukrainian drone strikes have disrupted refining operations. On July 8, Russia imposed a temporary ban on diesel exports through the end of July to address growing domestic fuel shortages.

Since August 2025, Ukraine has carried out at least 100 strikes on Russian refineries, with the campaign accelerating in recent months. At least 10 refinery attacks were reported in June alone. Nearly every major refinery in western Russia has been targeted, while strikes have recently reached the 450,000-b/d Omsk refinery in western Siberia—about 2,700 km from the front line in eastern Ukraine. Several refineries have been hit multiple times as attacks continued through June and into July.

Russian crude runs have reportedly fallen below 3.8 million b/d, down about 1.6 million b/d from a year earlier. Combined with attacks on storage terminals and other energy infrastructure, the disruption has reduced refined product output, contributing to widespread domestic fuel shortages and prompting the temporary export ban.

The strikes are also increasingly threatening Russia's export infrastructure. Kyiv has said these plants are legitimate military targets because energy exports help finance Russia's war effort. Export hubs on the Black Sea at Tuapse and the Baltic at Ust-Luga, along with major refineries connected to diesel export pipelines—including Perm, Moscow, Syzran, and Kirishi—have all come under attack, raising the risk of further disruptions to both diesel supply and export flows.

Diesel crack spreads surge as buyers compete for supply

Diesel crack spreads have jumped above jet fuel cracks in recent weeks as falling Russian exports tighten Atlantic Basin distillate markets, according to data from the International Energy Agency (IEA), with benchmark cracks rallying from lows near $40/bbl in mid-June to about $70/bbl in mid-July.

Key importing markets across North Africa and as far afield as Brazil have had to secure replacement supply as Russian volumes disappear, IEA said. European buyers, who are barred from importing Russian material, continue to lean on US exports to fill the gap. That reliance comes as two other potential swing sources—Middle East and India—remain constrained. The resulting competition for available cargoes is once again lifting European arbitrage values, drawing more barrels toward the region.