EIA forecasts prolonged oil market tightening amid Hormuz shipping disruptions

In its June 2026 Short-Term Energy Outlook (STEO), the US Energy Information Administration (EIA) assumes the Strait of Hormuz will remain effectively closed in the near term, with oil shipments resuming in third-quarter 2026.

The agency expects it will take until early 2027 for traffic through the waterway to return to pre-conflict levels. Some Middle East oil production is expected to remain disrupted beyond the forecast period.

Global oil producers in the Middle East reduced crude oil production by more than 11 million b/d in May compared with pre-conflict levels because of limited shipping traffic through the strait. EIA estimates production shut-ins averaged 11.3 million b/d in May and forecasts disruptions of 11.34 million b/d in June before easing to 10.11 million b/d in the third quarter and 5.70 million b/d in the fourth quarter.

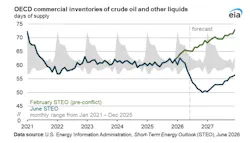

As a result, EIA expects global oil inventories to fall by an average of 6.3 million b/d in second-quarter 2026 and 7.6 million b/d in third-quarter 2026. OECD commercial inventories are forecast to fall to just under 2.3 billion bbl by December 2026, the lowest level since 2003. On a days-of-supply basis, OECD inventories are expected to fall to 50 days by yearend 2026.

Brent crude oil averaged $107/bbl in May, down $10/bbl from April. EIA forecasts Brent prices will average about $105/bbl in June and July before declining to an average of $89/bbl in fourth-quarter 2026 as oil flows gradually resume. Brent is forecast to average $95/bbl in 2026 and $79/bbl in 2027.

High fuel prices, reduced fuel availability, and government initiatives have lowered oil demand, EIA said. The agency now forecasts global oil demand will decline by 1.1 million b/d in 2026 compared with 2025 levels of 104.0 million b/d. The June forecast contrasts with EIA’s May outlook, which projected demand growth of 0.2 million b/d, and its February outlook, which projected growth of 1.2 million b/d.

Most of the demand reduction is expected in Asia. EIA forecasts demand will rebound in 2027, increasing by 2.5 million b/d to 105.3 million b/d as prices decline and supply flows return.

US petroleum exports

Disruptions to crude oil and refined product flows through the Strait of Hormuz have increased demand for US supplies.

US crude oil and petroleum product net exports reached a record 5.8 million b/d in April, with May net exports remaining near that level. EIA forecasts total US net exports of crude oil and petroleum products will average 4.2 million b/d in 2026, up 1.4 million b/d from 2025, before easing to 3.9 million b/d in 2027.

Net exports of petroleum products are forecast to average 5.6 million b/d in 2026, the highest annual level on record. Distillate fuel net exports are expected to average 1.5 million b/d in second-quarter 2026, up 27% from the same period last year, while jet fuel net exports are forecast to average 0.3 million b/d compared with about 0.1 million b/d in second-quarter 2025.

US crude oil imports averaged 5.6 million b/d over the 4 weeks ending May 1, the lowest monthly level since February 2021. During the same period, crude oil exports averaged 5.4 million b/d, which EIA said would be a record.

Higher crude prices also boosted petroleum product price forecasts. EIA forecasts average wholesale gasoline prices of $2.98/gal in 2026 and $2.61/gal in 2027. Diesel prices are forecast at $3.40/gal in 2026 and $2.98/gal in 2027, while jet fuel prices are expected to average $3.37/gal in 2026 and $2.86/gal in 2027.

Natural gas output grows

EIA forecasts US marketed natural gas production will increase 3.3% in 2026, or about 3.9 bcfd, followed by an additional 2.5% increase in 2027.

The agency expects the US will produce 4.6 bcfd more natural gas in 2027 than projected in its January STEO, largely because of higher associated gas production in the Permian region. Production growth is also expected in the Haynesville region.

Henry Hub spot prices averaged $2.94/MMbtu in May. EIA forecasts Henry Hub prices will average $3.60/MMbtu in 2026 and $3.46/MMbtu in 2027.

US LNG gross exports are forecast to average 17 bcfd in 2026 and 19 bcfd in 2027.