Diplomacy overrides fundamentals for oil prices

Oil, fundamental analysis

After an early rise, oil prices fell back this week as the market put more trust in diplomacy than physical fundamentals. Domestic and global stocks of crude continue to be drawn-down but US refined product inventories did increase last week. WTI’s Low was Monday’s $88.45/bbl for July while the High was Wednesday’s $97.00 on the large commercial crude draw. Brent crude hit its Low on Monday at $92.20/bbl with the low on Wednesday at $99.00. Both grades settled higher while the WTI/Brent spread has now tightened to ($2.70) which could make exports to Europe uneconomical.

Despite a supposed ceasefire amidst peace talks, hostilities on both sides continued in the war this week. Hezbollah has rejected a US-brokered agreement between Israel and Lebanon while Iran continues to insist on an Israeli ceasefire as a condition for any agreement. Iran attacked Kuwait’s International Airport. Oil prices also spiked briefly Friday on reports of an Iranian attack on an Omani export terminal. Prices later reversed when officials there said operations were unaffected. Oman exports between 800,000-900,000 bld. Meanwhile, the US has reportedly struck Iran’s Qeshm Island, a key location in the control of the Strait of Hormuz.

The current crisis in the Persian Gulf has forced the oil industry to put more of a focus on the actual ability to deliver oil vs. its actual production. “Spare capacity” has always meant increasing supply at the field level but not necessarily a guarantee that said barrels could physically be delivered to where they were needed.

China decreased its crude imports once again last month. The world’s No. 1 oil importer averaged 6.4 million b/d in May, down from 11.4 in February while refining about 13.5 million b/d with the balance coming from strategic reserves which it was able to build up over the course of last year with heavy buying.

The lower exports are helping to keep a lid on global oil prices. However, China, like every other country that is using strategic stockpiles, will have to return to buying for replenishment eventually.

South American countries Brazil, Guyana, and Venezuela have increased their crude exports by 1.0 million b/d over the first 5 months of the year, which comes at an opportune time. All three countries are projected to continue to improve their output through this year and next. Brazil is also increasing its refining capacity to take advantage of growing crude production which will allow it to export more products. And Venezuela is negotiating a long-term agreement with Indian refiners.

The use of strategic stockpiles has US traders once again turning their focus to the Cushing, OK, hub where commercial reserves have also been declining in recent weeks. The key delivery point for the NYMEX WTI futures contract is down to 22.4 million bbl as of last week. Capacity there is about 76 million bbl spread across hundreds of above-ground tanks with some of those used strictly for blending heavier grades of crude with the lighter shale oil.

Representing 16% of domestic commercial crude storage capacity, Cushing receives crude from various areas of the Midwest, Rockies, West TX, and Canada and distributes it to Midwest and Gulf Coast refineries. Companies active there have stated that operational problems with deliverability start to occur below the 20 million bbl level.

The Energy Information Administration’s (EIA) Weekly Petroleum Status Report indicated that commercial crude oil inventories for last week decreased while refined products increased. Oil production remained stable at 13.7 million b/d. The Strategic Petroleum Reserve (SPR) was down 8.0 million bbl to 357 million bbl. Stocks at Cushing were down 0.6 million bbl to 22.4 or 29% of capacity.

More jobs than expected were added in May with an additional 172,000 vs. a 80,000-gain forecast with increases largely in the healthcare and services sector. However, the unemployment rate remained at 4.3%. Fed officials now have to weigh positive jobs growth vs. higher Treasury yields and inflation in considering any interest rate changes. Some officials are said to be leaning towards a rate increase to combat inflation. All three major US stock indices are lower at week’s end after hitting new peaks earlier. The Dow remains above the key 50,000 mark, however. The USD is higher which is aiding the decline in crude oil prices while gold is lower.

Oil, technical analysis

July WTI NYMEX futures have fallen back below the 13- and 20-day Moving Averages (MA) but either side of the 8-day MA. Volume is below the recent average at 165,000. The Relative Strength Indicator (RSI), a momentum indicator is neutral at 45. Resistance is now pegged at $93.80 (13-day MA) while near-term Support is $90.10. Despite the optimism in the market currently, traders still need to take cautious positions ahead of the weekend since the status of a ceasefire and peace accord are still unknown.

Looking aead

An actual halt of all hostilities will be necessary before the market can believe that a permanent re-opening of the Strait of Hormuz will occur. Bids for federal oil leases in the Alaska National Wildlife Reserve (ANWR) will be opened this week which will indicate the industry’s desire to invest in new exploration and production there.

Fitch Ratings (London) is predicting that the Strait of Hormuz will be open by end-July and that the resultant logistical loosening will actually lead to a supply/demand surplus during fourth-quarter 2026. The agency contends that production capacity in the Persian Gulf has not been damaged extensively and that the situation is strictly about supply chain infrastructure. And while they project that OPEC will take an aggressive supply recovery stance, they do not address the replenishment of the reserves being depleted currently.

Natural gas, fundamental analysis

The July NYMEX natural gas futures jumped last week on the monthly roll, but have fallen back this week on a technical move and a lack of widespread warmer temperatures as storms persist in large areas of the country. A smaller-than-expected storage injection could not sustain the higher prices.

The week’s High was Monday’s $3.40/MMbtu which broke the Upper-Bollinger Band Limit while the Low was Tuesday’s $3.10. Natural gas demand this week has been estimated at about 98 bcfd on increased power consumption while supply was thought to be 109 bcfd. Inputs to LNG export plants were down to 16 bcfd due to planned maintenance outages. Exports to Mexico were 7.0 bcfd.

In the UK, natural gas prices at the NBP were most recently higher at $15.70/MMbtu. Dutch TTF futures were also higher at $16.55/MMbtu. Asia’s JKM was quoted at $18.80/MMbtu as Asian and European markets are essentially competing for the same shipments. The EIA’s Weekly Natural Gas Storage Report indicated an injection of 95 bcf vs. a forecast of +105 and a 5-year average of +98 bcf. Total gas in storage is now 2.578 tcf, 5.7% above the 5-year average.

Natural gas, technical analysis

July 2026 NYMEX Henry Hub Natural Gas futures are above the 13- and 20-day Moving Averages and right on the 8-day MA. Volume is around the recent average at 145,00. The RSI is neutral at 53. Support is $3.25 with key Resistance at $3.35 (Bollinger Band).

Looking ahead

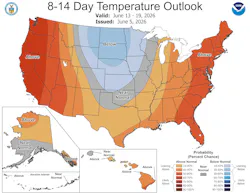

LNG exports are down currently on routine maintenance but warmer summer weather should increase demand for gas-fired generation. Delfin Midstream has reached a final investment decision for an offshore FLNG vessel about 45 miles off the coast of Cameron Parish, La. It will be the first of its kind for the US. The 8-to-14-day forecast indicates that about 2/3 of the country will see above-normal summer temperatures.

About the Author

Tom Seng

Dr. Tom Seng is an Assistant Professor of Professional Practice in Energy at the Ralph Lowe Energy Institute, Neeley School of Business, Texas Christian University, in Fort Worth, Tex.