EIA: Prolonged Strait of Hormuz disruption reshapes global oil markets

Disruptions to crude oil production in the Middle East have increased significantly since the US Energy Information Administration (EIA)’s April Short-Term Energy Outlook (STEO), leading the agency to revise its assumptions in the May outlook as the disruption continued.

In its April STEO, EIA assumed the conflict would not extend beyond April and that traffic through the Strait of Hormuz would gradually resume, though not return to pre-conflict levels until late 2026. In the May STEO, however, EIA assumes the strait will remain effectively closed through late May, with oil flows gradually resuming in late May or early June. Pre-conflict production and trade patterns are not expected to largely resume until late 2026 or early 2027. Some Persian Gulf producers are not expected to return to pre-conflict production levels during the forecast period.

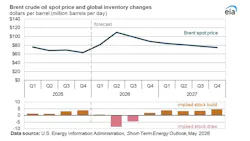

Brent crude oil spot prices averaged $117/bbl in April, an increase of $46/bbl from the February average. EIA data showed the April average was the highest monthly level since June 2022 following Russia’s invasion of Ukraine. Daily Brent spot prices reached as high as $138/bbl on Apr. 7.

Tight physical crude availability widened the spread between spot prices and front-month Brent futures to nearly $30/bbl in early April as buyers sought replacement supplies. By late April, although crude prices remained elevated, spot and futures prices moved closer together as trade flows adjusted and refiners sourced alternative supplies.

Oil market volatility also increased sharply after the conflict began in late February. According to EIA, crude oil implied volatility averaged 78% based on CME Group futures and options data, with daily Brent implied volatility reaching 106% on Mar. 12. Before the conflict, implied volatility had generally remained below 30% since the beginning of 2024. Recent Brent volatility levels were the highest since the start of the COVID-19 pandemic in early 2020.

Crude oil production disruptions

Middle East crude oil production disruptions increased during the conflict. Production shut-ins averaged 10.5 million b/d in April and are forecast to peak at nearly 10.8 million b/d in May as storage levels reach maximum capacity. Forecast revisions also reflected expectations that Iran would reduce production as the US blockade curtailed Iranian oil exports.

EIA estimates showed total crude oil production shut-ins of 8.92 million b/d in March 2026, 10.54 million b/d in April 2026, and a forecast 10.75 million b/d in May 2026. Forecast aggregate disruptions were estimated at 8.83 million b/d in June 2026, 6.41 million b/d in third-quarter 2026, and 1.71 million b/d in fourth-quarter 2026.

Initial assessments following the closure suggested that months of global oversupply and elevated oil inventories positioned markets to absorb a short-term disruption. However, inventories continued to decline as the disruption persisted. Higher prices are expected to eventually stimulate supply growth from price-responsive producers such as US shale producers, although such responses are expected to require several months—and even longer in other regions. Demand reductions are expected to occur more quickly, helping move the oil market toward balance.

Oil demand, oil price

EIA revised global oil demand growth expectations downward because of higher prices, fuel shortages, government initiatives to reduce fuel use, and reduced refined product exports. Demand reductions were assumed to occur mainly in Asia because of the region’s heavier reliance on Middle Eastern crude supplies.

Global oil demand growth for 2026 was revised to 0.2 million b/d, compared with 0.6 million b/d in the previous month’s forecast and 1.2 million b/d in the February forecast. Oil demand was expected to rebound in 2027 as supply flows returned later in 2026, with demand increasing by 1.5 million b/d to 105.6 million b/d.

Although the US announced a ceasefire in early April, oil prices were still expected to include a significant risk premium throughout the forecast period. Traffic through the Strait of Hormuz remained largely halted because of risks to oil tankers and the US blockade on Iranian oil shipments through the strait.

About the Author

Conglin Xu

Managing Editor-Economics

Conglin Xu, Managing Editor-Economics, covers worldwide oil and gas market developments and macroeconomic factors, conducts analytical economic and financial research, generates estimates and forecasts, and compiles production and reserves statistics for Oil & Gas Journal. She joined OGJ in 2012 as Senior Economics Editor.

Xu holds a PhD in International Economics from the University of California at Santa Cruz. She was a Short-term Consultant at the World Bank and Summer Intern at the International Monetary Fund.