Rising gasoline prices and their impact on US inflation and economy

Mark Finley

Rice University | Baker Institute

Prices at the pump are rising sharply. According to AAA, the national average price for regular gasoline has risen by nearly 90¢/gal over the past month to near $3.80; diesel prices have risen even more rapidly, by roughly $1.40/gal to just over $5, using Mar. 17 data.

Higher prices are good for domestic producers, but not for consumers.

Higher prices at the pump will weigh on consumer spending and confidence—and, if history is a guide, on the approval ratings of political leaders. Based on average US daily gasoline consumption of 8 million b/d, if current prices remain in place over the rest of the year, the average American family could pay over $600 more for gasoline alone. That figure comes before considering the higher cost of fuel for domestic trucking and shipping, agriculture, petrochemicals, and elsewhere in the economy.

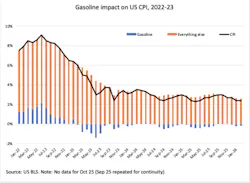

Gasoline’s outsized role in inflation

Gasoline plays an especially important role in inflation because of its outsized volatility, despite the relatively small weight it carries in official inflation calculations.1 In February, the 12‑month CPI inflation rate was 2.4%. With gasoline prices showing a small year‑on‑year decline, gasoline reduced the headline figure by 0.165%. Excluding gasoline, the inflation rate would have been 2.565%.

Where are we heading, and what will it mean for inflation? Prices at the pump are unpredictable, and what follows is hypothetical.

Based on average prices so far in March, and if prices remain at current levels going forward, I estimate that gasoline would add about two‑thirds of a percentage point to the headline CPI inflation figure when March data are released next month. If inflation for everything else remains constant, the headline 12‑month CPI would rise to about 3.2–3.3% from about 2.4% in February. (That assumption—that inflation for everything else remains flat—is questionable, given how higher prices for other oil products such as diesel and jet fuel are likely to be passed along.)

That would be a significant jump, but it pales in comparison with the role gasoline played in the surge in inflation in 2022. Then, the 12‑month CPI peaked at 9.1% in June, and gasoline added more than 2.1% to the headline figure. At that time, prices at the pump briefly exceeded $5/gal, and for that month gasoline inflation stood at 60% year‑on‑year.

To reach that level again, prices at the pump would have to rise by an additional $1/gal. In turn, that would require crude oil prices to increase by a further $40/bbl, or refining margins to rise by a similar amount—or some combination of the two. While today we appear to be a long way from that outcome, the ongoing disruption of oil flows through the Strait of Hormuz—the largest disruption in the history of the global oil market—and the related attacks on energy infrastructure in the region mean this is something worth watching.

[1] The weight varies depending in large part on fluctuations in gasoline prices. In recent years it has typically been 3-5% of total consumer spending in calculating the CPI basket.

Author

Mark Finley is a nonresident fellow in energy and global oil at Rice University’s Baker Institute. He has over 35 years of experience working at the intersections of energy, economics, and public policy. Before joining the Baker Institute, Finley was the senior US economist at BP.

Iran war coverage hub

This Iran war compilation hub highlights news, insights, and updates from Oil & Gas Journal and Offshore, both EndeavorB2B brands, concerning the war in Iran.

About the Author

Mark Finley

Mark Finley is the nonresident fellow in energy and global oil at Rice University’s Baker Institute. He has over 35 years of experience working at the intersections of energy, economics and public policy.

Before joining the Baker Institute, Finley was the senior U.S. economist at BP. For 12 years, he led the production of the BP Statistical Review of World Energy.