Oil, fundamental analysis

Global oil prices entered their fourth week of declines as supplies out of the Persian Gulf region appear to be loosening up and as talks between the US and Iran appear to be progressing. Prices have now fallen ($19.00)/bbl over the last 4 weeks. A larger-than-expected inventory draw was largely ignored.

WTI’s High was Tuesday’s $71.60/bbl for July while the Low was Thursday’s $67.05. Brent crude hit its High on Tuesday at $72.30/bbl with the low on Monday at $71.45. WTI settled slightly lower week on week Brent was higher. The WTI/Brent spread has now tightened to ($3.32). NYMEX regular session trading was closed on Friday for the July 4th holiday while thin volumes traded on their electronic platform.

Crude oil tankers are reported to be moving through the Strait of Hormuz given Iran’s agreement to allow such passage during the MOU’s 60-day negotiation period. Tanker-tracker services are estimating that about 20-30 tankers and cargo vessels per day are traversing the Strait now compared to 100-120 per day pre-war. The result has been a lowering in the risk premium and a dramatic “bearish” shift in the market sentiment for oil pricing. The future of the operation of the Strait remains unclear as Iran is in talks with Oman regarding joint administration which would include fees of some type for passage. The lifting of US sanctions on Iran has also resulted in more movements of oil although they are reportedly selling at a high discount.

While diplomatic discussions in Doha appear to be in a start/stop mode, key issues have at least been identified. Iran insists on Israel exiting Lebanon completely which includes leaving “occupied” areas in the South. Meanwhile, Israel demands that Hezbollah there be completely disarmed, something that neither that group nor the Iranians agree with. And Iran has steadfastly called for Israel to halt its attacks on Lebanon. Israel and Lebanon had supposedly worked out an agreement to halt hostilities but bombings by Israel continue. Furthermore, the Iranian nuclear stockpile issues have yet to be worked out.

The Energy Information Administration’s (EIA) Weekly Petroleum Status Report indicated that commercial crude oil inventories for last week decreased for the 8th-straight week. The SPR was down 5.5 million bbl to 326 million bbl. Stocks at Cushing, Okla., were up 710,000 bbl to 19,700, or 26% of capacity. (Operators there have stated that there are issues delivering volumes below 20 million bbl.) It was the first injection in 9 weeks. Production last week was 13.8 million b/d vs. 13.8 million b/d the prior week and 13.4 last year.

The EIA is now forecasting US domestic oil production to average 13.7 million b/d this year and 14.1 million b/d in 2027. Libya has reached 1.4 million b/d in crude production on its way to a target of 1.5 million. OPEC will conduct its monthly meeting on Sunday when Saudi Arabia announces its selling price, a major market demand signal, especially for Asia.

Gasoline prices are now $3.82/gal., down $0.08/gal. from last week, down $0.44/gal. from last month, and up $0.66/gal. from last year.

The US only added 57,000 jobs last month, lower than the forecasted +115,000 and ending a streak of positive additions the past few months. The unemployment rate lowered to 4.2%, however continuing the “slow hire, slow fire and slow growth” economy. The Dow hit another high this week, settling at 52,900 while the S&P and NASDAQ were also higher week-on-week. Gold is up for the week but far below the $5,000 mark. The USD is slightly lower which may help support oil prices.

Oil, technical analysis

August WTI NYMEX futures have below the 8-, 13-, and 20-day Moving Averages. Volume is below the recent average at 62,000 due to light trading on the electronic platform while NYMEX is closed. The Relative Strength Indicator (RSI), a momentum indicator, is very oversold at 30. Resistance is now pegged at $68.80 (8-day MA) while near-term Support is $67.00 (week’s Low).

Looking ahead

Traders may be overly-optimistic regarding sustained crude supplies flowing out of the Persian Gulf region as we are currently seeing “flowing” cargoes that have been stranded since the start of the conflict. A detailed on-the-ground assessment of damage needs to emerge before we get a clear picture of the cost and timeline for any necessary repairs. It’s too early to assume a normal resumption of pre-war production and shipping.

Meanwhile, the higher prices over the past 100 days have led to demand destruction and only time will tell just how much of that will become permanent. Furthermore, at these price levels, buying to refill strategic reserves could enter the market. The West Coast Pipeline project in Western Canada has been announced which could transport up to 1.0 million b/d of bitumen from Alberta to the Pacific Coast for exportation to Asia.

Natural gas, fundamental analysis

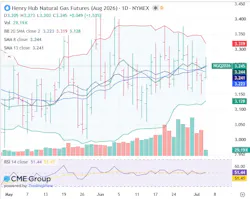

Despite warmer weather, August NYMEX Henry Hub Natural Gas futures traded lower this week on increased production and a larger-than-forecasted storage injection. The week’s High was Tuesday’s $3.35/MMbtu while the Low was Thursday’s $3.15. Natural gas demand this week has been estimated at about 108-111 bcfd on increased power consumption while supply was thought to be 116.5 bcfd. Exports to Mexico were 7.5 bcfd while LNG exports were 17 bcfd. In the UK, natural gas prices at the NBP were most recently lower at $14.30/MMbtu. Dutch TTF futures were also lower at $13.50/MMbtu. Asia’s JKM was quoted at $15.40/MMbtu as Asian and European markets are essentially competing for the same shipments. The EIA’s Weekly Natural Gas Storage Report indicated an injection of 87 bcf vs. a forecast of +81 and a 5-year average of +64 bcf. Total gas in storage is now 2.922 tcf, now -0.8% above last year and 6.4% above the 5-year average.

Natural gas, technical analysis

August 2026 NYMEX Henry Hub Natural Gas futures are trading above and below the 8-, 13-, and 20-day Moving Averages. Volume is about the recent average at 135,000 (Thursday). The RSI is neutral at 51. Critical Support is $3.15 with Resistance at $3.30.

Looking ahead

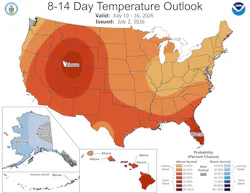

Qatar has resumed shipments of LNG out of the Persian Gulf with at least 6 cargoes destined for China so far. Meanwhile, Japan has increased the use of coal for power generation given the higher-priced LNG imports. The 8-14 day forecast looks favorable for an increase in gas-fired generation for A/C loads.

About the Author

Tom Seng

Dr. Tom Seng is an Assistant Professor of Professional Practice in Energy at the Ralph Lowe Energy Institute, Neeley School of Business, Texas Christian University, in Fort Worth, Tex.