2026 capital spending stays disciplined

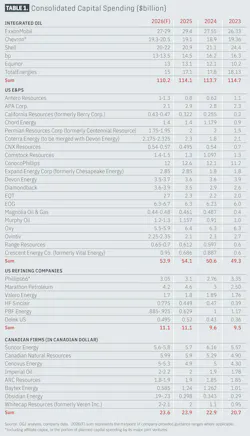

Combined capital expenditures by six major integrated oil companies—ExxonMobil Corp., Chevron Corp., Shell PLC, bp PLC, Equinor ASA, and TotalEnergies SE—are expected to ease to about $110.2 billion in 2026 from $114.1 billion in 2025, according to Oil & Gas Journal’s annual capital spending survey.

While the oil majors have not abandoned net-zero commitments, their investment priorities have clearly shifted. Medium-term carbon-reduction targets have weakened, while capital is increasingly being redirected toward higher-return upstream and LNG opportunities. Shell, for example, retired its 45% carbon-intensity reduction target for 2035, while bp has scaled back its renewable energy ambitions, reduced spending on low-carbon businesses, and divested related projects. Hydrogen initiatives, once heavily promoted across the sector, have also lost momentum. For BP and Shell, the share of capital allocated to these areas has fallen to around 10% or less, bringing them closer to the spending profiles of their US and Asian peers.

At the same time, the majors are continuing their return to core oil and gas businesses. What became increasingly evident in 2025 is carrying into 2026: a stronger focus on reserve replacement, disciplined production growth, and higher-margin projects. Rather than pursuing broad-based expansion, companies are concentrating investment on assets that can deliver stronger returns and more resilient cash flow. At the same time, many majors are also pursuing significant cost savings and capital-efficiency gains.

Among selected US exploration and production (E&P) companies remaining public after recent M&A activity, total capital spending is broadly steady at about $53.9 billion in 2026, compared with $54.1 billion in 2025. That flat spending profile underscores the sector’s continued emphasis on capital discipline, free cash flow generation, and shareholder returns. At the same time, efficiency gains—from longer laterals and lower well costs to improved drilling performance and infrastructure utilization—are helping many producers maintain activity and production growth without materially increasing capital budgets. Large shale-focused producers such as EOG Resources, ConocoPhillips, Diamondback Energy, and Occidental Petroleum remain the anchors of the group.

The refining sector is similarly stable. Total spending among the listed US refiners is holding at around $11 billion in both 2025 and 2026. Refiners continue to invest, but largely in a measured way, with capital directed toward maintenance, reliability, selective upgrades, and projects tied to efficiency improvements or regulatory compliance.

Canadian producers also present a relatively firm spending outlook, with aggregate capital expenditures of about C$23.6 billion in 2026 versus C$23.9 billion in 2025. Spending remains above 2023 and 2022 levels, pointing to sustained investment in oil sands, thermal developments, liquids-rich gas, and related infrastructure.

Taken together, the survey suggests that the 2026 spending landscape is defined less by aggressive growth than by discipline and portfolio optimization. Integrated majors are trimming budgets while pursuing meaningful cost savings, US E&Ps are keeping spending broadly flat, refiners remain steady, and Canadian producers continue to show resilience. The broader message is that the industry is still committing substantial capital, but companies are directing that spending ever more selectively—toward core assets, high-return developments, and operational resilience rather than rapid expansion across the board.

US-Iran war

The war involving the US, Israel, and Iran has introduced a new layer of uncertainty to the global energy investment outlook. Military strikes and retaliatory attacks disrupted tanker traffic through the Strait of Hormuz, helping push oil prices above $100/bbl for the first time since 2022.

Even so, higher prices alone are unlikely to trigger a broad shift in oil company spending plans. Most producers had already entered 2026 with a strong focus on capital discipline and shareholder returns, and that framework does not disappear simply because geopolitical tensions have driven prices higher. That said, if supply disruptions persist, North American spending may rise selectively.

Instead, the conflict is more likely to influence where capital is directed rather than fundamentally change overall spending behavior. The clearest beneficiaries could be North American LNG projects, as buyers look to reduce exposure to Hormuz-linked supply risks, along with established upstream positions in US shale, offshore Brazil, and Guyana, where politically stable production may become more attractive.

Majors’ spending plans

ExxonMobil projects cash capital expenditures of $27–29 billion in 2026. This investment supports the company's long-term growth, with $28–32 billion per year planned for 2027–2030. Capital is being deployed into high-return areas including the US Permian basin, Guyana, Brazil, and global LNG projects.

ExxonMobil is significantly expanding its global LNG portfolio, aiming to nearly double its supply by 2030 compared to 2020 levels. Key projects include the massive Golden Pass project in Texas, major expansions in Qatar (North Field East), the PNG LNG project in Papua New Guinea, and the Coral South FLNG project in Mozambique.

Beyond upstream investments, ExxonMobil is advancing projects within its Low Carbon Solutions division, including carbon capture and storage (CCS), hydrogen, and lithium initiatives.

Chevron said it expects 2026 organic capital spending of $18-19 billion. Of that total, about $17 billion is slated for upstream activities, including nearly $6 billion for US shale and tight assets in the Permian, Denver-Julesburg (DJ), and Bakken basins, and roughly $7 billion for offshore projects globally, mainly tied to growth in Guyana, the Eastern Mediterranean, and the Gulf of Mexico. Downstream capital spending is projected at about $1 billion, with nearly three-quarters directed to US operations.

Chevron expects affiliate capital spending of $1.3-1.7 billion in 2026, with nearly half of the total earmarked for CPChem’s two major integrated polymer projects.

Shell expects 2026 capital spending to total $20-22 billion, in line with its medium-term framework, with about $12-14 billion allocated to its Integrated Gas and Upstream businesses. Integrated gas and LNG remain at the core of the company’s strategy as Shell continues to focus investment on areas tied to growing global natural gas demand. Shell is taking a more selective approach to low-carbon investment, opting not to restart its Rotterdam biofuels project and pulling back from certain power developments, including the Atlantic Shores offshore wind project in the US.

Shell said it will continue lowering structural costs, with a goal of delivering $5-7 billion in cumulative savings by the end of 2028 relative to 2022. By yearend 2025, the operator had already achieved $5.1 billion in structural cost reductions since 2022, with additional savings still expected. About 60% of those reductions came from operational efficiencies, a leaner corporate center, and faster, value-driven decision-making.

bp plans to invest about $13–13.5 billion in 2026, reflecting its revised strategy to strengthen the role of oil and gas within its portfolio. Under its new strategy, the operator plans to raise annual oil and gas investment to about $10 billion during 2025–27, roughly 20% above its previous guidance, while targeting returns of more than 15% on those projects. Under interim leadership and ahead of Meg O’Neill taking over as chief executive officer in April 2026, bp has moved away from its role as a “green pioneer” to refocus on being a “resilient energy provider.”

bp’s upstream portfolio includes developments in the US Gulf of Mexico, Azerbaijan, and the North Sea, along with new LNG projects. To strengthen the balance sheet, bp is executing a $20-billion disposal program, including an agreement to sell a 65% stake in its Castrol lubricants business. In December 2025, bp completed the sale of its US onshore wind business, bp Wind Energy, to LS Power.

Equinor estimates 2026 organic capex at around $13 billion. The company said its capital allocation strategy remains centered on maximizing value from the Norwegian continental shelf, pursuing focused international oil and gas growth, and building an integrated power business. As part of this effort, the operator plans to improve free cash flow by cutting its 2026–27 organic capital expenditure outlook by $4 billion and reducing operating costs by 10% in 2026 through tighter cost control and portfolio high-grading. Equinor also expects oil and gas production to grow by about 3% in 2026 and aims to deliver a return on average capital employed (ROACE) of around 13% in 2026–27.

TotalEnergies’ capital expenditures reached $17.1 billion in 2025, with around one-third devoted to new oil and gas projects and $3.5 billion allocated to low-carbon energy, primarily Integrated Power. TotalEnergies plans capital spending of about $15 billion in 2026. About $3 billion is dedicated to low‑carbon energies, mainly electricity. The company is implementing a multi‑year cash‑savings plan, now targeting $12.5 billion over 2026–2030, including $2.5 billion planned for 2026.

TotalEnergies expects oil and gas production to increase by 3% in 2026, supported by the ramp-up of projects started in 2025 and by start-ups scheduled for 2026, notably Lapa Southwest in Brazil, Ratawi in Iraq, North Field East in Qatar, TFT II & South in Algeria, and Tilenga in Uganda. Integrated LNG is also expected to grow in 2026, supported by the start-up of North Field East in Qatar and Costa Azul on the Pacific coast of North America.

US E&Ps’ spending plans

Capital spending among US E&Ps is expected to remain relatively stable in 2026, as producers continue to emphasize capital discipline over aggressive growth. After several years of consolidation, the US shale sector has entered a new phase marked by larger operators, stronger balance sheets, and a sharper focus on free cash flow, operational efficiency, and shareholder returns. Major transactions such as ExxonMobil’s acquisition of Pioneer Natural Resources and ConocoPhillips’ purchase of Marathon Oil have reshaped the competitive landscape and concentrated more capital in the hands of a smaller group of large producers.

Consolidation remained a defining feature of the sector in 2025, although dealmaking became more selective. Buyers increasingly focused on inventory depth, basin fit, gas exposure, and operating synergies rather than scale alone. EOG’s $5.6-billion acquisition of Encino expanded its lower-cost Utica position instead of adding more expensive Permian inventory, while the Devon Energy-Coterra Energy merger highlighted the appeal of multi-basin scale among public E&Ps. As a result, the number of publicly listed independent producers continued to shrink.

ConocoPhillips plans capital spending of about $12 billion, a reduction of about $600 million compared with 2025, driven by efficiencies in the Lower 48 and lower major project spending. The capital is to support continued development across its global portfolio. Key investments include the Willow project in Alaska, which represents one of the largest new oil developments in the US in decades. The company is also expanding activity in the Lower 48 shale plays and participating in several international LNG projects, including developments in Qatar. The company’s 2026 production guidance is 2.33–2.36 MMboe/d.

Occidental Petroleum (Oxy) plans 2026 capital spending of $5.5–5.9 billion, a $550 million reduction from 2025 excluding OxyChem. Following the January 2026 completion of the OxyChem sale, roughly 70% of oil and gas capital will be directed to US onshore assets. Despite the lower budget, Oxy expects 2026 production to grow, averaging 1.45 MMboe/d. The company is also targeting an additional $500 million in oil and gas savings in 2026, including $300 million from capital efficiency and $200 million from operating and transportation costs.

EOG Resources plans to spend $6.3–6.7 billion in 2026, with most of the budget allocated to US shale drilling programs. The company expects oil production to increase 5% year over year and total production to rise 13%, including the impact of the Encino acquisition. EOG plans to complete 585 net wells across its domestic multi-basin portfolio of high-return assets.

The 2026 program also assumes a low-single-digit reduction in average well costs, supported by longer lateral lengths and other durable efficiency gains. Activity is expected to increase in the Utica and Dorado plays, while the company continues to advance exploration prospects in the UAE and Bahrain.

Diamondback Energy has raised its capital spending following its merger with Endeavor Energy Resources, forming one of the largest pure-play operators in the Permian basin. The company expects capital expenditures of about $3.6–3.9 billion in 2026, reflecting continued capital discipline while marking a modest increase from 2025 to support development of newly acquired, high-return inventory. The budget is primarily directed toward the Midland basin, where Diamondback plans to complete about 5.9–6.3 million net lateral ft during the year.

In February 2026, Devon Energy and Coterra Energy announced an all-stock merger valued at about $58 billion. The combined company will retain the Devon name, with Devon shareholders owning about 54% and Coterra shareholders 46%. The deal is expected to close in second-quarter 2026, pending regulatory and shareholder approvals.

Until closing, the companies must operate as separate legal entities with their own budgets and capital programs. Devon Energy plans capital expenditures of about $3.5–3.7 billion, reflecting increased activity following its acquisition of the Grayson Mill assets. Coterra Energy expects capital spending of about $2.175–2.325 billion, reflecting increased activity following recent acquisitions in the Delaware basin.

Natural gas-focused producers such as EQT Corp. and Antero Resources are maintaining solid 2026 investment programs as US LNG export capacity along the Gulf Coast continues to expand. Rising LNG demand should support overall US gas market fundamentals and improve the call on Appalachian supply, although production growth in the basin is expected to remain relatively modest and will depend in part on available pipeline takeaway capacity.

Refining sector

The refining industry has entered a period of limited capacity expansion, with companies focusing instead on improving operational efficiency, optimizing product slates, and expanding midstream and petrochemical integration. US independent refiners are expected to maintain relatively steady capital spending in 2026.

Phillips 66 continues to prioritize investment in its midstream and chemicals businesses, which have become increasingly important sources of earnings. The company’s capital program includes projects aimed at expanding gas processing capacity, strengthening its natural gas liquids (NGL) value chain, and supporting integrated operations across major US basins.

Within its refining segment, Phillips 66 is focusing on high-return, low-capital projects designed to improve margins and enhance operational flexibility rather than pursuing large-scale refinery expansions.

Marathon Petroleum Corp. continues to allocate capital toward projects that enhance efficiency and improve profitability across its refining system. The company is investing in a series of upgrades at key complexes, including Galveston Bay and Robinson, designed to improve product yields and reduce operating costs. The utility modernization project at the Los Angeles refinery was successfully implemented in fourth-quarter 2025.

At the same time, Marathon’s midstream affiliate MPLX LP is expanding pipeline and processing infrastructure, particularly in the Permian basin and the Appalachian region. These investments support growing oil and natural gas production while strengthening the company’s integrated value chain.

Valero Energy Corp. plans to invest about $1.7 billion in 2026. Of that total, roughly $1.4 billion is allocated to sustaining capital, with the balance directed toward growth projects in refining and low-carbon fuels. The company remains one of North America’s largest renewable diesel producers, although spending on renewable fuels has become more measured in recent years. Valero is also continuing work on the FCC unit optimization project at its St. Charles refinery, a $230-million investment designed to improve the plant’s ability to produce higher-value products. The project remains on track to begin operations in the second half of 2026.

Canadian producers

All financial figures are presented in Canadian dollars unless noted otherwise.

Canadian producers are expected to maintain solid capital spending in 2026 as improved market access and stronger crude prices support investment across the country’s energy sector.

One of the most significant developments for the Canadian industry has been the completion of the Trans Mountain Pipeline expansion, which began operations in 2024 after more than a decade of planning and construction. The expansion nearly tripled the pipeline’s capacity from Alberta to Canada’s Pacific coast, enabling producers to ship larger volumes of crude to international markets. As a result, the price discount for Western Canada Select (WCS) crude relative to global benchmarks has narrowed significantly, improving the economics of oil sands production.

Canada’s broader energy outlook has also been helped by the emergence of new LNG export outlets on the West Coast. LNG Canada shipped its first cargo in June 2025, marking the start of operations at Canada’s first large-scale LNG export plant. These developments are creating new demand for natural gas production in western Canada while strengthening the country’s role as a global LNG supplier.

Canadian Natural Resources’ 2026 capital spending, initially set at $6.3 billion, was revised down to about $5.99 billion, due to efficiencies and the deferral of the Jackpine mine expansion. The operator is continuing with its highly capital efficient thermal in situ drilling program and conventional E&P assets. Canadian Natural is targeting production guidance of 1.59–1.65 MMboe/d in 2026, which represents growth of 3% over 2025 levels.

Suncor Energy’s 2026 capital plan midpoint stands at $5.7 billion. Capital will be directed primarily toward sustaining operations and a targeted group of high-value projects, including in situ well pads, Mildred Lake East, the West White Rose project, Fort Hills North Pit development, and continued optimization of the Petro-Canada retail network. Key targets include 840,000–870,000 b/d in upstream production and 99–102% refining utilization.

Cenovus Energy Inc. expects capital spending of $5.0–5.3 billion in 2026, up from $4.9 billion in 2025. The budget includes $3.5–3.6 billion of sustaining capital, excluding turnarounds, to support safe and reliable operations and maintain base production. The company also plans to allocate $1.2–1.4 billion to growth projects, including the Christina Lake expansion.

Baytex is reducing capital spending in 2026 as it transitions to a more maintenance-focused and capital-efficient program, prioritizing free cash flow and shareholder returns while still advancing key growth areas such as the Pembina Duvernay.

National oil companies

National oil companies (NOCs) are expected to remain the dominant force in global upstream investment. While many international oil companies (IOCs) continue to emphasize capital discipline and shareholder returns, many major NOCs are entering a heavy investment cycle for 2026. These companies control the majority of global reserves and continue to account for a significant share of new production capacity and large-scale energy infrastructure projects worldwide.

Saudi Arabia’s Aramco remains one of the largest upstream investors globally. For fiscal year 2025, the company reported lower revenue and operating profit compared with the previous year, mainly reflecting weaker oil prices. Despite the earnings decline, Aramco maintained a steady investment pace, with capital expenditures totaling $50.8 billion in 2025, a modest increase of 0.8% year over year.

The company has issued 2026 capital spending guidance of $50–55 billion, with planned investment across liquid fuels, downstream operations, and emerging energy sectors. Aramco also continues to pursue opportunities in the global LNG market as part of its strategy to diversify its portfolio while balancing traditional hydrocarbon production.

Petrobras approved a $109 billion capex plan for 2026–2030, comprising $91 billion in its implementation portfolio and $18 billion in projects under evaluation. The operator said the plan is designed for a lower-oil-price environment and emphasizes capital discipline, stricter project screening, operational efficiency, and financial resilience.

The program remains heavily weighted toward oil and gas. Petrobras allocated $69.2 billion to exploration and production in its implementation portfolio, including 62% for presalt assets, 24% for postsalt fields, and 10% for exploration. The company expects oil production to peak at 2.7 million b/d in 2028 and total output to reach 3.4 MMboe/d in 2028-29.

Petrobras also earmarked $15.8 billion for refining, transportation, marketing, petrochemicals, and fertilizers, with plans to raise installed refining capacity to 2.1 million b/d by 2030 from 1.8 million b/d, without building new refineries. In gas and lower-carbon businesses, the company plans to invest $4 billion. Petrobras also expects to deliver about $12 billion in manageable operating-expense savings over 2025–2030.

Under the Sheinbaum administration, Mexico’s PEMEX has proposed a significant capital increase for 2026, targeting around $24.7 billion in productive investment, representing a roughly 34% increase compared with the 2025 budget. The spending program is intended to strengthen domestic oil and gas production while supporting refinery operations and reducing reliance on imported fuels.

In Asia, China’s national oil companies are also maintaining large and relatively stable investment programs. China National Petroleum Corp. (CNPC) remains the country’s dominant onshore producer and is focusing heavily on developing ultra-deep and unconventional resources to offset declines in mature fields.

China National Offshore Oil Corp. (CNOOC) set 2025 capital spending at RMB 125-135 billion, or roughly $17-19 billion, and said capex would remain stable. The company has targeted 2026 production of 780-800 MMboe and continues to prioritize offshore developments in China alongside major international projects, including Yellowtail in Guyana and Buzios 7 in Brazil. CNOOC is also advancing green-development initiatives, including offshore wind, expanded use of green power, and regional CCS/CCUS pilot projects.

About the Author

Conglin Xu

Managing Editor-Economics

Conglin Xu, Managing Editor-Economics, covers worldwide oil and gas market developments and macroeconomic factors, conducts analytical economic and financial research, generates estimates and forecasts, and compiles production and reserves statistics for Oil & Gas Journal. She joined OGJ in 2012 as Senior Economics Editor.

Xu holds a PhD in International Economics from the University of California at Santa Cruz. She was a Short-term Consultant at the World Bank and Summer Intern at the International Monetary Fund.

Laura Bell-Hammer

Statistics Editor

Laura Bell-Hammer is the Statistics Editor for Oil & Gas Journal, where she has led the publication’s global data coverage and analytical reporting for more than three decades. She previously served as OGJ’s Survey Editor and had contributed to Oil & Gas Financial Journal before publication ceased in 2017. Before joining OGJ, she developed her industry foundation at Vintage Petroleum in Tulsa. Laura is a graduate of Oklahoma State University with a Bachelor of Science in Business Administration.