OPEC forecasts global oil demand to reach 116 million b/d in 2045

In its annual World Oil Outlook report released on Oct. 9, 2023, the Organization of the Petroleum Exporting Countries (OPEC) projects global oil demand to reach 110.2 million b/d in 2028, up 10.6 million b/d compared with 2022. Non-OECD oil demand is anticipated to make up 10.1 million b/d of this increase, reaching 63.7 million b/d in 2028. OECD demand is expected to see a modest uptick of 500,000 b/d.

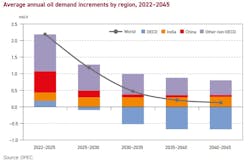

In the long-term, global oil demand is expected to increase by more than 16 million b/d between 2022 and 2045, rising from 99.6 million b/d in 2022 to 116 million b/d. During this forecast period, non-OECD oil demand is projected to surge nearly 26 million b/d, while OECD oil demand is poised to contract by approximately 9.3 million b/d.

According to OPEC's predictions, the most substantial boosts in non-OECD oil demand are set to come from India, Other Asia, China, Africa, and the Middle East. Specifically, India is projected to add 6.6 million b/d to oil demand between 2022 and 2045. Other Asia’s oil demand is set to increase by 4.6 million b/d, China’s by 4 million b/d, Africa’s by 3.8 million b/d, and the Middle East’s by 3.6 million b/d.

The largest incremental demand during the forecast period from 2022 to 2045 is projected for the road transportation, petrochemical, and aviation sectors. Oil demand in these sectors is set to increase by 4.6 million b/d, 4.3 million b/d and 4.1 million b/d, respectively. With respect to refined products, major long-term demand growth is expected for jet-kerosene (4 million b/d) followed by ethane-LPG (3.6 million b/d), diesel-gas oil (3.1 million b/d), naphtha (2.5 million b/d), and gasoline (2.5 million b/d), according to OPEC.

OPEC's predictions regarding oil demand stand in contrast to recent forecasts from the International Energy Agency (IEA), which suggest that oil demand will peak by 2030.

Energy mix

According to OPEC’s forecast, global primary energy demand is set to increase from around 291 million boe/d in 2022 to close to 359 million boe/d in 2045, an increase of 68.3 million boe/d, or 23% over the outlook period. Growth is expected to slow gradually from the relatively high short-term rates to more modest long-term increments, in line with moderating population and economic growth. Energy demand growth will be driven by the non-OECD region, which is set to increase by 69 million boe/d over the outlook period. Around 28% of non-OECD growth is expected to come from India alone. At the same time, energy demand in OECD countries is set to marginally decline.

Demand for all primary fuels except coal is set to increase in the long-term, with coal use dropping due to energy policy and climate commitments. The strongest growth is expected for renewables (notably wind and solar), which will increase by 34.3 million boe/d, based on strong policy support in many regions. The share of renewables in the energy mix is set to rise from around 2.7% in 2022 to 11.7% in 2045. Oil will remain the fuel with the largest share by 2045 at 29.5%. Natural gas demand is set to increase by 20 million boe/d over the outlook period, reaching 87 million boe/d in 2045. The share of fossil fuels in the energy mix will drop from above 80% in 2022 to about 69% in 2045, due to the decline of coal. In the same period, the combined share of oil and gas in the energy mix will still represent 54% in 2045, according to the Outlook.

Liquids supply

In this Outlook, OPEC expects non-OPEC liquids supply to grow from 65.8 million b/d in 2022 to 72.7 million b/d in 2028, a growth of nearly 7 million b/d. About 3.4 million b/d of this growth is attributed to the US, with other notable contributors being Brazil, Guyana, Canada, Qatar, and Norway.

US liquids supply, however, is expected to reach its peak around the end of the current decade, leading to an overall decline in non-OPEC production starting in the early 2030s, eventually reaching 69.9 million b/d by 2045. Guyana, Canada, Argentina, Brazil, and Kazakhstan are some of the few non-OPEC producers set to expand beyond the medium-term, but non-crude liquids including biofuels and other unconventional will also keep increasing.

OPEC liquids will rise steadily in the medium-term from 34.2 million b/d in 2022 to 37.7million b/d in 2028, and further to 46.1 million b/d by 2045. OPEC’s share of global liquids supply will therefore increase from 34% in 2022 to 40% in 2045. After US liquids supply, and thus non-OPEC liquids, peak in the early 2030s, OPEC liquids will continue to grow.

Investment requirements for the overall oil sector between 2022 and 2045 are estimated at a cumulative $14 trillion (in 2023 US dollars), averaging around $610 billion per year. Of this, $11.1 trillion is expected to be required in the upstream sector, or an average of $480 billion per year. Downstream and midstream requirements are estimated at $1.7 and $1.2 trillion, respectively.