Rystad: A US gas boom is coming

Natural gas production in the US is set to grow to a record 93,3 bcfd in 2022 and will continue to rise, exceeding 100 bcfd in 2024, according to Rystad Energy analysis. Performance of the country’s key gas basins will attract increased interest from investors and markets, as a result, with CO2 emissions intensity, capital efficiency, and potential bottlenecks drawing scrutiny, Rystad said.

US’s gas output reached a record 92.1 bcfd in 2019, but production subsequently declined to 90.8 bcfd in 2020 as a result of the COVID-19 pandemic. Rystad expects 2021 volumes to fall even further, to 89.7 bcfd, but the trend will quickly change as the effect of the pandemic subsides and activity builds across the major gas basins.

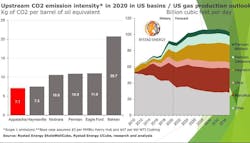

The Appalachian basin was the US’s lowest in 2020 in terms of CO2 emissions intensity, according to the analysis, and the region is set to report a record-high capital efficiency in 2021 as reinvestment to maintain output will drop to its lowest level. Meanwhile, the Haynesville will offer the largest gas output growth going forward, risking bottlenecks unless more pipelines are approved.

Appalachia

Looking at CO2 emissions intensity, the Appalachian region benefits from well-established and relatively modern infrastructure. With the considerable adoption of e-frac fleets, Rystad Energy’s Scope 1 upstream emissions analysis scores the Appalachia region as lowest in CO2 emissions intensity in the US, with 7.1 kg of CO2/boe in 2020.

“Such a level of CO2 intensity performance brings Appalachia to the top quartile among all oil and gas fields globally. As the basin becomes more mature and modern ESG best practices are implemented, we anticipate Appalachia to improve further in its CO2 intensity dimension in the next 3-4 years,” said Emily McClain, Rystad senior analyst.

The Haynesville follows with a CO2 intensity of 7.5 kg CO2/boe, Niobara with 10.6 kg CO2/boe, the Permian basin with 10.9 kg CO2/boe, south Texas’ Eagle Ford with 11 kg CO2/boe, and the Bakken with 20.7 kg CO2/boe.

Producers active in the Appalachian can also expect capital efficiency levels rise to a record high in 2021, Rystad Energy said, a trend that will continue in the years to come. To maintain production, Appalachian producers will need an upstream reinvestment rate of only 67% in 2021.

While the largest public independents in the region have historically managed to lock in relatively favorable derivatives positions, 2016 was the only year that the basin was able to deliver an upstream reinvestment rate under 100%, excluding the impact of hedging, financing activities, and midstream-related cash flows, according to Rystad estimates.

The pre-hedging upstream reinvestment rate increased to 147% in 2019 when the gas market was hit by a sudden downturn in second-half 2019. It stayed above 100% in 2020, moderating toward yearend with a combination of frontloaded capex and a gas price recovery in the year’s second half.

Upstream reinvestment rates look set to stay well below 100% across the basin, based on the new business models adopted by some of the largest and most well-established producers. In the base case, an average long-term upstream reinvestment rate of 75% for the Appalachian region going forward is expected.

Despite infrastructure bottlenecks, recent pipeline delays, and project cancellations amid exploration and production companies’ changing business models, total gas production in the Appalachian region has yet to reach its peak. In a base case scenario, Rystad anticipates 16% gas production growth before a final plateau is reached, with Marcellus and Utica forecast to add 5 bcfd over the next 2 decades.

However, the overall region’s contribution to the nation’s total will stay flat at 36% in 2035 compared to 2021. The Permian and Haynesville drive most of the incremental growth. Nevertheless, Appalachia will remain the dominant supplier given its remaining inventory of drilling locations.

Haynesville

The Haynesville is set to become the largest source of gas output growth in the US, forecast to add about 10 bcfd from 2020 to 2035, growing by 86% during that time. The region is forecast to account for about 21% of the country’s gas production in 2035, compared to 13% in 2020.

It remains poised to see production growth of 5 bcfd or more over the next 5 years based on a conservative level of drilling on the back of robust permitting activity, an expanding inventory of commercial locations that includes East Texas and the mid-Bossier, and improving 2-month initial production results, Rystad Energy estimated.

A key factor in Haynesville’s ability to sustain an advantage against the Appalachian region will be to maintain the relative ease with which operators can transport gas from wellheads to Gulf coast markets, compared to the bottlenecks and midstream project cancellations faced by producers in the Northeast.

Rystad’s analysis on Haynesville’s current and planned takeaway capacity noted that the basin has the capacity to sustain the forecast production growth up to 2024, the year when potential bottlenecks could start, unless new pipeline projects get approved.

As Haynesville’s second growth phase began and operators returned to previous record production numbers of the late-2019 boom, the system touched 90% utilization, the rate above which strain due to bottlenecks may occur. The LEAP, Index 99, and the CJ Express pipelines have since alleviated these potential strains, with utilization rates currently back near 70%.

The analysis visualizes scenarios that the system may face over the coming years. Under a scenario in which all new projects are approved, constructed, and brought online, and the Mid-Con stays at its currently forecast low levels, the system will stay at comfortably under 90% well into the medium term, providing sufficient capacity for a booming third growth phase.

If planned projects under review—including two Tellurian pipelines currently deferred—are ultimately not built and only Gulf Run’s additional 1.65 bcfd capacity is added, the system would touch a utilization rate near 90% by fourth-quarter 2024. Additional projects would be needed to continue growth into the decade’s second half.

If Gulf Run does not receive FERC approval, the system would return to an unsustainable use level by second-quarter 2024.

Lastly, if none of these projects are added to the basin’s capacity and gas production in the Mid-Con returns to historical peaks last seen in 2019, under current production forecasts, the basin’s pipeline capacity would not only hit the 90% mark, but become fully overutilized by 2024, Rystad estimated.

Significant gas volume growth from tight oil plays is expected, Rystad Energy said. Associated gas from the Permian’s Delaware and Midland regions will account for more than 5 bcfd of growth from 2021 to 2035, driven primarily by the Delaware. The US is forecast to supply almost 80% of North America’s total gas production, supported by these increases.