Stranded gas, diesel needs push GTL work

Interest in commercial gas-to-liquids (GTL) technology, limited for over 70 years to countries with political rather than economic drivers, has heightened in the past decade with now-monthly announcements of technical advances and commercial agreements, studies and demonstrations and front-end engineering and design (FEED) awards, and even a groundbreaking or two.1 Companies with commercial GTL histories, such as Sasol and Shell, as well as others including BP, Syntroleum, ExxonMobil, Rentech, and ChevronTexaco, have made advances in hardware design, catalysts, and operating conditions in an attempt to improve GTL economics. Certain governments, such as those of Qatar and California, have taken leading positions in developing and implementing GTL as a component of long-term strategies.

Key GTL products fall into the categories of fuels (primarily diesel but also LPG), specialty streams (lube base-stocks and waxes), and petrochemicals (naphtha for steam cracking). This article will examine these markets and the potential impact of GTL developments on the global and regional markets for natural gas and some of these products.

GTL basics

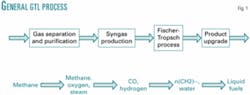

GTL technology involves the multistep, indirect conversion of methane to higher molecular weight hydrocarbons ranging from LPG to paraffin waxes, often controlled to peak in the diesel range (Fig. 1).

The first step after feed preparation and purification involves steam reforming and/or partial oxidation of methane to carbon monoxide and hydrogen. The key reactions include:

CH4 + H2O ↔ CO + 3 H2

CH4 + 1/2 O2 → CO + 2 H2

The synthesis gas is then converted to hydrocarbons in the Fischer-Tropsch (F-T) section with cobalt (with natural gas as feed) or iron-based (with heavy feeds such as coal) catalysts:

CO + 2 H2 → —CH2— + H2O

The liquid products are separated in the final upgrading section, which often also involves mild hydrocracking to convert higher molecular weight waxes and lubes to LPG, naphtha, and diesel.

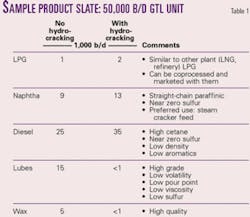

In modern variations, GTL unit designs and operations are modulated to achieve desired product distribution and a range of product slates. Certain operations (low temperature and/or no hydrocracking) result in primarily wax, lubes, and diesel products, whereas other conditions (higher temperature and/or mild hydrocracking) increase diesel, straight-chain paraffinic naphtha, and LPG at the expense of lubes and waxes.2 3 Wax and lube production typically ranges from zero to 30%, diesel from 50% to 80%, and the lighter products to as much as 25% of the final liquid products. The products are of generally high quality with near zero sulfur and high cetane for the diesel (Table 1).

For more detail on the GTL chemistry and processes, see reference 4.

The earliest commercial adoption of GTL was for use in the German World War II effort, with the second use in South Africa starting in the 1950s. These combined gasification with GTL to take advantage of coal resources.

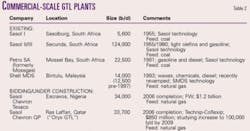

Three commercial units currently operate in South Africa (Table 2). Shell Bintulu (Malaysia) was built in 1993 and recently upgraded and expanded to approximately 14,000 b/d liquid product capacity. One plant (Oryx in Qatar) is under construction, another (Escravos in Nigeria) is at an advanced stage of bidding, and a large number of other facilities are at the study, planning, and design stages.

Given the low value of stranded gas and the premium expected for clean GTL diesel and heavier products, which will be discussed, a key determinant to the profitability of new GTL facilities is the capital cost. Historical capital costs of in excess of $50,000/bbl (total installed costs) have dropped due to technical advances to $25,000-30,000/bbl with $20,000/bbl in sight and even smaller numbers considered.5 Shell's stated goal is to reduce the cost to $12,000/bbl. There have been reductions in reactor size, improved catalysts, advances in temperature control using fluidization and hardware design, and optimized operating conditions.6 7

Synergies are also considered, including integration with power generation8 or hydrogen manufacture,9 while some GTL is driven by supply of coal, low value petcoke, bitumen, and Orimulsion. 9 10 There are also less well-known but promising technologies in the pipeline.11 12 13

Several factors have resulted in the interest in GTL and its variations over the past 2 decades. These include:

- Need to develop and exploit additional energy resources.

- Existence of large reserves of stranded natural gas and the attempt to monetize them.

- Desire for strategic diversification on the side of both producers and consumers.

- Environmental drivers ranging from a movement to reduce flaring to auto-emission regulations.

A number of consuming and producing countries have come to consider GTL as one component in a strategy of diversification and growth. On the producing side, Qatar can serve as an example. With current proven reserves of about 15 billion bbl of crude and production of 700,000-750,000 b/d, Qatari oil is depleting with a possible production decline to 500,000 b/d by 2012 and the commensurate loss in revenues.

Consuming countries also have an interest in diversification and enlargement of supply. Given the many political and social uncertainties in the Persian Gulf region (which could potentially translate to commercial and regulatory uncertainty), it is noted that about 65% of the world's crude, but only 36% of its natural gas reserves, are located in the Middle East. About 30% of the world's natural gas is located in the Russian Federation, with the rest in Asia Pacific, Europe, the Americas, and Africa.

At the same time, the projected rapid economic growth in the Asia-Pacific region, particularly the much talked-about need of China for energy during the first half of the 21st century, along with the decline in a number of existing oil fields, requires rapid entry of new energy resources including natural gas into the market.

Economics and markets

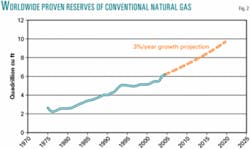

Worldwide proven natural gas reserves stand at about 6,100 tcf15 with approximately 3,000 tcf considered stranded. Much of GTL economics is dictated by significant new stranded natural gas finds. Of these new finds, some are very large, such as Qatar's North field (900 tcf proven reserves) and Iran's South Pars field (500 tcf). However, a segment of the natural gas of interest, particularly gas produced with crude oil, has been known of for decades but not exploited. For example, Nigeria flared 620 bcf of natural gas in 2000.16 Overall, reserves are expected to grow as, aside from one 5-year period during the past 50 years, discovered natural gas has far outpaced volumes brought on stream (Fig. 2).15 17

Unconventional sources are also of interest. Some, especially coalbed methane and gas from tight formations, and to a lesser extent basin-center aquifer gas, have been or are in production in countries such as the US, UK, and Australia. Another unconventional source, methane hydrates, found in colder regions such as Canadian, US, and Siberian permafrost, are of great interest due to their very large estimated amounts. The current consensus estimate of gas in place as hydrate, 600,000 tcf, is around 100 times larger than proven conventional reserves of natural gas.

Worldwide consumption of natural gas stood at 89.4 tcf/year in 2002,18 equivalent to about 45 million bbl of crude. Much stranded gas is reinjected, used as plant fuel, or, if associated with oil, flared if produced or kept in the reservoir, which limits crude production. For example, certain oil and gas reservoirs in Siberia are produced at a low rate due to the absence of an outlet for the natural gas.

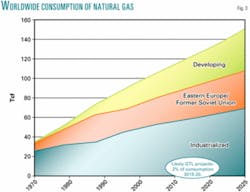

Compared to the total consumption of natural gas, existing LNG and GTL facilities are small. Globally, GTL units use 130 bcf/year and LNG units 7.2 tcf/year, which together represent 0.12% of proven gas reserves and about 8% of global annual gas consumption (Fig. 3). Although there are nearly 50 GTL facilities under various states of consideration with potential gas capacity of 4-5 tcf/year, observers believe that, at most, only half of this capacity (about 2.2 tcf/year) is likely to come on line in the next 10-15 years. This is approximately 2% of projected total gas consumption between 2015 and 2020.

In key regions, numbers differ, but our analysis suggests that unless there is surprising growth in the number and capacities of GTL facilities, it is unlikely that GTL will increase demand for stranded natural gas enough to increase the value of the gas in the field. In large fields, particularly, it is feasible to operate multiple GTL plants alongside LNG or other gas monetization units.

Slow growth

It is interesting to note that growth in GTL capacity has been slower than optimists of the mid-1990s projected. Causes include:

Recession of the late 1990s and low crude prices.

LNG as a fierce competitor for capital.

Slow pace of negotiations due to technical and economic unknowns, issues of regulatory stability, and evolving financial structures.

Furthermore, gas that is not stranded (in or with access to markets) is of significantly higher value—$5/MMbtu for Japanese imports in 2002, for example—and as such will not be suitable as GTL feedstock. A number of studies show that for GTL to be viable, the gas cannot be valued above 50¢/MMbtu, which is in the stranded gas range and similar to values assumed for LNG.19

Given the availability and likely low value of stranded gas, a key factor will be availability of and competition for capital. A number of studies have compared the full GTL and LNG trains and found that, for modern units with $20,000-30,000/bbl cost, GTL is competitive with LNG.2

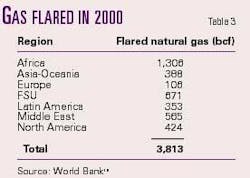

One key factor driving GTL and LNG is the global attempt to reduce flaring of natural gas in associated fields. As a recent World Bank study shows,16 the total worldwide flared gas in 2000 was estimated at 3.8 tcf with a particularly high ratio of flared gas to oil produced for a number of African countries (Table 3). Indeed, a key factor in the Nigerian decision to pursue GTL has been the attempt to reduce flaring.

Diesel from GTL

The most intriguing and important GTL product, one that has been studied extensively and one that warrants focus here, is diesel-range material.

Automotive diesel market

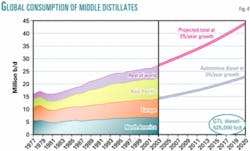

The global middle-distillates market, at about 27 million b/d, is a significant portion of the worldwide fuels market with a history of about 3%/year average growth during the past decade (Fig. 4). Of this, about 14 million b/d is automotive diesel. Europe has the largest diesel market, with demand of 3.4 million b/d; followed by Asia-Pacific, 3 million b/d; and North America, 2.8 million b/d.

These numbers are expected to continue to grow, largely driven by increased diesel-powered auto sales. For example, Schmidt's Automotive Industry Data (AID) estimates that the sale of such vehicles in Europe will grow from approximately 6 million units in 2002 to over 8 million by 2008, constituting over 60% of sales in countries such as France and Austria.2 The increase in Europe is mediated by a combination of emission mandates, jurisdictional tariff strategies, improved auto designs, and increased availability of low-emission fuels.

The automotive diesel market in the US is noticeably smaller, with diesel-powered light vehicles representing less than 4% of the total US auto market.20 As a result, the diesel market in the US is primarily driven by the commercial sector and is thus tied to overall economic growth. The growth in US diesel demand has averaged about 5%/year during the past decade.21 Regional and regulatory efforts are likely to increase diesel usage in the US during the next decade. These include activities and studies by the California Energy Commission, California Air Resources Board, and US Department of Energy.22 A number of fleets (light as well as heavy) have tested or shifted to clean diesel (including GTL and biodiesel blends) in various parts of the US with potential impact on long-term attitudes and trends.23

Growth in Asia-Pacific has been rapid yet uncertain and is expected to remain so. During the first half of the 1990s this growth stood at about 7%/year but slowed to under 3%/year in the recession years that followed. In a number of countries diesel-powered automobiles form a large fraction of the vehicles (for example, Japan at 20%). With the rapid developments in China, it is likely that growth will remain above 3%/year.

Globally, one observer suggests an increase in the proportion of diesel automobiles (including biodiesel and GTL) to 40% over the next few years from the current average of 30% relative to gasoline-powered cars, followed by partial replacement with hybrid technologies over the following decade.23 Based on overall economic growth and regional trends, observers anticipate demand for middle distillates (incorporating automotive diesel) to continue growing at 3%/year,21 from 27 million b/d currently to 44 million b/d by 2020. Of the 2020 demand level, 22.5 million b/d is projected to be automotive diesel.

GTL diesel supply

The projected numbers for GTL liquid product barrels are subject to great uncertainty. All GTL projects existing or under various stages of consideration represent total liquid product capacity of perhaps 1.8-2 million b/d.1 Some examples: Iran has had four studies. Nigeria has a number of agreements, some in advanced stages. Several studies point to GTL as a significant option for monetizing stranded gas in northern Australia. And Qatar alone is considering a liquid product capacity of 750,000-900,000 b/d by 2012-15, nearly 70% of which is likely premium diesel stock suitable for use as automotive diesel-blend material.

However, only a fraction of these potential capacities will likely come on stream in the foreseeable future. A study for the California Energy Commission estimates total worldwide GTL diesel capacity at about 75,000 b/d in 2010, 388,000 b/d in 2015, and 800,000 b/d by 2020.7 Sasol Chevron suggests 600,000 b/d of GTL diesel capacity by 2016. 19, 24

A quick example: Let us assume total GTL liquids of 750,000 b/d by 2020. At 70% diesel yield, this produces approximately 525,000 b/d of diesel fuel. This is expected to be less than 3% of the total worldwide automotive diesel market (Fig. 4). We thus expect a relatively small chance of oversupply caused by the introduction of GTL.

From a local point of view, however, GTL products could form a significant portion of a region's diesel consumption. For example, Shell estimates that one large-scale GTL plant would fully satisfy the city of London, while 10 such plants would produce enough pure GTL diesel for the entire US Petroleum Administration for Defense District V.23

It is possible, therefore, to develop a critical mass of available GTL diesel blendstock for a small market. As an example, GTL diesel from Shell Bintulu has been offered throughout Thailand in the past 2 years as a 30% blend in the premium grade Pura. Shell also has been very aggressively working with a number of governments in Asia, particularly China and Japan, to boost demand for blends of GTL and conventional diesel.

Regulatory environment

Emission standards for heavy and light-duty diesel vehicles have tightened or are expected to tighten considerably in a number of regions. These standards have produced emission or content limits on sulfur, particulates, aromatics, polynuclear aromatics (PNAs, impacting particulates), and nitrogen oxides.

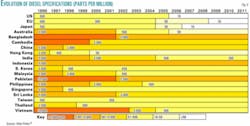

In the European industrial countries as well as Japan and the US, sulfur-content limits have evolved toward the 10-50 ppm range (Fig. 5). At the same time, a number of other countries, including many in the developing world, have introduced new and more restrictive mandates of 200-1,000 ppm.

Aside from sulfur, PNAs are regulated in Europe at 11 wt % with restrictions on particulates, aromatics, and NOx upcoming or under study in a number of jurisdictions.

GTL diesel is virtually sulfur-free and primarily paraffinic (very low aromatics, less than 5% PNA content) and therefore has come to be considered a potentially important blending element in satisfying environmental and auto emissions requirements.

A number of studies have demonstrated emissions improvements resulting from use of GTL diesel (neat or in blends) not only compared to conventional high-sulfur diesel, but also low-sulfur, low-aromatics refinery diesel. For example, one study suggests 40-50% reduction in the emission of hydrocarbons, 9% in NOx, and 30% in particulates when compared to low-sulfur refinery diesel.25 Another study estimates significant emissions benefits for light-duty and heavy-duty vehicles with current engine technology and 100% GTL diesel23 as well as with new engine technologies (Euro-4 and Euro-5) and using 15-30% GTL diesel blends.

Though tailpipe emissions with diesel GTL are significantly lower than with conventional refinery diesels, these benefits can be less pronounced from a well-to-wheel (WTW), greenhouse gas point of view. For example, a US study shows that the WTW CO2 emissions of refinery diesel was actually slightly lower than that of diesel from natural gas and F-T (460 g/mile of CO2 vs. 480 g/mile)23 with the great benefit of GTL, in such case, being that the lion's portion of the CO2 is produced far from population centers (not as auto emissions but as plant emissions) and can therefore be relatively easily sequestered and dealt with.

In addition to content and emission specifications, a number of jurisdictions have structures mandating or encouraging the incorporation of "alternative" fuels. These include the European Commission legislative proposals with mandatory targets for biofuels, natural gas, and hydrogen26 and the US Energy Policy Act of 1992 (applied to domestically produced GTL fuels in 2000).23

Quality, pricing issues

GTL diesel, in addition to having low sulfur and reducing emissions, is highly paraffinic, resulting in cetane numbers of 70-80. Further, it typically has lower density than refinery diesel (0.77-0.80 kg/l. vs. 0.83-0.85 kg/l.), resulting in a "density premium."

Diesel containing GTL blendstock is currently sold commercially in Thailand, Greece, Germany, and South Africa.

Though contemplated also in pure form, for a number of reasons it is found to be more practical as blendstock. These include:

- The lower density (and associated lower T90) results in a perceived lower fuel efficiency (miles per gallon) when compared to standard diesel.

- Pure GTL diesel would require separate infrastructure and some modifications of the automobile. This would take away a key benefit of GTL: that its fuel is compatible for use with current fuels and as an excellent transition fuel as regulations and markets develop for other, more radical alternatives.

- GTL diesel has relatively poor cold-start properties. This is less of a problem in warmer climates but nevertheless must be accommodated.

- In jurisdictions with very tight sulfur-content specifications (10-50 ppm, for example), the volume of GTL diesel required for diluting the sulfur in conventional diesel needs to be very high.

As a result, GTL diesel is most likely to be used in:

- Blending to bring off-specification diesel into compliance in jurisdictions with relatively lax specifications or where the base blend is close to specifications. For example, most of the 24,000 b/d of Qatar's Oryx GTL diesel is likely to be used as blendstock in Europe to bring conventional refinery diesel to specifications.

- Blending to bring certain refinery intermediate streams such as the FCC heavy cycle oil into diesel specification to avoid the alternative use of the FCC heavy cycle oil as heavy fuel oil product blendstock.

A number of studies, during the 1980s and 1990s and in the context of refinery hydroprocessing requirements, suggested a 5-10¢/gal premium for low sulfur diesel when compared with standard diesel. Such numbers have since been found reasonable for GTL diesel as well in light of the low sulfur, low density, and high cetane of GTL diesel. Commercially, for example, Shell's Pura brand diesel is sold at a premium relative to standard brands in Thailand.

However, as applied to sulfur, competition exists. Over the past 2 decades, the ability of refiners to reduce sulfur in products has improved dramatically, thanks in large part to construction of hydrotreaters and hydrocrackers in a very large number of refineries, but also to improvements in FCCs and other units. At the same time, biofuels, such as methyl esters and ethanol, though a small proportion at this time, are expected to grow in light of tax benefits in the US as well as mandates in a number of regions. Therefore, it is possible that the sulfur premium for GTL diesel might erode in years to come, although this possibility is mitigated by the anticipated increase in demand for both high and low sulfur diesel.

Some observers suggest that GTL diesel's premium will develop primarily because of its high cetane and low aromatics. If so, the GTL diesel will be more attractive in Europe than in the US or Asia due to the former's more restrictive cetane and aromatics specifications.

Other markets

While diesel-range material is the largest and most important, other markets exists for GTL products, including lubes, waxes, and naphtha.

Lubes market

Increased demand for high quality lubes (Group III/IV) and a projected increase in global demand for all lubes from 720,000 b/d in 2002 to 820-850,000 b/d in 2010)2 27 have stimulated efforts to bring new lubes hydroprocessing capacity on stream. Worldwide hydroprocessed base-stock capacity is projected to grow well beyond the demand of about 250,000 b/d.28 This and other factors have put downward price pressure on premium stocks, which may well continue into the next decade.

The heavy paraffins produced by GTL have virtually no sulfur and low viscosity, pour point, and volatility and make excellent lube base stocks when compared with products from conventional solvent processing. However, due to the small size of the lubes (and premium stocks) market, even one world-scale GTL unit (50,000-100,000 b/d total liquids with as much as 15,000-30,000 b/d of lubes) can provide a significant fraction of the worldwide demand for premium base stocks (on the order of 6-12%). Unmitigated, a handful of such units could exert additional downward pressure on the price of premium base stocks. The Exxon

Mobil project announced last year in Qatar alone is expected to deliver about 30,000 b/d of lube stocks into the market. An assumed worldwide GTL capacity of 750,000 b/d by 2020 could, in the worst case, result in a glut of over 200,000 b/d additional premium lube base stocks. ExxonMobil estimates that the introduction of high-quality base stocks from GTL could not only exert price pressure on very high viscosity index (VHVI) base stocks, polyalphaolefins, and lubes in Groups III and IV but also eventually on the conventional lubes of Groups I and II.

Because of this, the majority of the GTL plants under construction or planning include a product-cracking step in order to reduce the volume of lubes produced via conversion to the diesel and lighter range.

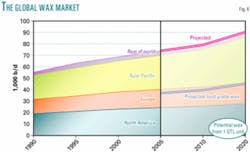

Wax market

Most of the paraffin wax in the world is currently supplied by refineries in the form of slack wax, which is subsequently refined by removing oil, aromatics, and sulfur into a range of products such as scale waxes, refined paraffin waxes, and microcrystalline waxes. The total global wax market is about 70,000 b/d, of which half is for food-grade waxes. The US market is 25-30% of the worldwide market.29

Growth in the market has been steady over the past 25 years, and models suggest this steady growth in demand should continue for the next 15 years (Fig. 6).

Two existing GTL plants, the Shell Bintulu and Sasol Secunda facilities, provide about 17% of worldwide petroleum waxes. These include food-grade derivatives and are of high quality.

At the same time, industry insiders think that the number of refineries willing to produce wax will be reduced as the manufacture of waxes is operationally difficult. For example, Chevron reduced its presence in the wax market in 2001. Regardless, as with the case of lubricants, the wax market is very easily overwhelmed due to its small size. For example, one typical GTL plant with total liquid production of 50,000-100,000 b/d could potentially produce as much as 5,000-10,000 b/d of high-grade wax, 6-11% of the total global wax market in 2015. As a result, most GTL plants are likely to opt to hydrocrack their wax-range products into diesel and naphtha.

GTL naphtha

GTL naphtha is highly paraffinic (primarily straight chains, low octane) and low in aromatics, making neither good gasoline blendstock nor a suitable refinery catalytic reformer feed. Rather, it is an excellent feed for steam crackers to produce ethylene and other olefins. In fact, due to its paraffinicity and purity, GTL naphtha yields more ethylene than does refinery naphtha. There are indications that the Asia-Pacific region is likely the strongest future market for GTL naphthas due to the rapid growth of the petrochemicals sector in that region.

Drivers and effects

The potential growth in GTL is, in large part, driven by the need to monetize large reserves of stranded natural gas along with the increasing demand for liquid products with tighter specifications. GTL technology is one component in the strategy by various parties to meet these demands.

We find that, given the commercial state of the technology and its anticipated growth during the next 10-15 years, GTL is unlikely to cause significant disturbance to the diesel market but, if unchecked, might increase the inventories of slack wax and high-quality lube blendstock so as to bring downward pressure on their prices. F

Acknowledgment

Discussions with and assistance from Barbara R. Shook of Energy Intelligence Group is gratefully acknowledged.

References

1. See http://gmaiso.free.fr/lng/.

2. Redeker, D., Gas to Liquids Euroforum, Paris, February 2003.

3. Cee www.chemlink.com.au/gtl.htm.

4. Rahmim, I. I., "The Promises and Limitations of Gas-to-Liquids Technology," Global Forum on Natural Gas, Galveston, Tex., May 2004.

5. Crouch, A., "GTL: A New Era," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

6. Rahmim, I. I., "Gas-to-Liquid Technologies: Recent Advances, Economics, Prospects," 26th IAEE Annual International Conference, Prague, June 2003.

7. Waddacor, M., "Modern-day Gas Alchemy Yields Cleaner Fuels," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

8. Gray, D., Tomlinson, G., "Potential of Gassification in the US Refining Industry," report to the Department of Energy, June 2000.

9. Gray, D., Tomlinson, G., "Opportunities for petroleum coke gasification under tighter sulfur limits for transportation fuels," 2000 Gasification Technology Conference, San Francisco, October 2000.

10. Bohn, M. S., Benham, C. B., "A comparative study of alternate flowsheets using Orimulsion as feedstock," 25th International Technical Conference on Coal Utilization and Fuel Systems, Clearwater, Fla., March 2000.

11. Oder, R. R., "Magnetic Separation of Iron Catalysts from Fisher-Tropsch Wax," ACS Annual Meeting, Anaheim, Calif., March 2004.

12. Venkataraman, V., Gray, D., "Applications of Ceramic-Membrane Technology," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

13. Zhou, Z., Zhang, Y., Tierney, J. W., Wender, I., Petroleum Technology Quarterly, Winter 2004.

14. Bevan, H., Oxford Energy Forum, August 2004.

15. US Energy Information Administration, "International Energy Outlook," 2004.

16. "Report on Consultations with Stakeholders," Global Flaring Reduction Initiative, World Bank in Collaboration with the government of Norway, 2001.

17. Chew, K., "The World's Gas Resources," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

18. "BP Statistical Review of World Energy," 2003.

19. Hill, C., "What makes a natural gas to liquid fuels project viable?" Middle East Petroleum and Gas Conference, Dubai, March 1998.

20. GTL Working Group Analysis, California Energy Commission, Sacramento, Calif., Oct. 12, 2004.

21. Birch, C., "The market for GTL diesel," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

22. Pytte, T., "Global trends in transport fuels and the role of natural gas," Australia Institute of Energy, Perth, October 2003.

23. Cherrillo, R. A., Clark, R. H., Virrels, I. G., "Shell gas to liquids in the context of a future fuel strategy—technical marketing aspects," 9th Diesel Engine Emissions Reduction Workshop, Newport, RI, August 2003.

24. Van Rheede, J., Oxford Energy Forum, August 2004.

25. Venkataraman, V. K., "Overview of gas-to-liquid programs: its role in ultra-clean transportation fuels intitiative and commercialization strategy," Workshop on Alternative Fuels for Ferries and Other Vessels, Almeda, Calif., November 2000.

26. Klein, S. R., "GTL policy and the path forward," in "Fundamentals of Gas to Liquids," Petroleum Economist, January 2003.

27. Markarian, J., Chemical Market Reporter, Vol. 263, No. 17, Apr. 28, 2003.

28. Cox, X. B., Burbach, E. R., "The outlook for GTL and other high quality lube basestocks," NPRA Annual Meeting, New Orleans, March 2001.

29. EIA, Petroleum Supply Monthly, October 2001.

The author

Iraj Isaac Rahmim ([email protected]) is president of E-MetaVenture Inc., a consulting and training firm working in the areas of natural gas and oil processing technology and economics. He holds BS and MS degrees from the University of California and a PhD from Columbia University, all in chemical engineering.