Oil supply challenges-2: What can OPEC deliver?

The first part of this two-part series appeared Feb. 21, 2005, p.20.

The global market will need increasing volumes of oil from members of the Organization of Petroleum Exporting Countries after non-OPEC production reaches a maximum of about 50 million b/d between 2007 and 2011 (see Fig. 7, OGJ, Feb. 21, 2005, p. 28). Predicting future OPEC production potential is subject to considerable uncertainty as it depends on a number of interrelated factors:

• The near and medium term (to 2020) demand for oil.

• Non-OPEC production.

• OPEC oil reserves.

• The timing and scale of investment decisions to increase production capacity in the Persian Gulf OPEC countries.

• The ability of OPEC’s mature oil fields to increase production capacity.

A question crucial to future oil supply, therefore is: Can OPEC’s old fields deliver?

Persian Gulf producers

Most of OPEC’s remaining oil reserves (80%, some 700 billion bbl) and future production potential are in the five Persian Gulf oil-producing countries: Saudi Arabia, Kuwait, the United Arab Emirates, Iran, and Iraq. These producers share the following characteristics (see also Fig. 1a):

• Supergiant oil fields provide most of the oil production and future oil production potential.

• Most of these oil fields have been on production since the 1950s and 1960s, and many have been on plateau production since the 1970s.

• The fields discovered in the 1940s to 1960s are 35-55% depleted. Average OPEC depletion is some 30%.

• Since the 1980s, most of the fields have been conserved at low offtake rates, typically less than 2%. This compares with offtake rates of the Prudhoe Bay oil field of nearly 5% and of Forties of more than 7%.

• The initial production rate from new wells has declined from tens of thousands of barrels per day in the 1960s and 1970s to thousands of barrels per day today.

• Most of the supergiant oil fields have had water or gas injection installed to maintain pressure for 20-30 years. Handling produced injection fluids is a growing problem in Iran, Saudi Arabia, the UAE, and in older fields in Iraq (Kirkuk, Zubair, and Rumailah).

• The published plans of the state oil companies in the region indicate extensive deployment of infill drilling, multilateral and horizontal wells, and enhanced oil recovery technologies, in line with the mature nature of their oil fields.

The fundamental importance of reservoir quality, field size, and maturity of producing fields can be illustrated by taking a closer look at each of these countries.

Saudi Arabia

Oil was discovered in Saudi Arabia in 1938, and the country began producing oil in the same year.

Supergiant Ghawar oil field was discovered in 1948 and has been on production since 1951. The field has been on plateau production of 3-5.5 million b/d since 1972. Ghawar oil field had produced 57 billion bbl by end 2003 and has published remaining recoverable reserves of some 70 billion bbl, roughly the same as the original recoverable oil reserves of the North Sea.1 The field is more than 40% depleted. In 1975 the field started producing water, and in 2003 the field produced 5 million b/d of oil and 1.7 million b/d of water-a 30% water cut.

After more than 30 years of plateau production, the effects of reservoir architecture and the complex and not always predictable patterns of movement of injected water are now becoming more and more manifest in production. Initial well rates in the 1970s averaged tens of thousands of barrels a day, but new wells drilled today average thousands of barrels per day. Abdul Baqi and Saleri report an extensive program of infill drilling (horizontal and multilateral wells) at Ghawar, supporting the view that the field is now mature and that maintaining existing production levels is a technical and investment challenge.

More than 70% of Saudi Arabia’s original oil reserves, some 350 billion bbl with 700 billion bbl in place, are contained in supergiant fields with original recoverable reserves greater than 5 billion bbl. These same fields have provided 97% of the oil production to date. Saudi Aramco uses a 50% recovery factor to estimate its remaining proven oil reserves estimate of 262.7 billion bbl. Given the concentration of reserves in supergiant oil fields, this is not unreasonable and in line with world averages.2

In 1985, the published oil-in-place and “proven” reserves gave an average recovery factor of 37%.1 3 Based on the published information and the relatively high recovery factor of 50% used by Saudi Aramco, the reported “proven” reserves of Saudi Arabia should probably be considered as proven plus probable from the discovered fields.

Iran

Oil was discovered in Iran in 1908, and production started in 1913.

Iran’s largest oil field, Ahwaz, began production in 1960 and has been on plateau production of 400,000-1 million b/d since 1972. The initial reserves have been estimated at 25.4 billion bbl, of which 9.4 billion bbl had been produced to the end of 2003. The field is 37% depleted.

The recently revised estimate of “proven” oil reserves for Iran of 130 billion bbl (including about 20 billion bbl of natural gas liquids) indicates an average recovery factor of 33% from oil in place of 560 billion bbl.4 Like those of Saudi Arabia, 70% of Iran’s original oil reserves are contained in supergiant fields.

The lower average recovery factor for Iran suggests that Iran has considerably more potential for reserves growth in existing fields than Saudi Arabia. While this is probably partly true, the difference in recovery factor also reflects the larger number of smaller fields in Iran (fields with less than 1 billion bbl of reserves) and significant differences in reservoir quality. Saudi Arabian oil reserves and production are mainly from the Jurassic Arab D carbonate, which is a relatively simple, high-porosity, high-permeability reservoir where high oil recoveries can be expected. Iran’s oil reserves are mainly in the tight, fractured Tertiary Asmari limestone and the strongly layered, occasionally fractured, tight carbonates of the Cretaceous Bangestan Group. Recovery factors of about 40% seem likely to be the upper limit for large oil fields with these reservoirs.

In the giant Ahwaz oil field, the high porosity-permeability Asmari sandstone is expected by National Iranian Oil Co. (NIOC) to yield a recovery factor of 64%, whereas the poorer reservoirs of the Bangestan Group are expected to yield recovery factors of around 20%.4 A detailed field-by-field analysis of Iran suggests that the published estimate of “proven” reserves is a good estimate of the proven plus probable from the discovered fields.5

As in Saudi Arabia, initial well rates in Iran have fallen from tens of thousands of barrels per day in the 1970s to thousands of barrels per day today. Most of Iran’s large fields have been pressure-supported by gas injection for some 20 years and infill drilling programs active for more than a decade. Water production is an increasing problem in all of Iran’s major oil fields.

Iran has had success in adding new reserves through exploration, particularly in the Abadan Plain bordering Iraq. The Azadegan and Yadavaran oil fields have added about 10 billion bbl of reserves over the last 7 years. However, these fields have relatively poor reservoir quality (layered, low-permeability carbonates of the Bangestan Group) and relatively heavy oil (less than 28˚ gravity).

Iran has considerable potential to add new reserves through field extensions in the main producing areas of Khuzestan and exploration, particularly in the Abadan Plain and the deep waters of the Caspian Sea.

Kuwait

The Greater Burgan oil field produces 1.5-1.8 million b/d, about 75% of Kuwait’s oil production. The field was discovered in 1938 and has been on production since 1946. It has produced at a plateau rate of 1.5-2.5 million b/d since 1960.

The Burgan sandstone reservoirs are prolific, and there is a strong aquifer which seems to support the reservoir pressure at offtake rates of less than 1.5 million b/d. The field has 400-500 wells producing 4,000-5,000 b/d/well. After more than 40 years of plateau production, remaining reserves are estimated to be 70 billion bbl-about 75% of Kuwait’s published reserves-and the field is probably 40% depleted.

Kuwait is keen to reduce offtake at the Greater Burgan field to 1.2 million b/d to conserve the field and to allow reservoir pressure to recover. This objective is compromised by the slow pace of development of additional production capacity through the implementation of advanced reservoir recovery practices in the smaller and more complex reservoirs of Kuwait’s northern oil fields (Raudhatain, Sabriyeh) and Minagish, with combined remaining reserves of about 14 billion bbl.

Iraq

Oil was discovered in Iraq at Kirkuk field in 1927. Rumailah field (north and south domes) was discovered in 1953. These two fields have accounted for more than 70% of Iraq’s total production capacity.

Kirkuk has been on production since 1934 and on plateau of more than 1 million b/d since 1968. Rumailah started production in 1954 and reached 1 million b/d output in 1988. These fields are believed to be 40-50% depleted.

Rumailah in particular, with its complex clastic reservoirs, seems to have suffered from overproduction in recent years. Excessive production combined with complex reservoirs has caused heterogeneous pressure depletion, water breakthrough into producing wells in the best reservoirs, and the creation of isolated pockets of bypassed oil. Restoring and maintaining production levels from these fields will be a challenge.

Iraq has considerable potential in undeveloped oil fields. East Baghdad, Majnoon, West Qurna, Nahr Umr, and Halfaya oil fields probably have combined remaining proven reserves of more than 60 billion bbl. However, the reservoir quality of these fields is relatively poor, particularly in Majnoon and Nahr Umr close to the Iranian border.

The oil fields of Iraq are the least depleted and least developed of any of the Persian Gulf oil producing countries, and Iraq has the potential to rapidly increase oil output.

The UAE

Oil was discovered at Bab field in 1960, and production started in 1962 from Bu Hasa field. Six fields (Bu Hasa, Zakum, Bab, Asab, Fateh, and Umm Shaif) provide 75% of the UAE’s oil production.

These fields have been at plateau rates since the mid-1970s. Reservoirs are strongly layered, low-permeability carbonates with limited aquifer support. Most of the UAE’s oil fields have extensive water or gas injection programs, and horizontal wells are widely deployed.

Published proven oil reserves are 97.8 billion bbl, which suggests a low depletion of 20% as about 25 billion bbl had been produced to the end of 2003.3

Production challenges

Published OPEC reserves figures are assumed to equate to “most likely” estimates of remaining reserves, combining both proven and probable categories for discovered oil fields: i.e., some 882 billion bbl of ultimate remaining reserves (URR) of oil at the end of 2003.

It has been asserted that these published reserves are either grossly inflated or refer to original and not remaining reserves.6 However, where more detailed field data are available and analysis undertaken, particularly for Iran and Saudi Arabia, they broadly confirm that the published proven are probably equivalent to the remaining proven and probable reserves.1 4 5 It may be argued that possible overestimates of Saudi Arabia’s reserves are compensated by the generally accepted underestimation of Iraq’s oil reserves. Iraq is the least depleted of OPEC countries.

Real reserves increases are still possible in OPEC countries. These may be added by exploration success, increasing recovery factors, and proving up NGLs and condensate as markets access gas reserves. Fig. 1 indicates estimates for these potential additions, which could take OPEC’s remaining oil reserves to about 1.2 trillion bbl.

Combined with earlier results, these predictions for OPEC yield an estimate of the world’s ultimate recoverable oil reserves of 2.5-2.9 trillion bbl, with 1.29-1.66 trillion bbl remaining (1.224 trillion bbl produced to end 2003).

In many respects the question whether OPEC can deliver is as much an issue of the capabilities of mature oil fields, political will, and investment rate as it is of oil reserves. It seems unlikely that OPEC can increase production at the rate that was possible in the 1960s and 1970s, when the fields were fresh and initial well production rates were higher. Saudi Aramco has a maximum production-rate case of 15 million b/d.7 While this seems low, given the reserves, it may well be realistic given Saudi Aramco’s knowledge of its reservoirs and their capability. A detailed analysis of Iran’s oil fields suggests 7 million b/d may be the maximum rate achievable for Iran in the future without further discoveries.5 Only Iraq has undeveloped supergiant oil fields (West Qurna, Majnoon, and East Baghdad) and the potential to rapidly increase production to 8-10 million b/d.

Politics, economics

There are also political and economic factors to consider. OPEC countries will certainly generate sufficient oil revenues to invest in the required new capacity. However, they have other demands on state revenues, and the Persian Gulf producers will have to show greater alacrity in decision-making than they have demonstrated to date.

The five Persian Gulf countries (Saudi Arabia, Iraq, Iran, Kuwait, and the UAE) are crucial to raising OPEC production. The political situation in Iraq is unlikely to be conducive to major investment in new oil production capacity for some years. Saudi Arabia has serious internal problems, which threaten to destabilize the ruling Saudi royal family. Iran remains under unilateral US sanctions. US military intervention in the Persian Gulf and its failure to effectively and fairly engage in resolving the Palestinian-Israeli conflict conspire to provide a hostile backdrop to western interests in the Middle East. The combination of burgeoning future oil revenues and growing hostility to the US in the region is not conducive to major capacity expansion and will not provide a stable investment environment or offer easy opportunities to the major international oil companies to assist in any capacity expansion projects.

Based on these considerations and the maturity of OPEC’s major fields, it seems more likely that OPEC’s considerable reserves will be expressed as a long plateau rather than a sharp peak. It is quite possible that the Persian Gulf countries will not raise production capacity high enough or quickly enough, either for political reasons, the slowness of internal decision-making, or the hostile security environment. The consequences of this for world oil supply, the world economy, and world security are immense, with the likelihood of further military interventions and conflicts within the Middle East.

While this doom scenario is possible, it seems more likely that the Persian Gulf countries will raise production capacity, albeit slowly and constrained by reservoir realities and political and logistical factors. Consequently, for the purpose of this article, OPEC’s maximum production potential has been set at 50-55 million b/d for its published remaining oil reserves of 882 billion bbl, and 60-65 million b/d for the higher remaining oil reserves of 1.2 trillion bbl. These production levels yield about 50% depletion at the predicted peak rates in 2025 (Fig. 1b)-an assumption that seems reasonable.

These constraints yield a future rate constant for the logistic equation of 0.07, which compares with the 0.12 achieved by OPEC between 1911 and 1973.

Even reaching these production levels will require an immense effort in the immediate decade.

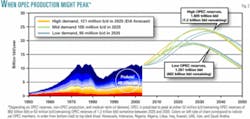

OPEC's peak

OPEC production is expected to peak at about 52 million b/d around 2025 for all demand cases for low OPEC reserves (Fig. 2). If OPEC reserves are high, OPEC production is expected to peak at about 65 million b/d around 2030.

It is unlikely, except in the high reserves case, that OPEC production will be able to meet the high demand forecast of 121 million b/d for 2025 by the US Energy Information Administration.8 OPEC is able to meet mid-demand growth (about 1.5%/year) until 2013-15 if OPEC’s oil reserves are low or until 2017-20 if OPEC’s oil reserves are high. OPEC is able to meet low-demand growth (about 1%/year) until 2020 under either reserves scenario.

These forecasts suggest world oil demand is likely to be dampened by a rising oil price due to supply constraints, particularly after non-OPEC production peaks (2007-11), but also when OPEC production increases start to tail off. This could occur in 2010-15 if OPEC’s reserves turn out low or around 2015-20 if OPEC’s reserves are high.

Oil supply will become increasingly concentrated in the Middle East and the former Soviet Union. The proportion of oil production from the main producers of the Persian Gulf (Iran, Iraq, Saudi Arabia, Kuwait, and the UAE) is forecast to rise to 45% in 2025 from 25% in 2003. Just seven countries-Russia, Iran, Iraq, Saudi Arabia, Kuwait, the UAE, and Venezuela-are expected to make up more than 60% of world oil production in 2025.

Global peak

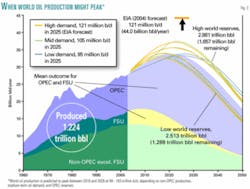

For the range of oil reserves demand scenarios considered here, world oil supply is predicted to peak at 90-105 million b/d between 2016 and 2028 (Fig. 3; Table 1).

The mean outcome is a peak of about 93 million b/d around 2021. Despite the considerable variation in oil reserves and demand scenarios considered, the peak in world oil production is predicted to occur within quite a narrow range. The principal reason for this is the rapid decline in non-OPEC production after about 2012. OPEC production may still be increasing, but it will not be able to compensate for the decline in non-OPEC supply.

Based on these results, the EIA forecast of world oil demand of more than 120 million b/d in 2025 seems unlikely to be met by production.

World oil production is not expected to decline to current levels until 2030 (low reserves case) or 2043 (high reserves case). Total world oil reserves are estimated at 2.5-2.9 trillion bbl. The world has consumed 1.224 trillion bbl to the end of 2004, so remaining reserves are estimated at 1.3-1.7 trillion bbl (Table 1).

Likely crises

As the different components of supply reach their maximum production rate, a series of crises in oil supply is likely over the coming decades.

The first, related to the peak and decline of non-OPEC production, is practically upon us and underpins the currently high oil prices. Other factors are burgeoning world oil demand, driven primarily by China and the USA, and restricted output from Iraq.

The imminent inability of non-OPEC production to meet incremental demand and its decline after 2010 precipitates the second crisis as OPEC’s diminishing spare capacity (even with Iraq’s production back to preinvasion levels) becomes less and less able to accommodate short-term fluctuations in demand. The timing and depth of the crisis depend on world oil demand and OPEC investment in new capacity. While OPEC countries will have every incentive to make the necessary investments, the pace of past decision-making is not encouraging, and enough spare capacity may not be available in time.

The third crisis, due to OPEC’s incremental supply being unable to meet incremental demand, follows in the first half of the next decade. This assumes that OPEC’s reserves are as published-882 billion bbl. If OPEC’s reserves are higher than published, this crisis may not occur until the latter half of the next decade and may be muted, particularly if demand moderates.

These crises will have global economic and geopolitical significance: The oil price will be high and volatile, and demand growth will have to be curtailed. ✦

References

1. Abdul Baqi, Mahmoud M., Saleri, Nansen G., “Fifty-Year Crude Oil Supply Scenarios: Saudi Aramco’s Perspective,” Saudi Aramco presentation to Center for Strategic and International Studies, Washington, DC, February 2004.

2. Laherrere, J., “Distribution and evolution of ‘recovery factor,’” paper presented at the International Energy Agency Oil Reserves Conference, Paris, Nov. 11, 1997.

3. BP PLC, “BP Statistical Review of World Energy,” 2004.

4. Kazempour Ardebili, Hossein, IIES conference in Tehran, October 2003.

5. Wells, P.R.A., “New production capacity: when can Iran deliver?” CWC conference, London, May 2002.

6. Campbell, C.J., “Middle East Oil-Reality and Illusions,” Association for the Study of Peak Oil and Gas, 2004. Web site www.peakoil.net.

7. Al-Husseini, Sadad, OGJ, May 17, 2004, p. 16.

8. Energy Information Administration, US Department of Energy, “International Energy Outlook 2004,” Report No. DOE/EIA-0484, 2004.