Study examines Chinese SPR growth alternatives

Development of China’s strategic oil reserve system depends largely on the mindset of its decision makers.

Conservative, security-driven thinking will lead to higher costs for the government and more stress on the global oil market. A more open-minded approach, by contrast, could allow an efficient and comparatively inexpensive build of reserves.

This article will examine the strategic petroleum reserve strategies used by the US, Japan, and South Korea, in an effort to determine the optimum course for development of China’s reserves.

Background

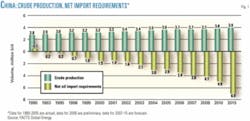

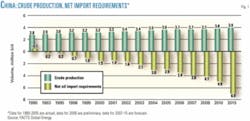

China’s demand for oil has become a global political and economic issue. China imported 2.9 million b/d of crude oil in 2006 and roughly 1 million b/d of refined products. It is the second largest oil consumer and third largest oil importer in the world. Net imports of oil (crude plus refined products) account for nearly half of its oil consumption (Fig. 1).

Against this backdrop, China has begun building a strategic stockpile of oil. By mid-2007 the Chinese government had filled the first strategic petroleum reserve storage site at Zhenhai, Zhejiang province; 12.4 million bbl nearly completely. Total capacity at Zhenhai’s SPRs is 5.2 million cu m (33 million bbl), split among 52 storage tanks.1

High-level discussion on the need for SPRs began after China became a net importer of oil in 1993. China’s Tenth Five-Year Plan, passed by the National People’s Congress in 2001, declared the goal of developing strategic stockpiles. Construction for the first four sites, however, did not begin until June 2004.

China’s SPR

China’s SPR plan has three phases.

- Phase I (2004-08) includes construction of one stockpiling facility each in Zhenhai and Aoshan in Zhejiang province, Qingdao in Shandong province, and Dalian in Liaoning province, with a combined storage capacity of 100 million bbl (25 days of China’s net oil imports).

- Phase II will increase storage capacity to 300 million bbl by 2010 (42 days of net oil imports).

- Phase III could increase storage to 500 million bbl.

China ultimately plans sufficient strategic petroleum reserves to cover 90 days of imports, which is also the mandatory goal of the International Energy Agency’s 90 days of forward cover initiative. FACTS’ forecast shows that to cover 90 days of net oil imports in 2015, China will need to have 625 million bbl of oil in storage.

Sinopec is overseeing construction of the Zhenhai site, which sits adjacent to its massive Zhenhai refinery. Sinopec is also responsible for construction of the Huangdao site, while PetroChina and Sinochem are building at the Dalian and Aoshan sites, respectively.

China’s state oil companies, however, will not manage the SPRs. The nascent State Oil SPR Office and State Oil Stockpiling Center will instead perform this role, having been established a few years ago for this purpose by the National Development and Reform Commission.

Sinopec completed construction of 52 100,000-cu m crude tanks at the Zhenhai base in August 2006. Construction of the three other storage bases in Aoshan, Huangdao, and Dalian is expected to be completed in 2007-08. Aoshan, like Zhenhai, will store roughly 5 million cu m (31 million bbl) of crude, while the Huangdao and Dalian sites will be smaller at 3 million cu m (19 million bbl) each.

Phase I of China’s stockpiling plan, which the government seeks to complete by the end of 2008, will therefore include roughly 16 million cu m (103 million bbl) of crude oil, equivalent to about 35 days of China’s current net oil imports, or 15 days of total oil consumption.

Sources within China have revealed glimpses of China’s future stockpiling plans. Phase II plans call for an additional 200 million bbl of tank storage, slated for completion by 2010. The country has begun looking for new sites to build this second batch of strategic petroleum reserves, including Caofeidian, Tangshan (Hebei province), Nansha, Guangzhou (Guangdong province), and Bao’an, Shenzhen (Guangdong province).

The planned Caofeidian storage has a capacity of 15 million cu m (94 million bbl). The city signed an agreement with Sinopec to build a 300,000-tonne crude terminal; construction has already begun. Handling capacity is 400,000 b/d. China will build a crude pipeline of the same capacity connecting Caofeidian with Tianjin. Total investment will be 3 billion yuan ($383 million).

Nansha is the location of a proposed 240,000-b/d Sinopec-KPC refinery and 1 million tonne/year ethylene plant. Titan Petrochemicals Ltd. of Singapore plans to build oil storage there. The city government of Shenzhen plans to build new oil and gas storage at Bao’an, Longgang, and Nansha.

China has also started preparations for a huge underground oil storage facility, the first of several planned underground storage sites being looked at in the city of Zhanjiang. According to local government, the storage caverns will hold 7 million cu m (44 million bbl) of oil, and construction will cost 2.3 billion yuan.

China’s Phase III plans call for an additional 200 million bbl of tank storage. Few details are available about these plans, but some SPR sites will be built in interior provinces such as Sichuan and Xinjiang.

Reserve strategy

According to Ma Kai, head of the NDRC, China’s top energy planning body, China’s SPRs will implement a dual oil reserve strategy that includes government and private strategic oil reserves. Besides having a government-managed SPR, the government will require that China’s four state-owned oil companies hold their own government-mandated oil stocks, imitating Japan’s stockpiling system.

The government also encourages large oil companies to build their own commercial oil reserves.

Operation mechanism

Sinopec, PetroChina, and Sinochem are only responsible for the construction of SPR facilities and will not manage and operate them. Established under the Bureau of Energy within NDRC, the State Oil Stockpiling Office is a governmental department, while the State Oil Stockpiling Center is much like a state-owned company and is directly responsible for the management and operation of China’s SPR. The full nature and structure of these organizations, however, remains unclear.

Oil companies

China’s State SPR Office lies inside the BOE within the NDRC. The director of the State SPR Office is also a deputy director of the BOE.

On Feb. 2, 2007, the National Energy Leading Group of the State Council said that SPR regulations will be part of the new energy law drafted by the National People’s Congress. Currently, oil storage held by Chinese state oil companies is considered commercial storage. State oil companies, however, will eventually participate in China’s SPR program.

On Feb. 5, 2007, the NDRC approved terminal expansion projects for Sinopec at Zhenhai and Sinochem at Aoshan, both in Zhejiang province. Sinopec will turn two small berths into a 250,000-tonne crude and product terminal with 150,000-b/d capacity. Sinochem plans to build a 300,000-tonne crude terminal at Aoshan with 300,000-b/d capacity.

Strategic, commercial

Ever since the Zhenhai SPR site started injecting crude in August 2006, controversy has surrounded the role of SPRs in China. Data show that of the 25 million bbl stored at Zhenhai SPR, nearly half have been leased to Sinopec. The NDRC insists that leasing SPRs is consistent with SPR principals, but others have raised questions regarding this practice. The rule itself is unclear, although the Chinese government promises to clarify how the SPR sites and crude should be used when the full legislature governing SPRs is completed.

Existing models

The US, Japan, and South Korea are the three consuming countries that have so far instituted SPRs.

- US. The US government operates the largest and most efficient public petroleum stockpile in the world. The US established its SPR in 1975 under the Energy Policy and Conservation Act in response to the 1970s oil embargo. As of Mar. 2, 2007, the US SPR held 688.6 million bbl of oil at four storage sites in Texas and Louisiana.

The presence of salt domes along the US gulf coast allows for large, cheap, and efficient oil storage, rapid drawdown, and minimal maintenance costs compared with other modes of storage.

The US Department of Energy operates the SPR and fills it via a royalty-in-kind program devised by the Clinton administration in 1999. Through this program, the DOE’s Minerals Management Service collects royalties as oil from companies operating government offshore leases in the Gulf of Mexico, and uses this oil to fill the SPRs. Prior to 1999, MMS collected these royalties in cash.

When President George W. Bush was inaugurated in 2001, the SPR held just under 600 million bbl of oil. Following the terrorist attacks of Sept. 11, 2001, President Bush instructed the DOE to fill the SPR to 700 million bbl, close to its capacity of roughly 730 million bbl.

The comprehensive energy bill passed by the US Congress in July 2005 calls for expansion of the SPR to 1 billion bbl, as long as purchases of oil for the reserves do not raise oil or oil product prices.

As the world’s leading importer of oil (13.5 million b/d in 2005)2 and dominant global economic and military power, the US governs its oil stockpiles conservatively. Government policy dictates that oil from the reserve can be released only by order of the president and in case of a disruption to oil supply.

Only two emergency drawdowns of the US SPR have occurred; one in 1991, the other in 2005. In January 1991, in response to oil market anxiety created by the Gulf War, the mere announcement of President Bush’s plans to release oil brought a measure of stability to the market.

The second emergency drawdown occurred after Hurricane Katrina caused massive damage to oil production facilities, terminals, pipelines, and refineries along coastal regions of Mississippi and Louisiana in late August 2005, causing gasoline prices to spike. In September 2005, through a coordinated action with the IEA, President Bush ordered the drawdown and sale of 30 million bbl of crude oil from the SPR to US markets. The IEA, which serves as the main supranational entity coordinating energy information and policy among developed countries, mandated a drawdown correlated with the US release.3

Any other US SPR releases have been limited to test sales and exchange arrangements with private companies.

- Japan. Japan’s model is the most expensive and comprehensive system of strategic oil stockpiling in the world. Japan imports more oil than any other country besides the US. Unlike the US and China, however, Japan produces no domestic oil.

Japan has divided its system of petroleum stockpiling into two sets of reserves: public and private. Roughly 320 million bbl of crude, managed by the Japan Oil, Gas, and Metals National Corp. under the Ministry of Economy, Trade, and Industry, comprise the government-managed strategic petroleum reserve.

Ideas and guidelines that govern these stockpiles are similar to those applied to the US SPR, but Japan has no salt caverns and has therefore needed to invest heavily in other methods of storing oil.

JOGMEC provides information on 10 national stockpiling bases accounting for roughly 215 million bbl of oil. This includes 112 million bbl in aboveground tanks, 51 million bbl in floating tanks, 30 million bbl in rock caverns, and 22 million bbl in underground tanks.

Aboveground tanks and rock cavern storage both represent financially appealing alternatives to salt caverns. Underground and floating tanks are much more expensive but demonstrate Japan’s efforts to protect its reserves from natural disasters such as earthquakes and typhoons.

The second part of Japan’s strategic stockpile consists of government-mandated private storage. Private Japanese oil companies and importers of refined products must maintain stocks equivalent to 70 days’ consumption. According to JOGMEC, private stocks amount to nearly 275 million bbl of oil, or 82 days’ forward cover. Crude oil comprises about half the private stocks, with oil products making up the balance.4

The stockpiling requirement is subsidized by the Japanese government but still constitutes a significant burden on Japanese oil companies and a large barrier to entry into the Japanese market.

The Japanese government’s drawdown policy is more rigid than that of the US. Japan’s nearly 600 million bbl of oil is the only reserve in the world that approaches the size of US SPR. Japan consumes less than a fourth and imports less than half as much oil as the US. Therefore, Japan’s system provides extensive protection against supply disruption, but at a very high cost.

In marked contrast to China and the US, Japan’s oil demand is shrinking, improving the strength of its reserves.

After a recent internal evaluation of its stockpiling practices, Japan plans to increase the strength, flexibility, and readiness of its reserves, including reducing private companies’ stock requirements to 60 or 65 days.

- South Korea. The South Korean strategic stockpiling model differs from the rigid approaches of Japan and the United States. Under government auspices, Korean National Oil Co. maintains about 63 million bbl of crude oil, 7.3 million bbl of petroleum products, and 3.6 million bbl of LPG. KNOC stores about 80% of these stocks in rock caverns, with aboveground tanks housing the remainder.

KNOC plans to increase the public stockpile to 140 million bbl by 2008. Current stockpiling locations have 114 million bbl in capacity. 4

Private Korean oil companies must maintain 40 days of forward coverage for domestic sales, equal to roughly 72 million bbl of oil.

KNOC manages Korea’s public oil stockpiles with flexibility in an effort to recoup some of the expense associated with building and maintaining stocks. The company occasionally conducts time swaps, which entail taking advantage of fluctuating oil prices by lending oil from national stockpiles. Korean refiners (and sometimes international oil purchasers) are invited to bid on a quantity of stockpiled oil. The winning bidder must return the oil within a stipulated period to pay the premium bid.

The practice is intended simultaneously to allow KNOC to offset costs, keep its reserves in circulation, and maintain a balance of stocks that reflect the present state of Korean consumption but fall short of acting as a revenue stream for the company.

KNOC also rents its spare storage capacity to foreign oil companies. Statoil stores more than 11 million bbl in KNOC’s facilities as part of its Joint Oil Stockpiling program. KNOC developed this program to allow continued growth of oil stocks following the Asian financial crisis of 1998. The program provides moderate revenue in the form of rental fees and dictates that in the event of a supply crisis, Korea would enjoy a preferred right to purchase Statoil’s stored stocks at market prices.

KNOC spends the money saved or earned from joint oil stockpiling and time swaps on expanding its reserve and occasionally comes under criticism for the cost-offsetting measures it employs in its stockpiling strategy. KNOC’s system, however, has broadened the concept of strategic oil stockpiling by showing that stockpiled oil does not need to be static oil.

Comparison

All oil-stockpiling systems share the goals of increasing oil supply security and minimizing the effects of supply disruptions by maintaining noncommercial oil reserves. The preceding descriptions, however, show that the world’s first, second, and fourth-ranked importers of oil have employed dissimilar stockpiling strategies. Characteristics relevant to this discussion include cost of development, forward cover protection, drawdown policy, and economic efficiency.

Tradeoffs exist between security and efficiency. The US stockpile is the largest, but high demand means its SPR provides the fewest days of forward cover. Japan’s high cost of development is partially attributable to Japan’s vulnerability to natural disasters as well as to lack of salt cavern storage.

Table 1 sheds additional light on the contrasting conditions and motivations that underlie each stockpiling system.

Strategic oil stockpiling, like many energy issues, represents a confluence of geopolitical and economic interests. None of the three systems represented is extreme. Despite KNOC’s cost-saving measures, oil stockpiles do not approach independent commercial feasibility. Even though massive Japanese reserves are hardly ever accessed, their existence inspires both national and global confidence in the oil market.

But large and readily identifiable cost differences exist among the different systems. The Korean approach places a smaller burden on both the Korean government and the global oil market. At the same time, however, no evidence exists that in a situation of global supply disruption, the Korean system would under perform its Japanese or American counterparts. KNOC’s relatively frequent drawdown and bidding procedures actually may facilitate smooth operation during a crisis.

This thread of analysis seems to show the superiority of Korea’s stockpiling system. Some experts and policymakers in China and elsewhere, however, disagree.

Analysis

Nominal oil prices at unprecedented highs and the global spotlight trained on China’s oil demand leave it little room for error in development of its oil stockpiles. Chinese sentiment currently favors Japan’s model, even as Japan plans to reform its system. Imitating Japan’s system, however, would be a mistake. China would be better off developing a flexible system, suited to its own unique economic, political, and strategic conditions.

This analysis finds no problem with Phase I of China’s stockpiling plan. The 100 million bbl stowed near import terminals and refineries will form the foundation of China’s strategic reserves.

As China’s import requirements continue to rise, however, stockpiling poses two challenges:

- Moderating any increase in dependence on imports.

- Avoiding price increases caused by importing barrels for stockpiling.

Filling its petroleum reserves will add 100,000-150,000 b/d to Chinese demand for years to come.

In order to keep up with increasing demand, China should expand its government reserves to maintain at least 50 days of forward cover, market conditions permitting. At current price levels, however, the per-barrel cost of these stocks will far exceed money spent in the past by Japan, South Korea, and the US in the development of their reserves. Building reserves as expansive and inflexible as in Japan or the US could be too costly. China should instead invest in a comfortable cushion of government stocks and augment them with more innovative measures.

The unique relationship between the Chinese government and its major oil companies could play to China’s advantage in developing reserves. The US and IEA oppose private strategic stockpiles because they fear that in an emergency, profit-maximizing companies may not share their government’s interest in protecting the domestic economy.

China, however, could take advantage of existing commercial storage capacity by requiring its state-run oil importers to hold 40 days of forward cover in a mix of crude oil and refined products, thereby achieving the goal of the IEA-mandated 90 days cover. These reserves, already in the hands of distributors, would serve as China’s first line of defense.

The Strategic Oil Stockpiles Office also could exercise flexibility in managing such “private” stocks, imitating KNOC by permitting companies to swap oil and to take advantage of seasonal price fluctuations.

Alternative stockpiling strategies could help complement China’s reserves. The Korean Joint Oil Stockpiling program is one example. The possibility of reaching agreements with producers to store their oil in China for release under certain predefined tight supply scenarios would be another.

References

- BP, BP Statistical Review of World Energy, June 2006.

- FACTS Global Energy, FGE Spring 2007 Databooks, April 2007.

- US Department of Energy, “Building Best Practices at the US Strategic Petroleum Reserve,” APEC Energy Working Group Workshop on Oil Stockpiling in the APEC Region, East-West Center, Honolulu, Ha., July 26-27, 2005.

- Kenji Kobayashi, International Energy Agency, “Growing Oil Imports, Growing Needs for Stockpiling and Global Oil Crisis Management,” APEC Energy Working Group Workshop on Oil Stockpiling in the APEC Region, East-West Center, Honolulu, Ha., July 26-27, 2005.

The authors

Daniel Nieh ([email protected]) is a language consultant at the International Centre for Security Analysis, London. He has also served as a research intern at Fesharaki and Associates Consulting and Technical Services (FACTS Inc). He holds a BA in East Asian languages and cultures (May 2006) from the University of Pennsylvania.

Kang Wu ([email protected]) is a senior fellow at the East-West Center and conducts research on energy policies, security, demand, supply, trade, and market developments, as well as energy-economic links, oil and gas issues, and the effect of fossil energy use on the environment. Wu is an energy expert on China and supervises the China Energy Project at the Center. He is also familiar with energy sector issues in other major Asia-Pacific countries and the region as a whole. As an energy economist, Wu’s work also includes energy modeling and Asia-Pacific energy demand forecasting. He holds a PhD in economics from the University of Hawaii, Manoa (1991).

Lijuan Wang is a senior consultant at FACTS Global Energy and chief representative of FGE’s Beijing office, focusing on Chinese energy issues. Previously, Wang served for 10 years as a journalist at China Chemical Industry News and for 5 years as editor-in-chief of China Chemical Week. She was a visiting scholar at both the East-West Center and Argonne National Laboratory. Wang graduated from Beijing University of Chemical Technology with BS degrees in both chemical engineering and management engineering.

Shi Fu ([email protected]) is a PhD candidate in economics at University of Hawaii and a research assistant at the energy economics group of the East-West Center. He has previously worked as a chemical engineer and an economic researcher. Fu holds a BA in chemical engineering from Nanchang University, China (1995) and an MA in economics from Sichuan Academy of Social Sciences, China (2003).