IEA: Upstream oil and gas investment continued to tumble in 2016

Upstream oil and gas investment continued to tumble in 2016, falling 26% in nominal terms to $434 billion, which was close to the rate of decline in 2015, according to the International Energy Agency’s 2017 World Energy Investment report. Investment in 2016 was little more than half the peak level of 2014, when oil prices started to fall sharply. The fall in investment in 2015 and 2016 totaled $345 billion in what could be called an unprecedented contraction.

The pace of the decline in upstream spending varies considerably by region, companies, and type of asset. Most of the decline can be explained by lower unit costs, but a significant share of the contraction is due to reduced drilling.

Led by a slump in shale drilling, North America experienced the largest decline in upstream spending over the 2 years to 2016, falling by nearly $180 billion, or 60%, the report said.

Investment remained resilient in the Middle East and in Russia because of lower finding and development costs, the prevailing fiscal regimes, and—particularly in Russia’s case—a well-developed local upstream service industry and exchange-rate effects.

All types of investments have seen reduced spending, with the largest declines occurring in shale oil and gas basins. By 2016, investment there had dropped to less than one third of levels reached in 2014. Oil sands saw a similar trend.

Capital investment in conventional projects, both onshore and offshore, showed greater resilience to the oil price collapse but drivers were fundamentally different.

“Onshore benefited from continued spending in regions like Russia and [the] Middle East as well as the strategies of several companies, which focused on maximizing output from already producing assets rather than developing new projects,” IEA said. “Investment in offshore projects, which have longer lead times, was supported by continuing spending in already sanctioned projects,” it said.

IEA noted that the magnitude of the drop-in dollar spending on conventional crude oil resources—which have historically provided the bulk of global oil supply—is nonetheless unprecedented. The number of projects that obtained final investment decision (FID) for development in 2016 was down more than 70% compared with 2013, to little more than 50. For offshore projects, the decline is even more pronounced since only 17 projects were sanctioned in 2016 compared with more than 70 just 3 years earlier.

Investments in 2017

Most of the companies that have released their investment plans for 2017 anticipate an increase in their budgets, indicating that spending may have bottomed out. Based on company reports, IEA estimates that global oil and gas upstream investment in 2017 is set to increase by almost 6%, to just less than $460 billion in nominal terms, or a 3% increase in real terms. The trend varies by region and by type of project and company.

However, with oil prices falling below $45/bbl in mid-June, there is a real possibility that companies may not be willing to fully implement these investment plans.

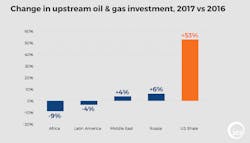

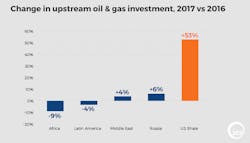

In 2017, the largest planned increase in upstream spending in percentage terms is in the US, in particular in shale assets that have benefited from a reduction in breakeven prices as a result of a combination of improvement in costs and efficiency gains.

Based on detailed analysis of investment announced by companies, spending in US shale activities is expected to increase 53% in 2017 compared with 2016, the report said.

In Mexico, upstream investment will get a boost from its first offshore licensing round, which successfully attracted bids from several international operators. Chinese national oil companies have all announced a rise in investments after 2 years of sharply reduced spending.

The anticipated rise in Russia’s upstream spending is subject to downside risks. While companies appear to be pushing ahead with new oil and gas projects to take advantage of tax breaks introduced by the government, the extension of oil production cuts agreed with the Organization of Petroleum Exporting Countries in May and the appreciation of the ruble might slow activities.

Capital spending offshore is expected to remain depressed this year, though some signs of a revival are emerging. Over the last 2 years, investment in offshore operations has been primarily focused on projects that had been sanctioned before the oil price downturn.

The only new projects that are expected to go forward in 2017 are those where costs have been cut sharply. They include projects in the North Sea and Gulf of Mexico, such as Statoil ASA’s Johan Castberg and BP PLC’s Mad Dog II, both of which have seen cost reductions and have benefited from simplification and standardization.

Brazil’s offshore is another area where offshore activities are expected to continue due to the combination of favorable factors including quality of reservoirs, recent cost reductions, and the entrance of experienced offshore operators such as Total SA and Statoil.

At midyear, Hess Corp. and ExxonMobil Corp. reported FID to proceed with the development of Phase I of the deepwater field offshore Guyana. On the other hand, projects in Angola and Nigeria are still suffering from high costs, exacerbated by local content requirements and unfavorable fiscal terms.

Similarly, activities in Southeast Asia are not expected to rebound quickly due to regulatory uncertainties and a resource base that is more gas-oriented and less economically attractive due to oversupply in regional markets and competition from large LNG supply facilities in Australia.

Source of financing

According to the report, despite the oil and gas sector’s poor financial performance and the observed loss in stock market value since mid-2014, it remains capable of attracting capital inflows. The downturn did not significantly affect the funding mechanisms for investments by oil and gas companies, though most of them increased leverage significantly.

For the majors, including BP, Chevron Corp., ConocoPhillips, Eni SPA, ExxonMobil, Shell, and Total, cash flow remained the main source of finance though net debt increased by over $100 billion between mid-2014 and early 2017. The majors’ commitment to maintain their dividend policies was a major factor behind the need to issue more debt.

US independents, with a more leveraged business model, initially saw debt costs soar, but their financial health has improved thanks to efficiency gains and the lower cost of debt. They continue to rely heavily on asset sales and external equity financing.