SPECIAL REPORT: World LPG production may outpace demand

Expansion of the global LPG industry has been faster than most other energy markets and will accelerate during the next few years as new LNG projects start up in many regions.

With increasing production of both conventional natural gas and LNG in many countries, LPG production will grow substantially. In addition to propane and butane, ethane production will increase rapidly, especially in the Middle East.

The residential and commercial markets for LPG have also expanded rapidly, primarily east of the Suez Canal, with especially strong growth in India and China leading the trend. High prices for all petroleum products, including LPG, have yet to dampen demand. Strong growth will be needed to absorb the impending rapid increase in production. If world economies begin to falter due to high energy prices, however, demand for LPG may be unable to consume the excess product.

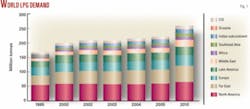

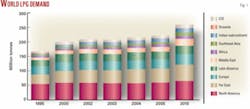

The global market for LPG increased to slightly less that 220 million tonnes in 2005 from only 168 million tonnes in 1995. This growth represents an overall increase of 31% or about 3.1%/year.

Virtually all end-use sectors contributed to this demand growth during this 10-year period. The engine fuel market grew fastest, but from a fairly small base. Both the residential-commercial and petrochemical feedstock sectors also enjoyed particularly strong growth during this period. Refinery demand for LPG declined slightly.

In North America, natural gas processing margins were unusually volatile during 2005, as natural gas prices remained relatively high during the first half of the year. Two devastating hurricanes in the Gulf of Mexico destroyed production platforms, pipelines, and gas processing plants in both Texas and Louisiana. Gas processing margins subsequently soared to record highs then declined at yearend.

During the 1990s and the early part of this decade, LPG markets were primarily demand-driven. Purvin & Gertz, however, expects that the second half of this decade will become supply-driven by the many new production projects that will be started up around the world.

Thus, through the end of the decade, supplies will likely grow faster than base demand. The resulting surplus of LPG will have to move into price-sensitive markets such as petrochemicals production during the next several years.

LPG demand growth

Global demand for LPG totaled slightly less than 220 million tonnes in 2005. Purvin & Gertz estimates that the market will grow to about 228 million tonnes in 2006 and reach more than 258 million tonnes by 2010. Thus, demand will likely grow by a total of about 55% compared to demand of 167 million tonnes in 1995 (Fig. 1).

Although total global growth for LPG since 1995 averaged 3.1%/year, growth rates in individual geographic regions have varied significantly. The highest growth has occurred in developing regions of the world. In the more mature economies of Western Europe and North America, LPG demand increased much more slowly than the global average.

Demand growth continued to be highest in the Middle East, Far East, Southeast Asia, and the Indian subcontinent. Much of this demand growth resulted from rising consumption by the residential-commercial sector. Demand growth in the Middle East primarily, however, resulted from the region’s expansion of its petrochemical sector.

Asia, Oceania

The total Asian market-the Far East, Southeast Asia, and Indian subcontinent-overtook North America as the largest LPG consuming region in the world in 2001. LPG demand in Asia totaled slightly more than 66.5 million tonnes in 2005. For comparison, the North American market increased to about 59.6 million tonnes in 2005. Thus, LPG demand in Asia has increased by an average of about 5.7%/year since 1995. Nearly 70% of total demand in the region is for use in the residential-commercial sector.

Within the region, Japan and China are the largest consumers of LPG. Demand in each country totaled about 18.6 million tonnes in 2005. In 2006, we expect demand in China will surpass Japan. Growth in Chinese demand for LPG was very strong at about 20%/year throughout the 1990s but has slowed to 7%/year during the first half of this decade. During the same time, Japanese demand growth was 0.4%/year during the 1990s and -0.5%/year since 2000.

Purvin & Gertz expects that Chinese demand will continue to grow but not at rates seen in the 1990s. Japanese demand will likely remain nearly flat, however.

The LPG market in Southeast Asia is much smaller than the Far East. Some of the markets nevertheless have also exhibited strong growth rates and are becoming more important regional players in the LPG trade.

The region has experienced total LPG demand growth of slightly less than 7%/year since 1995. Total LPG demand in the region grew to about 8.8 million tonnes/year (tpy) in 2005 from 4.7 million tpy in 1995.

Much of the demand in the region is concentrated in Malaysia and Thailand, both of which have mature LPG markets with high penetration in the residential-commercial markets. Together, these two countries represent 60% of the total demand in the region.

Most countries in Southeast Asia, with the notable exception of Singapore, have experienced reasonably high growth rates during the last 10 years. More than 70% of the regional consumption is in the residential-commercial sector. Purvin & Gertz expects that growth in this sector will continue through the rest of the decade at more than 5%/year. At about 13%/year, Vietnam will likely exhibit the highest growth rate of any country in the region during this period.

The LPG markets in the Indian subcontinent continue to exhibit strong growth rates. In 2005, total demand rose to about 11.1 million tonnes from only 3.8 million tpy in 1995. This increase represents growth of more than 10%/year. Almost all of this demand is concentrated in India, which accounts for more than 90% of the total LPG consumption on the subcontinent.

Almost all of the demand for LPG in Asia is in the residential-commercial sector. This region includes more than 3.5 billion people, or almost 56% of the world’s total population. We expect economic growth in this region to continue and result in additional consumption of LPG, although more slowly than during the last 10 years. Per-capita consumption of LPG in these countries will likely increase rapidly 2005-10.

Compared to Asia, LPG demand in nearby Oceania is very low at only 2.1 million tonnes in 2005. Australia dominates the regional market with total consumption of 1.9 million tonnes. One unique aspect of the Australian market is the very high use of LPG as auto fuel, an end-use sector that accounts for almost 65% of the total use in the country.

Purvin & Gertz expects that total regional demand will grow slowly to about 2.4 million tpy in 2010, with Australia continuing to dominate the regional consumption.

Latin America; Middle East

Latin America is also a large market for LPG. Since 1995, demand in the region has grown by nearly 6 million tonnes to about almost 27 million tonnes in 2005. Within the region, about 80% of the LPG is consumed in the residential-commercial sector.

Demand in the region contracted in 2002-03 but again resumed growing in 2004. Much of the contraction in demand occurred in Brazil and Mexico due to a combination of economic factors and penetration into the market by natural gas. Purvin & Gertz expects that demand will grow to nearly 30 million tonnes by 2010.

Mexico continues to have the highest per-capita use of LPG in the residential market of any country in the world. Four out of five households in the country use LPG as cooking fuel.

In the Middle East, LPG demand is a notable exception to most regions that consume large amounts of LPG in the residential-commercial sectors. Conversely, demand in the Middle East has been heavily influenced by the petrochemical sector’s use of LPG as a feedstock.

Additionally, the Middle East has historically provided much of the LPG that is consumed in the Far East. We expect that this trade pattern will continue for the foreseeable future. Increased crude oil production in the Middle East during the last few years has caused an increase in associated-gas production in the region. The corresponding increase in LPG production has freed up some supplies for export.

Saudi Arabia has been a major contributor to the use of the LPG for chemicals production and currently accounts for almost half of total LPG consumption in the Middle East. In 2005, regional demand for LPG totaled about 15.6 million tonnes, and Saudi Arabia accounted for about 7.4 million tonnes. Petrochemical feedstock demand accounts for more than 75% of the total demand in Saudi Arabia.

We expect that demand for LPG in Saudi Arabia will remain steady for several more years but will likely jump sharply beginning in 2008, as the next series of chemical manufacturing facilities come into production. Demand in the residential-commercial sector should remain relatively steady, with only slow growth during the next few years. By 2010, total demand should reach about 13 million tpy.

Iran is the next largest consumer of LPG in the Middle East, accounting for slightly less than 20% of regional demand. Demand growth in Iran has averaged slightly more than 5%/year since 1995. Petrochemical use of LPG in the country will increase dramatically after 2010, pushed by expanded production from the South Pars field. For the near term, rising demand by the residential-commercial sector will cause the market in Iran to grow by about 3%/year through the remainder of the decade.

Europe, Africa

LPG demand has increased rapidly in some countries of Eastern Europe. Due to the collapse of the former Soviet Union, many of the newly formed republics experienced severe economic downturns 1990-95. Since 1995, many of these countries have enjoyed strong economic growth, and LPG demand has increased accordingly.

From 1995 to 2005, demand in many of the countries of Eastern Europe increased at more than 7%/year. Although this demand growth is strong in percentage terms, the absolute increases in LPG volumes were less impressive, mainly because these countries were starting from fairly low consumption bases.

In Northern Europe, the UK and Ireland comprise the largest consumer of LPG and currently account for almost 3.7 million tonnes of the regional consumption, which totaled about 16.2 million tonnes in 2005. Germany is not far behind, accounting for 2.8 million tonnes. Scandinavia and Poland each consumed roughly 2 million tonnes of LPG.

Total base demand in Northern Europe has grown only slowly to 12.5 million in 2005 from 11.5 million tonnes in 1995. Price-sensitive consumption for ethylene production, however, has nearly doubled to 3.7 million in 2005 from 1.9 million tonnes in 1995. Purvin & Gertz expects price-sensitive demand to continue to grow rapidly for the next few years to nearly 5 million tonnes in 2010 as global production of LPG rises faster than base demand.

Within Northern Europe, auto-fuel use in Poland has exhibited extremely strong growth during the past 10 years and accounted for the bulk of the growth in the country’s LPG market. The auto-fuel market for LPG may be one of the highest growth sectors for the regional industry during the next few years, but growth will likely vary widely from country to country.

In southern or Mediterranean Europe, growth patterns for LPG have been quite different than in the north. The countries that make up this region are very diverse and include Spain, Italy, France, Turkey, Bulgaria, Romania, and the Balkan states. Thus, some markets are very mature, whereas others are continuing to develop rapidly.

Demand in Southern Europe has grown to 16.5 million tonnes in 2005 from 14.1 million tonnes in 1995, which represents an average annual growth of 1.2%/year. The price-sensitive sector in the region consumes only very small amounts of LPG. Strong economic growth by the developing markets in the region may result in slightly higher growth demand growth for LPG but will likely not deviate significantly from past trends. Total demand in the region should reach about 17.5 million tonnes by 2010.

The CIS region (Commonwealth of Independent States) includes Russia and all the republics of the former Soviet Union, except the Baltic states. LPG demand in the CIS has grown at 2.7%/year since 1995. Between 1990 and 1998, demand in the region steadily declined due to weak economic conditions. In recent years, however, positive growth has returned to these markets.

In 2005, demand in the CIS totaled about 7.5 million tonnes. Russia accounts for the largest portion of the regional demand, consuming almost 80% of the LPG. Within Russia, the residential-commercial sector uses slightly less than one half of the total, and petrochemical consumption of LPG accounts for almost 40%. We expect LPG demand in the CIS to rise to about 8.6 million tonnes in 2010.

In Africa, LPG markets have grown rapidly in some countries. Demand in the entire region has grown at 5.3%/year.

In 2005, total LPG demand rose to 8.7 million tpy. Almost all the consumption in Africa is in the residential-commercial sector. Egypt is the largest consuming country, accounting for about one third of regional consumption. Algeria and Morocco are also large regional consumers of LPG. We look for regional demand to increase to 10.8 million tonnes by 2010.

North America

In North America, overall demand for LPG has grown at less than the world average. The North American market is one of the largest in the world and is quite mature. The petrochemical industry relies heavily on LPG as a primary feedstock.

Demand in the region has grown at only 0.8%/year since 1995. This small growth rate, however, masks the absolute demand increase due to the large size of the market. LPG consumption in the North American market increased by 4.4 million tonnes during this 10-year period. For comparison, by itself, this increase is twice the size of total LPG consumption in Oceania.

The North American market is unique due to its high use of LPG in the price-sensitive petrochemical feedstock market. In 2005, the region accounted for slightly more than 50% of the total world’s consumption for petrochemicals production. Thus, North America provides the worldwide LPG industry with an outlet for excess product through its ability both to store and consume large amounts of LPG. The market share of LPG in the feedstock market fluctuates constantly based on relative economics.

Because North America is a very mature market, Purvin & Gertz does not expect overall base demand to grow appreciably in the region. Growth should average only about 1.1%/year through 2010. Demand by the price-sensitive market, however, should expand rapidly for several years as the petrochemical industry takes advantage of surplus global supplies. Thus, we look for price-sensitive demand to grow rapidly by roughly 9% during the next 5 years.

This rapid increase is contingent on a very delicate global balance between LPG and petrochemicals. High prices for natural gas in the North America have driven up LPG prices and adversely affected the region’s competitiveness in the global petrochemical market. Although North America regained some of this lost market in 2004 and 2005 due to rising crude oil and naphtha prices, renewed erosion of this competitiveness could slow potential demand for LPG.

Global supply

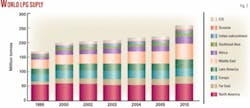

Global supplies of LPG rose to about 220 million tonnes in 2005 from 168 million tonnes in 1995. Thus, supplies increased by about 3.1%/year. Purvin & Gertz expects supplies will reach about 258 million tpy by 2010 (Fig. 2).

null

Changes in sources

Natural gas processing continues to be the largest supply source of LPG supply, accounting for nearly 60% of total worldwide production during the last 10 years. Refineries accounted for nearly all of the remaining production. Other sources account for less than 0.5% of worldwide LPG production.

A fundamental change in the market, however, will occur during the next few years as LPG is recovered from LNG, either as part of new natural gas liquefaction or at regasification terminals. The growth in LNG facilities around the world will unlock previously stranded gas supplies and increase LPG production accordingly.

Not all LNG projects will result in increased LPG supplies, however, because some markets can utilize LNG that includes the contained LPG. With many projects, however, extraction of the LPG components will be necessary before liquefaction of the gas stream. (See sidebar above.)

Regional supply

Regional LPG production has shown some notable shifts during the last decade.

In 1990, LPG produced in regions east of the Suez Canal (“East of Suez”) totaled slightly less than 30% of the world total. By 2000, the East of Suez’s share of total production had risen to about 35%, and Purvin & Gertz estimates that more than 40% of the world’s LPG supplies will come from East of Suez by 2010.

On a percentage basis, production increases have been particularly high on the Indian subcontinent, where production rose to 8.2 million tonnes in 2005 from only 3.4 million tonnes in 1995, growth of 9.8%/year. In Africa, production rose to 18.2 million tonnes from 8 million tonnes in 1995, growth of 8.7%/year. There were also significant increases in LPG production in both the Far East and Southeast Asia.

If absolute production increases are compared rather than percentage changes, however, the regional rankings are slightly different.

Since 1995, total global LPG production has increased by 52 million tonnes. The largest absolute production increase between 1995 and 2005 was in the Far East, where supplies increased by 10.9 million tonnes. Production in Africa increased by 10.3 million tonnes during the same period, and the Middle East’s LPG production rose by 9.4 million tonnes. Latin America and the Indian subcontinent increased their production by 6.5 and 4.8 million tpy, respectively.

• North America’s LPG production declined by 1.6 million tpy during this period. This decline is misleading, however, because a large amount of production in the prolific Gulf of Mexico region was knocked off line for several months during 2005 by two major hurricanes. Purvin & Gertz expects that LPG production in North America will grow during the next several years to nearly 58 million tonnes in 2010.

• The increase in Far East production of LPG was driven largely by increased production from refineries in both Korea and China. All of the production in the region comes from refineries, as there is no appreciable gas processing.

In the future, Purvin & Gertz expects that refinery production of LPG will increase, especially in China, where new refineries and refinery expansions are planned to accommodate the growing Chinese economy and growing demand for transportation fuels.

• In Africa, most of the LPG production increase is attributable to Algeria, where production rose to 10.8 million tonnes in 2005 from 5 million in 1995. Purvin & Gertz expects that LPG production will continue to grow but more slowly during the next several years. Due to the large growth in Algeria’s production, coupled with increased petrochemical consumption of LPG in Saudi Arabia, Algeria is challenging Saudi Arabia as the world’s largest exporter of LPG.

Libya is also a fairly large producer of LPG. Its production rose to 1.2 million tonnnes in 2005 and should reach about 1.5 million by 2010.

On Africa’s west coast, Nigeria’s LPG production has also increased significantly since 1995 due to an increase in crude oil production and a significant increase in gas processing capacity.

Previously, a large portion of Nigeria’s natural gas production, along with the entrained LPG, was flared. This practice has been decreasing, and the gas is now being processed to recover the LPG. Additions to LNG liquefaction capacity have also increased the overall recovery of LPG from the produced gas in Nigeria.

We expect that LPG production in Nigeria will increase to 5.7 million tonnes by 2010. Civil unrest in the country may become the largest impediment to increased production.

Other countries in West Africa that produce and export LPG include Angola, the Congo, and Equatorial Guinea. By 2010, we estimate that these countries will produce a total of about 1.6 million tonnes of LPG.

• The Middle East has also experienced high growth in LPG production since 1995. Saudi Arabia remains the largest LPG producer in the region, but other major contributors to this production increase include Iran, the UAE, and Qatar. The largest increase in production came from the gas processing industry in the region. Refineries produce only 11% of the region’s total LPG supplies.

During the next several years, we expect that LPG production will increase in Saudi Arabia, Iran, Qatar, and the UAE. All of these countries continue to develop existing and new gas reserves. The continued growth in worldwide demand for LNG will also drive expansion of gas processing in the Middle East. By 2010, LPG production in the region will reach about 53.5 million tonnes.

• LPG production in Latin America rose to 25.2 million tonnes in 2005. This production was less than in the Middle East and North America but higher than in the Far East.

Within the region, Mexico, Brazil, Venezuela, and Argentina are significant producers of LPG. Gas processing in the region accounts for more than 60% of LPG production; this will grow in the future. Several different countries will contribute to the expected growth in the future. In particular, Peru began production from the Camisea field in 2004.

Several countries in Latin America have plans for new and expanded gas liquefaction that will add to the regional LPG supply. Purvin & Gertz expects total LPG production in the region will rise to slightly more than 30 million tonnes by 2010.

• The Indian subcontinent has experienced strong growth in LPG supplies since 1995. Much of the growth has been due to additional crude oil refining capacity that was added in the late 1990s. More than two-thirds of the regional LPG production comes from refineries, which is a wide departure from the world average.

Total regional production rose to 8.2 million tonnes in 2005. India dominates the region, with more than 90% of production. By 2010, we expect that regional production will increase to 9.9 million tonnes.

• Gas processing capacity in Southeast Asia has increased since 1995, thereby adding LPG production to regional supplies. Refinery production in several countries in the region has also added to LPG production. The largest sources of supply in the region are Indonesia, Thailand, and Malaysia.

Indonesia has struggled to maintain LPG production at historic levels, due mainly to declining gas production at Bontang and Arun. The Arun LNG plant was shut down by civil unrest in the area, and LPG exports from Arun were discontinued several years ago. Gas volumes at Bontang continue to decline. Although additional LNG projects are under way, the natural gas feeding some of the newer projects is relatively dry and unlikely to yield much LPG.

Purvin & Gertz expects that regional LPG production in Southeast Asia will increase by about 1.6 million tonnes between 2005 and 2010. This estimate assumes some growth in gas processing in the region. Also, there are plans for a grassroots refinery in Vietnam, but this project is unlikely to add significant LPG volumes until at least 2009.

• In nearby Oceania, LPG production increased to 4.6 million in 2005 from 2.7 million tpy in 1995. This total increase of 73% during this period represents strong production growth, but the absolute volumes are small in comparison to overall worldwide supply. We look for production to grow modestly to about 5.0 million tonnes by 2010.

• Northern Europe is a large but mature producing region. LPG supplies have grown by less than 1%/year since 1995. Production from the North Sea represents a significant portion of regional production, but refineries in the region provide nearly half of the region’s total LPG supplies.

We expect that regional supplies will continue to increase, but growth rates will likely remain much lower than in other producing regions in the world. Increased refinery supplies of LPG should help offset declining North Sea supplies.

• In 2005, the CIS region produced 10.0 million tonnes of LPG, which represents a sizable increase from the production rate in 1995 of 5.9 million tonnes. This growth occurred as a result of additional gas processing in several countries. LPG production by refineries in the region, however, increased faster.

• North America continues to be a very large supplier of LPG, even though Asia has surpassed it in terms of overall consumption. We do not expect North America to lose its dominant position on the supply side in the foreseeable future.

Total LPG production in North America has been fairly stable during the last 10 years at roughly 55-59 million tpy. Gas processing provides slightly more than 60% of the LPG production in the region.

LNG projects

Future global production of LPG will be greatly affected by the additional natural gas that is produced in conjunction with liquefaction projects. New projects and expansions have been announced or planned for Qatar, Nigeria, Angola, Indonesia, Russia, Norway, and several other countries. These projects may add a large increment of LPG supply to the world markets during the next 5 years.

The most notable projects are in Qatar, with development of several new LNG trains associated with the North field, the world’s largest nonassociated gas field. Recoverable reserves in the field are estimated to be as much as 900 tcf of natural gas, representing about 20% of the world’s proven gas reserves.

If these gas production projects are developed on their current timeframes, we estimate that Qatar’s production will soar to slightly more than 6 million tonnes of LPG by 2010 from only 1.1 million in 1995. By 2015, production could increase by an additional 3-5 million tpy.

Iran also has plans to develop natural gas projects associated with the portions of the same gas field that fall within its national waters. LPG supplies from Iran will likely increase by more than 50% as the South Pars field is developed. Some of the additional LPG will be used in petrochemical projects that are being developed in conjunction with the gas production and processing facilities.

Expansion of the LNG industry in Nigeria will more than double LPG production from this coastal African country.

Along with the additional LPG derived from natural gas liquefaction around the world, more LPG production will also come from existing and new gas processing and refinery projects. Purvin & Gertz expects that LPG supplies during the period 2005-10 will expand more rapidly than in the first half of the decade. We look for total global LPG supply to reach 258 million tonnes by 2010, up from 220 million tonnes in 2005.

Trade patterns

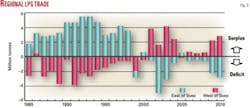

An interesting shift in global LPG trade patterns occurred in the late 1990s. Between 1995 and 2000, LPG demand in the East of Suez region increased by about 17.3 million tpy. During this same period, supplies in the region increased by only 15 million tpy. Although these changes seem subtle, the overall LPG supply-demand balance East of Suez shifted from a surplus of supplies to a deficit. Conversely, West of Suez experienced an equal but opposite shift in its LPG supply-demand balance (Fig. 3).

These relative changes in the regional supply-demand balances affected world LPG trade patterns. The Far East continues to be the largest LPG importing region in the world. Additional consumption of LPG to produce petrochemicals in some of the exporting countries in the Middle East, however, has reduced the amount of LPG available for export. Therefore, in recent years the Far East has had to import LPG from increasingly diverse sources to meet the demand of the region. As a result, imports into the Far East have come from West and North Africa and even from the North Sea.

The US continues to be the primary swing destination or supplier of LPG to the global market. The US has a large capacity to store LPG during times of excess global supplies and can also supply LPG from storage to other regions when their supplies are tight. Furthermore, the US petrochemical industry can consume large amounts of LPG when prices are attractive relative to other possible feedstocks.

Our analysis indicates that the increase in global LPG supplies will outpace the increase in base demand during the next several years. Therefore, discretionary consumption of LPG as a feedstock for petrochemical production (price-sensitive demand) will need to increase.

We estimate that total global price-sensitive demand will increase from 9.6 million tonnes in 2005 to about 13 million tonnes by the end of the decade. About 1.3 million tonnes of this expected increase will likely occur in Northern Europe, and the remaining increase of about 2.1 million tonnes will occur in North America.

Regional ethane markets

Ethane is seldom transported in ships from one region to another due to the high costs of shipping cryogenic products. Despite that difficulty, ethane is an extremely important component of the global petrochemical industry.

Nearly all ethane is extracted from natural gas. Its physical properties are relatively similar to methane, which is the main component of natural gas. Therefore, ethane can either be left in the gas or extracted from it.

The decision whether to recover ethane generally depends on the economics of extracting it from the produced natural gas. If ethane is to be recovered, its price must be higher than its extraction and purification costs, including its gas-based heating value.

Analyses by Purvin & Gertz’ strategic partner, Chemical Market Associates Inc. (CMAI), show that ethane was used to produce almost 29.5 million tonnes of ethylene in 2005, or about 27% of the 106.5 million tonnes of ethylene that were produced during the year. Despite this very large market, ethane’s use is extensive in only a few regions of the world, primarily the Middle East and North America.

The largest regional use of ethane occurs in the US and Canada, which account for about 53% of all the ethane consumed in the world. In the US, ethane supplies are adequate to cover industry needs, as significant amounts of ethane are still not recovered from natural gas that has been processed.

The Canadian petrochemical industry uses ethane extensively in western Canada, while the eastern Canadian industry uses a wider variety of feedstocks. In Western Canada, ethane production has declined, and propane has been used to supplement that declining production. Longer term, additional gas supplies from the Mackenzie Delta, Alaska, or both should help supplement current ethane supplies.

During the last few years, Latin America (primarily Mexico) consumed slightly more than 1.2 million tpy of ethane to produce about 23% of its total ethylene. Ethane consumption in Western Europe averaged roughly 2.4 million tpy during the last few years, which accounted for about 8% of the region’s total ethylene production.

Lastly, the Middle East has become a significant component of the global ethane market. About two-thirds of the ethylene that is produced in the region is derived from ethane. Thus, in 2005 the Middle East used 25% of the total world’s consumption of ethane. As new ethylene plants are added in several countries in the region, the Middle East’s share of the ethane market should grow to about 45% by 2010.

Additional ethane will need to be extracted from natural gas to satisfy global consumption for petrochemical production. In 2005, Purvin & Gertz estimates that the world’s consumption of ethane totaled about 37 million tonnes. This total could rise to more than 52 million tonnes by 2010. Most of this expected increase will occur in the Middle East.

The authors

Ronald L. Gist (rlgist@ purvingertz.com) is a senior principal in the Houston office of Purvin & Gertz Inc., having joined the company in 1996. He began his career with E.I. DuPont de Nemours & Co. in 1971 after receiving both BS and MS degrees in chemical engineering from Colorado School of Mines. Gist chaired GPA’s market information committee and is currently a director of the Houston chapter of GPA.

Ken W. Otto (kwotto@ purvingertz.com) is a senior vice-president and director in the Houston office of Purvin & Gertz Inc. He joined E.I. DuPont de Nemours & Co. in 1977, then moved to Champlin Petroleum Co. in 1979 and served 4 years at Corpus Christi Petroleum Co. Otto joined Purvin & Gertz in 1986, was elected principal of the company in 1987, senior principal in 1990, and vice-president in 1997. He holds a BS (1977) in chemical engineering from the University of Texas at Austin.

S. Craig Whitley (scwhitley@ purvingertz.com) is a senior principal in Purvin & Gertz Inc.’s Houston office. He joined the company in 1993, working in market analysis of natural gas, LPG, and NGL markets. Whitley has a BS in chemistry and zoology from Northwestern Louisiana State University, Nachitoches. He is a member of GPA, the International Association of Energy Economists, and the National Propane Gas Association.

Extracting NGL from LNG: no easy decision

The surge in projects to both produce and consume LNG will generate a corresponding increase in production of NGL. The amount of NGL in LNG, however, varies widely and is among the many considerations that complicate a decision to extract.

Many projects that primarily supply LNG to consumers in the Far East, specifically Japan and Korea, do not extract NGL from the gas. Conversely, LNG that contains relatively large amounts of NGL is often incompatible with markets in both Europe and North America.

At liquefaction

At the supply source before liquefaction, the presence or lack of local markets for both fuels and petrochemical feedstocks can be a major determinant in whether to extract NGL. Additionally, primary destinations for the LNG and accessibility to profitable markets for the NGL are important factors in the decision.

Most liquefaction processes require that virtually all of the natural gasoline be removed from the gas before liquefaction. Likewise, LNG typically contains less than 1% normal butane and isobutane. The propane content, however, can vary from roughly 0.1 vol % to as much as 3 vol %. The ethane content in LNG can vary significantly from 3% to 10%.

At destination

Therefore, at the destination for the LNG, processing decisions primarily involve the extraction of ethane and, to a lesser extent, propane. Several factors can influence this decision.

First, regulations or market specifications that set relatively low limits on the heat content of the re-gasified LNG can potentially override all economic factors.

If the heating value of the re-gasified LNG is too high, the gas can be blended with an inert gas such as nitrogen. This technique is currently used at some US regasification terminals. Similarly, the re-gasified LNG can be blended with natural gas from conventional domestic sources. Lastly, the NGL can be removed from the LNG during the regasification process.

Options

Two options are available for removing the NGL.

In one scheme, some or all of the NGL can be removed from the entire LNG stream. Alternatively, virtually all of the NGL can be removed from only part of the LNG to produce a very lean gas, which can then be blended with the remaining unprocessed LNG.

If the decision to extract ethane and propane from the LNG is based primarily on economics, yet another set of factors must be considered. Because LNG is already at cryogenic temperatures, significantly less energy is required to extract NGL from the gas. Thus, operating costs at LNG terminals are lower than for traditional gas processing plants. The NGL that is extracted from the LNG, however, may have to displace NGL from other conventional production sources. The resulting competition between the two sources may drive NGL prices downward.

Also, additional capital investments at the regasification terminals are required to extract NGL. The size and configuration of each terminal dictate the cost of the investment, which can exceed $50 million.

An investment of this magnitude may be difficult to justify for facilities such as LNG regasification terminals that do not necessarily have a continuous source of incoming product. Furthermore, the ethane and propane content in the LNG can vary widely, depending on the source of the LNG. Lastly, the NGL content of the LNG could drop significantly if any of the source countries decide to extract the ethane and propane for domestic use.

It may be difficult, therefore, to justify such a large investment in NGL-extraction capacity for a facility with an unpredictable supply.

Learn more about what’s happening in LNG

With the July 3, 2006, issue of Oil & Gas Journal, more than 60,000 subscribers will also receive the third 2006 installment of OGJ’s LNG Observer, a quarterly magazine produced with the widely respected GTI, Des Plaines, Ill. This publication aims at anyone interested or involved in the natural gas and LNG business.

If you don’t receive a copy of LNG Observer with your OGJ subscription:

- Access www.lngobservercom after July 10, 2006, to read it online; or,

- Write [email protected] to submit your e-mail address so that your name can be added to the circulation list.