ATJ offers viable pathway to increased SAF production

Probir Shah

Baker & O’Brien Inc.

Dallas

Operators, policy makers, and industry groups agree that development of production technologies for sustainable aviation fuel (SAF) is a vital pathway to cutting carbon emissions within the hard-to-abate air transportation sector to meet global net-zero goals by 2050.

While manufacturers currently use various processes for production of sustainable fuels (SAF, renewable diesel) from plant oils and recycled fats, an American Society for Testing and Materials (ASTM)-approved and commercially proven route to SAF production known as alcohol-to-jet (ATJ) technology based specifically on a feedstock of ethanol has garnered less traction with operators.

In this article, Baker & O’Brien Inc. evaluates SAF production using the ATJ process and ethanol feedstock to help operators establish a framework for conducting the detailed economic analysis and due diligence that highlights drivers and risks of potential ATJ SAF projects ahead of undertaking any major capital commitments.

Alongside examining feedstock supply issues, ATJ technology, and process economics against the background of regulatory incentives designed to spur increased output of SAF, the article also explores the future of US-based ATJ SAF production and suggests ways to enhance potential project profitability.

SAF demand, incentives

The International Air Transport Association (IATA) estimated global SAF production in 2022 at 80-120 million gal, covering less than 0.2% of total jet fuel demand.1 Although air transportation currently accounts for 2-3% of global anthropogenic carbon dioxide (CO2) emissions, continued growth in jet fuel demand—which IATA anticipates will come mainly from the expanding middle classes of developing countries—is projected to increase the sector’s percentage of emissions.

In line with the global energy transition, IATA member airlines are working to ensure sustainable growth by supporting net-zero emissions from their operations by 2050. The industry pledge comes alongside commitments from the current US administration targeting 3 billion gal/year of SAF production by 2030 and 35 billion gal/year by 2050, as well as those of the European Union (EU) under the ReFuelEU deal for aviation fuel suppliers to ensure that all fuel made available to aircraft operators at EU airports contains a minimum 2% share of SAF from 2025, 6% by 2030, 20% by 2035, up to a maximum of 70% by 2050.2-3

With development of commercially practical technologies for mass production of SAF critical to meeting US and EU net-zero emissions, Baker & O’Brien previously examined the predominant hydroprocessed esters and fatty acids (HEFA) route operators currently use to produce SAF and renewable diesel, which requires increased competition for the process’s feedstock of plant oils and recycled fats.4-5 The analysis also discussed how existing US federal and state tax incentives—including the federal Renewable Fuel Standard (RFS) and Inflation Reduction Act of 2022’s (IRA) Clean Fuel Production Credit (CFPC; extending the blenders tax credit through Dec. 31, 2024, and providing other tax incentives for SAF after Jan. 1, 2025), as well as various state-level Low Carbon Fuel Standard (LCFS) programs—favored investments in renewable diesel over SAF production.

ATJ SAF considerations

While there are at least seven ASTM-accepted processes for SAF production and many more still under testing for certification, ASTM currently approves ATJ-produced jet fuel from an ethanol or isobutanol intermediate under ASTM D7566 Annex A5, which permits blending up to 50% with conventional jet aviation fuel.

Many companies already have pursued SAF production via ATJ, with various airlines announcing numerous testing agreements. Ahead of its completed merger with United Airlines Inc. in 2012, the former Continental Airlines Inc. in 2011 tested ATJ-based jet fuel derived from algae oil. The US Air Force tested an A-10 Thunderbolt II jet in late-June 2012, and the US Army tested the Sikorsky UH-60 Black Hawk helicopter in late-December 2013, both using an ATJ-conventional fuel blend based on cellulose-derived alcohol.

After more than a decade of successful ATJ SAF flight tests, however, economically viable mass production of commercial SAF using ATJ technology continues to be difficult compared with fossil-based commercial jet fuel.

In the current discussion, factors considered in assessing SAF profitability via ATJ include the following:

- Feedstock type, supply.

- Process technology.

- Product yield, conversion efficiency.

- Co-product yield, value.

- Tax incentives.

Ethanol supply

The first consideration in the ATJ SAF production process involves availability of alcohol feedstocks such as methanol, ethanol, butanol, and other long-chain fatty alcohols.

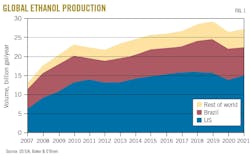

Fig. 1 shows global ethanol production by region between 2007 and 2021.

Globally, the US is the largest ethanol producer, with corn grain as the basis for most of the country’s production. While ethanol can also be produced from lignocellulosic crops (e.g., switchgrass), large-scale commercial production of ethanol from this feedstock remains unlikely.

Based on historical analysis of US Department of Agriculture (USDA) data, the yield per acre of corn production has increased by at least 20% during the last 15 years, with the yield of corn-based ethanol production (gallon of ethanol per bushel of corn) increasing by at least 10% across the same period. This compounding effect ensures an ample supply of ethanol from corn if sufficient ethanol production capacity is added.

Ethanol also benefits from an established supply chain infrastructure due to the RFS program administered by the Environmental Protection Agency (EPA). In the US, ethanol is blended into gasoline at a rate of about 10.3 vol. %, according to the Energy Information Administration (EIA). In 2022-23, EIA data show ethanol production averaged about 15.5 billion gal/year, enough to cover domestic supply requirements and exports of about 2 billion gal/year.

US ethanol plants, however, are equipped with 2 billion gal/year of underutilized capacity, making it possible for US producers to provide about 4 billion gal/year of ethanol for ATJ-based SAF production (e.g., 2 billion gal/year from exports plus 2 billion gal/year from spare capacity). The potential future supply of corn-based ethanol for ATJ production appears to be abundant through established supply chains and spare production capacity compared with other ethanol sources, such as cellulosic ethanol.

Brazil, the second-largest ethanol producer after the US, produces most of its ethanol from sugarcane, a competitive source of ethanol compared with corn-based ethanol. Only about 4% of Brazil’s ethanol production is corn-based.

Combined, US and Brazilian production account for more than 85% of global ethanol supplies, positioning the two countries to become the dominant suppliers of ethanol feedstock for future SAF production. Alongside its role as producer, Brazil is also the second-largest global ethanol consumer, mainly due to the country’s 27% fuel ethanol-blending requirement.

Recent data from the EIA and Brazil’s National Petroleum, Natural Gas, and Biofuels Agency showed that, in 2019, Brazil set a record for the highest ethanol production in any given year with an output of about 9.3 billion gal/year, which included a small net of 200 million gal/year in exports destined mostly to the US (about 5% of its domestic availability). The annual production record in 2019 came amid Brazil’s larger-than-expected sugarcane crop and low sugar prices.

In 2022 through end-September 2023, Brazil’s ethanol production averaged 8.4 billion gal/year, or about 90% of its 2019 production. Based on these levels, the amount of Brazilian ethanol available for export could be limited, but additional ethanol production may still be available given that the country’s ethanol plants operate at about 75% capacity. Any additional production might not be available for the US, however, as Brazil sets limits on ethanol exports.

A key takeaway is that the combined, total potential of ethanol availability for ATJ-based SAF production from US and Brazilian imports is about 4.2 billion gal/year, dominated by US supply potential. This assumes zero growth in production capacity and no change in US and Brazilian gasoline-blending demand for ethanol.

Emission considerations

Carbon intensity (CI) measures greenhouse gas (GHG) emissions associated with producing, distributing, and consuming a fuel and is based on the complete lifecycle of that fuel. It is commonly expressed in grams of CO2 equivalent per megajoule (MJ) of energy that fuel provides (gCO2e/MJ).

As outlined by the US RFS program, fossil-based jet fuel has a CI of 89.4 gCO2e/MJ. Ethanol derived from sugarcane (CI = 23.8 gCO2e/MJ) produces notably lower GHG emissions than corn ethanol (CI = 65.7 gCO2e/MJ) due to differences in agriculture and refining processes. While sugarcane-based ethanol currently provides a much higher incentive for use under the California LCFS and IRA CFPC tax credit programs, its availability can vary year-to-year based on performance of sugarcane crops and sugar prices. The economics of corn-based and sugarcane-based ethanol are discussed in detail in a later section.

ATJ process technology

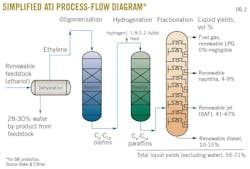

Fig. 2 presents a simplified ATJ process-flow diagram for production of SAF using product yields Baker & O’Brien estimated from non-proprietary, open-literature reviews.

In the ethanol-based ATJ process for SAF production, ethanol feedstock (alcohol) is dehydrated to ethylene, oligomerized into longer carbon chains, and hydrogenated to produce a jet fuel blendstock. By-products from the ethanol-to-jet pathway include water, LPG, naphtha, and diesel.

- Dehydration. Ethanol is first converted to ethylene (an olefin) via catalytic dehydration with water as a by-product of the reaction. Up to 10% of the ethanol can be found in the by-product water for further separation and recycling as feedstock to increase the overall conversion efficiency of the process.

The maximum amount of entrained water allowed in ethylene depends on the downstream catalyst technology. It may be possible to improve the catalyst design to accommodate higher amounts of moisture in ethylene, which helps minimize the ethanol content in by-product water. Maximizing once-through ethanol conversion to ethylene can remove the need to recycle the by-product, and such improvements increase the overall SAF conversion from the ATJ process.

- Oligomerization. Oligomerization reactions convert ethylene to long-chain olefins in the C4-C16 carbon chain length. Jet fuel is a C9-C16 carbon chain-length hydrocarbon with a boiling point range of 350-525° F. A small purge stream of lower-carbon products (not shown in Fig. 2) is maintained to minimize C4-C8 hydrocarbons in the oligomerization product. These C4-C8 molecules yield LPG and renewable naphtha, which typically have the lowest economic value of the process. Renewable naphtha can be blended into gasoline as renewable gasoline, while the fuel gas and renewable LPG can be used as fuel sources for the process heaters. Precise process design considerations are essential in this step for improving the desired yields.

Carbon chain-length molecules longer than C16 end up as renewable diesel, but there may be times when production of the renewable diesel by-product might be favorable depending on relative market values.

- Hydrogenation. Long-chain olefins are hydrogenated in a second reactor to convert them into saturated hydrocarbons (paraffins), preferably in the C9-C16 range. This reaction requires a large amount of hydrogen at high pressure in the presence of a catalyst.

- Fractionation. In the final phase of the process, the hydrogenated effluent is treated in a fractionator to separate the products based on their boiling point ranges.

Notably, the abovementioned processes involving dehydration, oligomerization, hydrogenation, and fractionation are common in the petrochemical industry, allowing for a shallow learning curve and rapid project development.

SAF yields are typically in the 41-47 vol. % range of ethanol processed, with total product liquid yields in the 55-71 vol. % range. Based on the 4.2 billion gal/year of ethanol availability cited earlier, the estimated US ATJ SAF production potential is about 1.7-2.0 billion gal/year.

Innovative technologies currently under development are anticipated to further increase efficiency and yields, which should decrease production costs and improve economics. Due to the commercial infancy of the ATJ SAF production scheme, process technology is a crucial element to address as part of any project’s due diligence and investment evaluation.

Although SAF production costs are considerably higher than conventional jet fuel, synergies with preexisting installations and equipment can be exploited. An advantage of using the ethanol-based ATJ process is that ethanol plants can be expanded or revamped to accommodate the technology. Additionally, ATJ SAF production plants can be co-located with petrochemical plants to integrate with existing infrastructure and utilities. Integration of the production process with existing petrochemicals and refining sites could result in major capital and operating cost savings.

ATJ process economics

The following ATJ economic analysis considers ethanol-feedstock costs, product and by-product prices, and the value of federal and state incentives.

A key parameter for assessing ATJ economics is the market value, or realized price, of SAF. With production still in its relative infancy, SAF volumes currently trade at a large premium to conventional jet fuel. IATA reports that, in 2022, the price of HEFA-produced SAF was about two and a half times higher than that of conventional jet fuel.6 IATA, however, also anticipates that SAF prices will converge with fossil-based jet fuel prices over time. To assess the economics of ATJ, then, SAF is valued the same as current fossil-based commercial jet fuel without any premium for its lower CI. Instead, a breakeven price for SAF has been calculated to earn a 15% return on investment in SAF production.

For illustration purposes, this article assumes the ATJ SAF plant is on the US Gulf Coast (USGC), which features a large concentration of refineries and petrochemical plants. Since California is the most active and mature low-carbon fuel market with LCFS incentives, product placement is assumed in Los Angeles. Additional parameters of the analysis include the following:

- Ethanol-feedstock cost is estimated as the delivered price to the plant gate.

- Product prices at the plant are calculated by deducting transportation costs from product prices delivered to Los Angeles.

- Plant operating costs are estimated at 50¢/gal of ethanol processed, including fixed and variable costs. Variable costs include the cost of hydrogen, purchased energy, catalysts, and chemicals. Fixed costs include labor, overhead, maintenance, property taxes, insurance, and other non-variable costs.

It is typical for this type of project to require double-digit returns (about 15%) on capital employed to cover the cost of capital and a risk premium. Based on Baker & O’Brien’s review of a recent US ATJ SAF project, this capital-return requirement in the current analysis is estimated at 75¢/gal of ethanol processed.

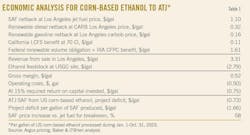

The economic analysis presents two hypothetical ATJ SAF plants in the US, one of which uses a feedstock of corn-based ethanol and a second that uses a feedstock of Brazilian sugarcane-based ethanol (Tables 1-2).

The pricing and incentive data are for the period running Jan. 1 to Oct. 30, 2023, on average. The analysis is based on the per gallon cost of US corn-based ethanol processed by the plant.

After allowing for operating costs and a required 15% return on capital employed against the gross margin, the corn-based ethanol ATJ SAF plant would realize a projected loss of 73¢/gal of ethanol processed. Based on an SAF volumetric yield of 44%, this equates to a net loss of $1.66/gal of SAF produced. The project would be breakeven, meeting the capital-return requirement, if the SAF product price is 58% above the price of jet fuel.

In the second scenario, the plant using Brazilian sugarcane-based ethanol as a feedstock for the ATJ SAF process would benefit from the IRA’s CFPC incentives due to its projected 51% lower overall GHG emissions than fossil-based jet fuel. The plant would also receive a higher California LCFS incentive due to its estimated lower CI of 44 gCO2e/MJ overall for the ATJ process. This is based on the sugarcane-derived ethanol’s CI of 23.8 gCO2e/MJ, adding contributions from estimations for transportation to the US and ATJ plant emissions, and subtracting estimated improvements to lower the CI.

After allowing for operating costs and the required 15% return on capital employed in the gross margin, the sugarcane-based ethanol ATJ SAF plant would realize a projected loss of 3¢/gal of ethanol processed. Based on an SAF volumetric yield of 44 vol. %, this equates to a net loss of 6¢/gal of SAF produced. The project would be breakeven, providing the required capital return, if the SAF product price is 2% above the price of jet fuel.

The sugarcane-based ethanol ATJ SAF plant is breakeven at a 35% lower SAF price than the plant using the corn-based ethanol ATJ SAF process. As of end-October 2023, the plant using the sugarcane-based ethanol ATJ SAF process maintained breakeven economics through the period (Table 2).

Assuming sugarcane-based ethanol is priced at parity to corn-based ethanol, the lower CI of the former is clearly more economical than corn-based ethanol for the ATJ SAF process. As previously noted in the discussion on feedstock supply, however, Brazil’s current ethanol supply availability is minimal compared to forecast SAF production demand, which needs to be considered when assessing potential US ATJ SAF projects. Regardless, any sugarcane-based ethanol ATJ SAF plant should have the flexibility to switch to corn-based ethanol to mitigate against scenarios when the sugarcane harvest decreases or sugar prices increase.

ATJ investment profitability

A complete understanding of federal, state, and local renewable fuel production incentives will be necessary for ATJ SAF plant investors. Consideration of various locations and production periods is essential to understanding product placement optionality. For US operators, this would involve review of final regulation for the SAF credit under the IRA of 2022’s CFPC released on Dec. 15, 2023, as well as consideration of California, Oregon, and Washington LCFS programs, where specific periods might provide arbitrage opportunities for one product destination over another. Certain other US states and cities also have announced different incentives for SAF use in their jurisdictions.

While CI for the renewable fuels mix (in gCO2e/MJ) as calculated by the various US West Coast states’ LCFS programs plays a major role in the overall state incentive, the IRA places a substantial threshold on SAF production to reduce the CI by more than 50% for the applicable tax-credit benefits to apply. Federal and state programs do not necessarily use the same lifecycle analysis model to calculate renewable fuel CIs.

Currently, economics for ATJ SAF investments in the US do not appear sufficiently robust to encourage the SAF volumes required to meet global net-zero goals. Additional incentives, mandates, or efficiency improvements are likely necessary for substantial investments in the ATJ SAF process. Changes to increase profitability are possible in three areas: carbon regulation, agriculture-related improvements to reduce ethanol’s CI, and ATJ processing improvements.

Increased carbon regulation can happen through a combination of higher LCFS credit values, higher prices for Renewable Identification Number (RIN) credits under the RFS, and lower lifecycle GHG emissions. The California Air Resources Board (CARB) is working to incentivize the LCFS program to continue promoting investments toward lower-CI fuel consumption in the state. Regulations and aggressive CI reduction targets are potentially under consideration to increase the LCFS credit values; however, RINS prices have moderated recently. Other states considering the adoption of low-carbon incentive programs will help create more demand for renewable fuels closer to the ATJ SAF plants, reducing transport costs and increasing profitability. The IRA’s CFPC regulations for fuel production starting Jan. 1, 2025, also can potentially increase the impetus for continued investments in renewable fuels projects. Projects using renewable energy, for example, from solar or wind sources, green or blue hydrogen, and CO2 sequestration, can decrease the LCFS CI and GHG emissions, thus increasing the incentive from LFCS and CFPC programs.

As to agricultural improvements, according to a USDA study, farmers are producing corn more efficiently with lower GHG emissions by reducing tillage, using cover crops to capture atmospheric CO2, and improving nitrogen management. These improvements can potentially decrease the CI of corn-based ethanol.

Another potential area for higher profitability can come from improvements to the ATJ SAF process. Increased yield selectivity and higher conversion rates of SAF from the oligomerization and hydrotreating reactions would drive higher SAF production and lower SAF breakeven prices.

The HEFA process currently produces SAF and renewable diesel, with US subsidies and incentives favoring production of the latter. The ATJ process, however, opens a new pathway for producing SAF. As demonstrated by the economic analysis of two US ATJ SAF plants, production of SAF from low-CI Brazilian sugarcane-derived ethanol can be profitable at conventional jet fuel pricing levels when the currently available subsidies and credits are applied. With US corn-derived ethanol the more likely feedstock for a US ATJ SAF plant given potential constraints on Brazilian sugarcane-based ethanol exports, however, a substantial price premium above conventional jet fuel prices will be required for SAF production from corn ethanol to be profitable since corn-derived ethanol feedstock features a higher CI and garners lower subsidies and credits.

Without the higher subsidies and other improvements discussed in this article—even if the ATJ SAF is more widely commercialized—more sustainable, lower-carbon air travel will come at a slower, more costly pace than anticipated by current net-zero targets.

References

- IATA, “SAF Deployment,” SAF Policy 2023, https://www.iata.org/contentassets/d13875e9ed784f75bac90f000760e998/saf-policy-2023.pdf.

- US Department of Energy, “DOE Releases Roadmap to Achieve Carbon Neutral Aviation Emissions,” Sept. 23, 2023, https://www.energy.gov/articles/doe-releases-roadmap-achieve-carbon-neutral-aviation-emissions.

- European Council and Council of the European Union, “Council and Parliament agree to decarbonize the aviation sector,” Apr. 25, 2023, https://www.consilium.europa.eu/en/press/press-releases/2023/04/25/council-and-parliament-agree-to-decarbonise-the-aviation-sector/#:~:text=The%20ReFuelEU%20Aviation%20initiative%20is%20part%20of%20the,levels%20and%20to%20achieve%20climate%20neutrality%20in%202050.

- Waguespack, K., “It’s Not Enough—SAF Production Will Need More Than the IRA Tax Credit to Really Take Off (Part 1),” Baker & O’Brien Inc., June 14, 2023, https://bakerobrien.com/article/its-not-enough-saf-production-will-need-more-than-the-ira-tax-credit-to-really-take-off.

- Waguespack, K., “It’s Not Enough, Part 2—Sustainable Aviation Fuel Can Only Fly With More Incentives,” Baker & O’Brien Inc., https://bakerobrien.com/article/its-not-enough-part-2-sustainable-aviation-fuel-can-only-fly-with-more-incentives.

- IATA, “Sustainable aviation fuel output increases, but volumes still low,” Sept. 1, 2023, https://www.iata.org/en/iata-repository/publications/economic-reports/sustainable-aviation-fuel-output-increases-but-volumes-still-low.

The author

Probir Shah ([email protected]) is a senior consultant for Baker & O’Brien Inc. in the Dallas office, where he provides more than 20 years of industry experience focused on the downstream, midstream, and renewable fuels sectors. Before joining Baker & O’Brien, he worked as a principal consultant at Muse, Stancil & Co., and held roles in engineering, operations, planning, and optimization at refineries owned by Delta Airlines subsidiary Monroe Energy LLC, Delek US Holdings Inc., and Phillips 66 Co. He holds MBA (2013) from Southern Methodist University, an MS (2001) in industrial engineering and management from Oklahoma State University, and a BS (1999) in chemical engineering from the Indian Institute of Technology. Shah is a candidate member (business valuation) for the American Society of Appraisers, a certified Six Sigma Green Belt, and is a senior member of the American Institute of Chemical Engineers.