US oil, gas industry capital spending to increase in 2018

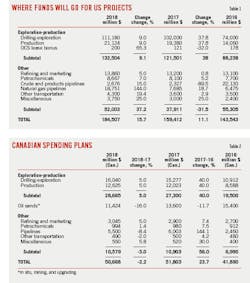

Oil and gas industry capital spending in the US will increase 15% to $184 billion this year vs. last year, according to OGJ's annual capital spending survey.

With commodity prices gaining firmer footing and strong operational results in various shale plays, capital expenditures for exploration and production firms in the US are set to increase this year, albeit partly reined in by a strong focus on capital discipline and efficiency gains.

Continued robust demand for refined products should maintain a stable outlook for refining and marketing. Refiners are developing growth projects integrated with its existing assets and infrastructure. Maintenance capital also will increase this year.

Capital spending for the US petrochemical industry also will continue to surge in 2018, with major capacity additions and as the industry rebounds from disruptions and project delays caused by Hurricane Harvey.

Pipeline construction in 2018 also gains momentum, with plans for natural gas systems making up most of the total.

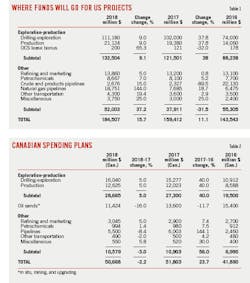

For Canadian operators, this year looks like another sluggish one. Capital investments on oil sands continue to decline.

Worldwide E&P spending is expected to increase this year, the first-year gain in 4 years. Flat-to-modest growth is expected in most regions.

US upstream spending

Capital spending in the US for upstream projects will increase 9% this year, according to OGJ. This growth follows strong capital spending in 2017, when the industry ramped up investment by nearly 40% and concentrated on developing its best oil acreage.

The upstream spending category includes outlays for oil and gas exploration, drilling, production, and offshore lease payments to the US Bureau of Ocean Energy Management.

US shale is driving the pickup, as firmer oil prices trigger a flood of capital into the Permian basin. The US rig count is forecast to increase steadily throughout 2018 to 945 rigs from 900 and average 925 rigs-9% higher than the 2017 average of 850, according to Barclays.

Many companies made their budgets assuming a West Texas Intermediate oil price of $50-55/bbl and a Henry Hub natural gas price of above $3/Mcf.

However, dominating 2018 budget decisions is cash flow over commodity prices. More focus on production optimization, data-driven drilling processes, and capital discipline should help producers reduce finding and development costs, improve returns, while reining in capital spending growth.

In the ongoing cash-flow-driven environment, producers favor lower-cost, short-cycle onshore plays in the US, and reduce allocation of new capital to long-cycle offshore or international plays.

One component of US upstream spending is the total of bonus payments that BOEM collects from lease sales for tracts on the Outer Continental Shelf.

BOEM has two lease sales scheduled for this year: 250 and 251. OGJ estimates that a total of $200 million will be generated by these lease sales.

Firms' spending plans

ExxonMobil Corp.'s capital budget for 2018 is $25 billion, according to preliminary data. That's up from last year's projected investment of $22 billion. And by yearend, ExxonMobil plans to have 30 drilling rigs in the Permian basin, up from 20 there now.

ExxonMobil reported that it would double its holdings in the Permian by purchasing $5.6 billion in assets in the Delaware section of the basin. Longer term, ExxonMobil sees total unconventional output growth of 20%/year through 2025, with growth in the Permian at about 45% through 2020.

Chevron Corp. capex budget for 2018 is $18.3 billion, about 4% less than spending plans in 2017 and lower for a fourth year in a row. However, the company is substantively boosting spending on US shale, especially in the Permian.

For 2018, Chevron's investment in US shale includes $3.3 billion for the Permian and another $1 billion for other shale and tight rock investments.

Chevron's total US upstream capital and exploratory expenditures are planned at $6.6 billion, and international upstream investment is at $9.2 billion. Chevron also plans to spend $2.2 billion on its downstream business, of which $1.4 billion is earmarked for the US downstream.

ConocoPhillips plans an average annual capital budget of $5.5 billion during 2018-20 based on a flat, real WTI price of $50/bbl. The Houston independent also intends to reduce its debt to $15 billion in 2019. The company cut capital spending twice in 2017 to $4.5 billion in 2017.

In 2018, Anadarko Petroleum Corp. expects to make capital investments ranging $4.2-4.6 billion. The company will allocate about 80% of capital toward the Delaware and DJ basins, including Anadarko midstream and the deepwater Gulf of Mexico.

Marathon Oil Corp. reported a $2.3-billion capital budget for 2018. The company's capital spending was $2.2 billion in 2017. More than 90% of the capital will be directed to four US resource plays, including the Eagle Ford and Bakken areas.

Hess Corp.'s 2018 E&P capital and exploratory budget will be $2.1 billion, the same as 2017. The 2018 budget allocates increased capital for continuing exploration and development activities offshore Guyana and for the Bakken, which includes increasing the rig count to six rigs from four. These increases are offset by lower capital allocated to the Gulf of Mexico and Malaysia compared with 2017.

Pioneer Natural Resources Co.'s capital budget for 2018 is $2.9 billion. The budget includes $2.63 billion for the Permian basin.

Devon Energy Corp.'s upstream capital budget in 2018 is $2.2-2.4 billion. This disciplined capital program is expected to be self-funded at a $50/bbl WTI price deck. On a retained asset basis, Devon's upstream capital plans are expected to drive US oil production growth of 14% compared with 2017.

Occidental Petroleum Corp. expects to spend more in 2018, after higher commodity prices and strong operational results in the Permian basin and Middle East.

Murphy Oil Corp. is planning capital expenditures in 2018 to reach $1 billion, slightly higher than its spending in 2017. A third of this total will go towards the US onshore.

Natural gas-focused producer Range Resources Corp. stipulated a sum of $941 million for the year, less than the company's 2017 expenditures of roughly $1.27 billion. About 80% of its 2018 budget is allocated in the gas-rich Marcellus shale play. Notably, the 2018 capital budget will likely reward Range Resources with 11% production growth from the year-ago period.

US refining outlays

Scheduled plant outages, turnarounds, and shutdowns increased by 5% in 2017, with the refining industry seeing the biggest increase. As high demand continues for US products in primary export markets, refiners will increase planned growth and maintenance spend in 2018.

Phillips 66 reported its 2018 capital budget of $2.3 billion, which includes $1.4 billion of growth capital and $900 million of sustaining capital.

The company plans $827 million of capital spending in refining, with $541 million for reliability, safety, and environmental projects. Refining growth capital of $286 million is for small, high-return, quick payout projects primarily to increase clean product yields. Projects include completion of the fluid catalytic cracking unit modernization at the Bayway refinery in Linden, NJ, and FCC optimization at the Sweeny refinery in Old Ocean, Tex.

Marathon Petroleum Corp.'s 2018 capital investment plan includes $2.2 billion of organic growth capital and $190 million of maintenance capital.

This robust organic growth plan includes the addition of eight processing plants representing nearly 1.5 bcfd of incremental processing capacity as well as 100,000 b/d of additional fractionation capacity in the prolific Marcellus, Utica, and Permian basin.

Andeavor planned $525 million as refining sustaining capital, up from $450 million estimated for 2017. Its turnaround spend will be $575 million in 2018, up from $540 million in 2017.

HollyFrontier Corp.'s 2018 capital budget allocates $375-425 million to refining and marketing. It has two turnarounds scheduled for 2018.

Valero Energy Corp.'s 2018 estimated capital expenditures include $1.7 billion as sustaining capital and $1 billion as growth capital. In 2017, the company's sustaining capital was $1.3 billion, and its growth capital was $1.1 billion.

Petrochemicals

With access to cheap and abundant feedstocks, the US remains one of the largest destinations for global petrochemical investment. Since 2010, $85 billion worth of petrochemical projects have been completed or started construction, according to the American Chemistry Council (ACC).

OGJ forecasts that US petrochemical capital investment will increase 7% this year to $8.6 billion, with major capacity additions and the industry rebounds from Hurricane Harvey-related disruptions and project delays.

Total SA, Borealis, and Nova announced that affiliates of the three companies have signed definitive agreements to form the $1.7-billion ethane steam cracker alongside Total's Port Arthur refinery and Total/BASF existing steam cracker.

Indorama is set to restart a long-idled cracker in Lake Charles, La., and Formosa Plastics is due to complete a cracker in Point Comfort, Tex. Shin-Etsu Chemical and Sasol will likely complete their ethylene projects in 2019.

Chevron Phillips Chemical's 2018 capital expenditures will decrease from 2017 due to completion of the US Gulf Coast Petrochemicals Project. The new polyethylene units included in this project started up during third-quarter 2017, while commissioning of the ethane cracker at the Cedar Bayou facility is expected to begin in this year's first quarter.

US pipelines

Expenditures are set to climb this year for pipelines in the US. According to OGJ's most recent Worldwide Pipeline Construction report, plans called for construction of 2,824 miles of gas pipelines and 405 miles of crude and product lines to be completed in the US this year (OGJ, Feb. 5, 2018, p. 72). This compares with 1,156 miles of gas pipelines and 350 miles of crude and product lines estimated in 2017.

OGJ forecasts that spending on these gas lines, including compressor stations, will climb this year to $18.75 billion. Spending for crude and products lines in the US will total $2.6 billion.

Spending in Canada

In Canada, capital expenditures this year for conventional oil and gas exploration, drilling, and production will increase by a modest 5% to $28.6 billion (Can.) following last year's 40% jump.

According to the Petroleum Services Association of Canada's (PSAC) 2018 Canadian Drilling Activity Forecast, a total of 7,900 wells is to be drilled in Canada in 2018. For 2017, PSAC's final revised forecast predicts a yearly total of 7,550 wells.

Investment in the oil sands has fallen each year since 2014, as projects have been completed and brought onstream. According to OGJ, capital spending in the oil sands will drop to about $11 billion this year as few new projects have been sanctioned.

Suncor Inc.'s capital program in 2018 is $4.5-5 billion, a reduction from 2017 of $750 million, and a year-over-year production increase of more than 10%. Upstream project spending is expected to be $3.6-4 billion compared with $5.8 billion in 2017.

With the start of oil production at both Fort Hills and Hebron expected by yearend, Suncor's 2018 capital program is largely focused on sustaining capital given the major planned maintenance programs in both oil sands upgrading operations and downstream refineries including a total plant turnaround at the Edmonton, Alta., refinery.

Cenovus Energy Inc. plans to invest $1.5-1.7 billion in 2018 compared with $1.6 billion in 2017 and $1 billion in 2016. Most of the 2018 budget is allocated to sustain base production at the company's oil sands operations. The remaining capital will primarily support continued construction at the Phase G oil sands expansion at Christina Lake, where costs are coming in below original expectations, and a targeted drilling program in the Deep basin.

Husky Energy Inc.'s total capital spending is expected to be $2.9-3.1 billion in 2018 compared with $2.3 billion in 2017. Upstream project spending is expected to be $2.1-2.3 billion compared with $1.5 billion in 2017. Spending in upstream will be largely allocated to growing the Lloyd thermal portfolio, with 60,000 b/d of new production scheduled to be brought online between 2019 and 2021, and the construction of the West White Rose Project in the Atlantic region with the start of oil production planned in 2022.

Downstream project spending of $710-785 million includes the Lima crude oil flexibility project, which will add 30,000 b/d of additional heavy oil capacity by 2019, and a project to increase heavy oil processing capacity at the Superior, Wisc., refinery.

Canadian Natural Resources Ltd.'s 2018 capital budget is targeted at $4.3 billion, off $500 million from 2017, excluding capital for the Athabasca Oil Sands Project (ASOP) acquisition.

Overall crude oil and natural gas liquids production is targeted to increase from 2017 levels by 23%, ranging 815,000-885,000 b/d in 2018, thanks to the completion of the Phase 3 expansion at Horizon Oil Sands Mining and Upgrading and a full year of production at the AOSP.

Encana Corp. plans to spend $1.8 billion this year, flat with its 2017 level. Encana would focus its 2018 capital spending on its core areas-specifically the Permian basin and the Montney play that straddles Alberta and British Columbia.

TransCanada Corp. will spend $9 billion in 2018 on growth projects and maintenance.

International E&Ps

After decreasing 3% in 2017, international E&P capital spending will increase 4% in 2018, according to the recent annual Barclays E&P spending survey, released in December 2017.

Spending by national oil companies is expected to be up modestly in 2018 again, while international oil companies also increase by mid-single-digits following 15-20% declines each year for the last 3 years.

Flat-to-modest growth is expected in almost every region, with even Latin American expected to bottom out after 4 years of steep declines.

Petrobras and YPF have begun to show a willingness to spend more. Meantime, presalt fields in Brazil, shallow and deep waters in Mexico, shale deposits in Argentina, and offshore areas in Guyana and Suriname are capturing growing interest from global oil companies.

Middle East spending is to be modestly higher in 2018, following a 5% decline in 2017. Barclays estimate Saudi Aramco spending to increase 2% in 2018, following a 5% decline in 2017. Kuwait Oil Co.'s spending will increase 3% in 2018.

Despite production cuts agreed to following OPEC's announcement on Nov. 30, 2017, Barclays expects Russia and the former Soviet Union's upstream spending to increase 6% in 2018, driven by higher spending by almost every company except Rosneft.

Spending in Europe in 2018 will decline 2%, followed by a 5% decline in 2017, driven primarily by Eni SPA and somewhat offset by Statoil AS, which is expected to show a modest increase.

BP PLC expects its 2018 organic capital expenditure to be in the $15-16 billion range. BP's capital expenditure for full year 2017 was $16.5 billion compared with $16.7 billion for the same periods in 2016.

Royal Dutch Shell PLC, according to its 2017 Management Day presentation, expects capital investments between 2018 and 2020 to average $25-30 billion/year. This compares with its 2017 capital spending of $25 billion.

Meantime, offshore spending is poised to fall another 14% in 2018, following estimated declines of 12%, 35%, and 19% in 2015, 2016, and 2017, respectively, according to Barclays. However, 2018 will mark the final year of declines as the impact of structural cost reductions for offshore projects could lead to a rebound in project sanctioning in 2018, which leads to growth in 2019.

About the Author

Conglin Xu

Managing Editor-Economics

Conglin Xu, Managing Editor-Economics, covers worldwide oil and gas market developments and macroeconomic factors, conducts analytical economic and financial research, generates estimates and forecasts, and compiles production and reserves statistics for Oil & Gas Journal. She joined OGJ in 2012 as Senior Economics Editor.

Xu holds a PhD in International Economics from the University of California at Santa Cruz. She was a Short-term Consultant at the World Bank and Summer Intern at the International Monetary Fund.