Caspian pipeline prospects hinge on transparent, logical regulatory frameworks

Whether Caspian oil and gas production will justify multiple export routes and when that might happen have been central strategic issues in the development of this hydrocarbon province.

Considerations for all sides are crucial, but in at least one case they do not conflict: Host governments among the Caspian producing nations, multinational companies operating in the region, and consuming countries that are providing much of the crucial capital and technology all can benefit from strategic alternatives that neutralize commodity price risk.

Differences arise from the power politics underlying particularized interests. Access to diverse pipeline export options that offset regional geopolitics and dilute producer market power may benefit one party but injure another.

The influence, both external and internal, exerted in favor of or against various proposed alignments constitutes the historic conundrum for the region: The great games that have played out continuously over time as control over resource wealth and trade routes is sought.

Price scenarios

Today, roughly 18 months after the depths of the last oil price collapse, two things have become immensely clear, if they were not already.

- A world in which real oil prices are perceived to be consistently low over a critical planning horizon is not one that can easily support multiple oil-export-pipeline routes. Isolated from the best markets by great distances and difficult terrain, trapped by complex geopolitical intrigue and very real security issues, the Caspian becomes, in this scenario, one of the most remote of hydrocarbon provinces.

There are limited options that can be supported. The best positioned pipeline projects in terms of fundamental economics, reserve base, and financial backing are first in line.

Alternative routes will be developed only as they can be supported given the constraints present in a low oil-price case. We, and other analysts, have demonstrated this reasoning (OGJ, Apr. 19, 1999, p. 29).

- But a world in which real oil prices are perceived to be consistently high over a critical planning horizon presents quite a different story. In this case, the Caspian becomes less remote and more essential to the world energy balance (OGJ, June 12, 2000, p. 76).

A rationale can develop for surplus transportation capacity in the region, and Caspian "pipeline politics" can take new strategic twists.

There exists at present an opportunity to observe what a higher oil-price case might mean for the region. However, clearly, there are dozens if not hundreds of caveats at play in either case.

Determined efforts can move less attractive pipeline projects, in economic terms, to the front of the list if they satisfy critical strategic interests. The current high prices for oil can easily slump if demand slackens and excess supplies develop.

And while oil prices bear some influence on the natural gas transportation picture for the Caspian, the residual constraints for gas transportation options become much more evident at the nexus between low oil-price and high oil-price world views.

Unquestionably, a low oil-price world implies conditions not only on the supply side but for demand as well. We have learned from the 1997 Asian meltdown that macroeconomic disruptions among consuming countries can spill across emerging markets, including "transition" economies that were part of or heavily influenced by the former Soviet Union (FSU) and that comprise part of the current and future demand for natural gas resources.

Key questions include the following:

- Does the apparent shift in industry psychology toward higher oil prices reflect market fundamentals or short-lived variables?

- With recent discoveries, is the Caspian proving to be the kind of hydrocarbon province it is hoped to be? Or, do sufficient doubts remain about the ultimate rank of Caspian resources to cast doubt on a multiple-pipelines thesis?

- What does the current situation and market psychology imply for the future? Are there breakthrough possibilities for the region's abundant gas resources that would cut the Gordian knot on competing transportation options and the dependence on regional demand (OGJ, Nov. 15, 1999, p. 51)?

- Finally, how can investors and host governments in the region navigate for the longer term through the kinds of sharp commodity price cycles evident since 1997?

State of the world

We begin by asking: What do we believe to be true about the world today and how does that belief system impact prospects for the Caspian?

Most important is the growing willingness to question the adequacy of oil supplies in light of the rebound in demand and prices during 1999. Production capacity constraints in key petroleum provinces such as Venezuela and Iran as a result of sharp investment reductions during the price collapse and political, economic, or natural disruptions pose what many think are serious mid-term risks.

A more rapid recovery among countries most heavily affected by the 1997 "Asian flu" has introduced new concerns with regard to supply security.

The psychological shift with regard to oil market outlooks since April 1999 is rooted in critical indicators. For the first quarter of 1999, the price of West Texas Intermediate averaged about $12/bbl, a significant increase over the December 1998 price (Table 1).

Although cohesion within the Organization of Petroleum Exporting Countries, combined with improved demand forecasts for Asia, signaled an upward trend, companies continued to require new projects to be commercially viable with prices as low as $10-12/bbl.

The WTI price moved significantly higher in late 1999 through 2000 to date, reaching $34-35/bbl in early summer. Along with these price movements has come a view that higher prices may be the rule for some time to come.

As a consequence, the Saudi announcements regarding an additional 500,000-b/d increase in production triggered a lower price only temporarily.

In addition, doubts have been raised about the excess production capacity of 4-5 million b/d usually associated with Middle Eastern producers. One reason the Saudi announcement did not have a lasting downward impact on prices is concern about the kingdom's ability to increase output.

As usual, there are many offsetting factors that could combine to disrupt current thinking and perceptions. High on the list is whether economic recovery in Asia is sound, or whether insufficient 'housecleaning' was undertaken to eliminate financial excesses and inefficiencies.

During the past decade, Asia has supplied most of the incremental growth in oil demand, a trend that will only increase. In this swing consuming region, economic fortunes in Asia will dictate oil-market volatility.

Perhaps even higher on the list is the effort of the US Federal Reserve Bank to administer a "soft landing" of the American economy. The astonishing US economy buffered the Asian tidal wave and provided crucial liquidity to prevent severe global repercussions.

A failure in the Fed's efforts, leading to a "hard landing," could push the US economy into a recession, which would significantly dampen the world oil demand. In either situation-economic performance in Asia or the US and spillover from each-higher crude oil prices are not positive.

Thus, while strong arguments can be made for higher average crude prices, there is wide acknowledgement that prices greater than $30/bbl may not be sustainable.

Discord and confusion about these signals introduces a third important risk, a collapse in OPEC discipline. Apart from any real constraints in production capacity, the waxing and waning of the members' abilities to coordinate and police themselves persist as a background factor.

Nevertheless, current forecasts for oil prices over the next several years range from the low to high $20s/bbl, strikingly different from the magical $18-22/bbl range of a few years back or even the occasional doomsday forecasts of late 1998 of $5/bbl.1

In this environment, Caspian resources provide a valuable alternative source of oil supply. Moreover, the costs of developing offshore fields and building necessary pipelines are more easily financed. Even natural gas, as an alternative fuel, should benefit from high oil prices. This is the context within which our following update of Caspian prospects should be viewed.

Caspian potential

In April 1999, industry estimates of proved oil reserves of Azerbaijan, Kazakstan, Turkmenistan, and Uzbekistan were 15-40 billion bbl. Our approximation of 32.3 billion bbl provided some middle ground. Proved gas reserves were estimated at about 230 tcf.

There have been two significant discoveries in the region that make 32 billion bbl of oil more realistic and that will probably trigger upward revisions for natural gas reserves.

First is the discovery of significant gas reserves off Azerbaijan at Shah Deniz field. The second is the discovery of Kashagan field off Kazakhstan. It has been long argued that the Caspian Sea would be a prolific resource base, and these two finds certainly support this thesis.

Estimates of gas reserves in Shah Deniz are 25-35 tcf. After several test wells, initial estimates for Kashagan field indicate reserves greater than 8 billion bbl, although estimates by local officials reach as high as 40 billion bbl.

We predicted that Kazakhstan's output could reach 2.20 million b/d in 2010 under an optimistic scenario (OGJ, Apr. 19, 1999, p. 29). If Kashagan lives up to its promotion, this number looks fairly realistic.

Oil production in Azerbaijan has increased about 34% from 190,000 b/d in 1998 to 255,000 b/d in 1999. And there was an overall 90,000-b/d increase from 0.99 million b/d in 1998 to 1.08 million b/d in 1999 for the region (Table 1; OGJ, Dec. 20, 1999, p. 92). The US Energy Information Administration's projection for 2000 of 1.27 million b/d indicates a more optimistic increase.

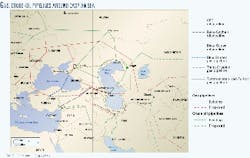

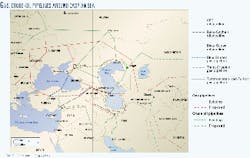

Caspian crude-oil pipelines

Table 2 is revised from an earlier version (OGJ, April 19, 1999, p. 31).

The Caspian Pipeline Consortium pipeline is expected to be in operation by the end of 2001. In the past, this would have ruled out any other large pipeline construction during the short term. The emerging psychology with respect to world oil markets and the recent discovery of Kashagan field, however, improve chances of the long-debated Baku-Ceyhan line.

Indeed, the case could be made that a Baku-Ceyhan pipeline would provide critical strategic surplus capacity both to meet world oil demand and balance the regional market in order to offset potential price manipulation posed by a second Iranian pipeline and associated oil-swap proposal.

The Baku-Ceyhan line would provide a cost-saving transportation option for Turkmenistan. In addition, Baku-Ceyhan would provide an alternative transport route for additional Kazakh production beyond CPC capacity.

Without the Baku-Ceyhan alternative, swaps with Iran could be the main alternative for about 500,000 b/d of Turkmen oil and about 250,000 b/d of Azeri or Kazakh exports by 2010.

Iran might easily ask captive exporters to pay in the neighborhood of $7/bbl to move oil in this situation (that is, slightly less than the cost of next-best alternative, railways through Russia to Baltic ports or through Georgia to Black Sea ports), in contrast to about $3/bbl with Baku-Ceyhan as a competing transportation option.

Other alternatives-an eastward route to China, or additional capacity or cooperation from Russia-are unlikely. Although we include the Chinese pipeline in Table 2, at this stage, this option does not appear to compete seriously with Baku-Ceyhan.

Lastly, Turkey is likely to increase its efforts to prevent passage of additional tanker traffic through the Bosporus Strait. The country will probably reach some level of success, as indicated by the International Maritime Organization's apparent support of Turkish views.

Recent guarantees by the Turkish, Georgian, and Azeri governments for Baku-Ceyhan also increase the chances of this pipeline. Turkey guarantees to cover costs greater than $1.3 billion for the Turkish section of the pipeline, while Georgia and Azerbaijan are willing to pay for damages that may be caused by delays during the construction of the pipeline in their territory.

Caspian natural gas pipelines

Turkey remains the primary market for Caspian natural gas, at least in the short to medium term (Table 3).

The Blue Stream pipeline is closer to reality with financing of $1.7 billion for the offshore section in line2 and ratification of tax exemptions in the parliaments of both Russia and Turkey. Offshore construction awaits Saipem SPA's specially equipped ship to finish its tour of duty in the Gulf of Mexico. Construction of the Samsun-Ankara section in Turkey has already started.

With rapid development of the Shah Deniz discovery, Azerbaijan has become a strong contender in the race to supply Turkey with gas. It may even be possible to renovate existing pipelines in Azerbaijan and Georgia to bring gas to Turkey.

Early estimates discussed in the Turkish parliament indicate that Azeri gas could cost as little as 40% of the cost of Turkmen gas.

These developments significantly hurt the chances of the Trans-Caspian Gas Pipeline (TCGP). Russia appears to have won the gas race to Turkey.

Somewhat ironically, Russia will likely supply Turkmen gas via the Blue Stream pipeline. There is now a long-term contract between Russia and Turkmenistan for 700 bcf/year that, although not as strong a commitment as Russia was hoping for, represents an important step for Blue Stream.

Turkmenistan can also sell up to 210 bcf/year of gas to Iran, and Iran can supply Turkmen gas to Turkey when the Turkish portion of the pipeline is completed in September 2001. That amount can be increased if the capacity of Turkmenistan-Iran connection is expanded.

Currently, it appears that the Turkmen Pres. Niyazov considers these sales more consistent with the country's immediate need for hard currency.

In response to these developments for Blue Stream, PSG International Ltd., a joint venture of US firms Bechtel Enterprises Inc. and GE Capital Structured Finance Group, is moving to abandon its development of TCGP. Royal Dutch/Shell, however, appears determined to bring Turkmen gas to Turkey via a route outside of the Russian and Iranian spheres of influence.

Strategically, the TCGP remains a valuable option for Turkmenistan in the long run when Russia and Iran may not need Turkmen gas to supply Turkey or their other customers.

Rumors about Niyazov's frustration with PSG's unwillingness to pay $500 million up front for the construction of the TCGP are probably well-founded, but the Turkmen government is certainly not without options.

As with every host government in the region, sound policies that support high-risk, nation-building projects that are essential to the futures of these countries would go a long way.

Overall, early winners in the Caspian pipeline game have started to emerge, setting a tone for the future. Russia and Turkey appear to be the frontrunners in the race for crude oil and natural gas, the former as a supplier and transporter and the latter as a willing recipient of much needed hydrocarbon resources. The CPC pipeline is finally near completion, and Blue Stream is under construction.

In our analysis, the prospects for Baku-Ceyhan significantly improve with the Kashagan discovery and a more positive world oil market psychology. Kazakhstan and Azerbaijan will export their oil with increasing ease in the near future, while Georgia should be able to increase its transit revenues, although the impact of transit fees on long-term energy development and trade should be questioned.

Azerbaijan enjoys a privileged position as a key supplier in the western Caspian: The country is very likely to become a hefty gas exporter to Turkey ahead of Turkmenistan.

While currently selling more gas to Russia and Iran than it has been able to in recent years, Turkmenistan appears to be the only potential loser. With the possibilities for a trans-Caspian gas pipeline diminished, Turkmenistan remains dependent on these two gas-rich countries that will, eventually, substitute their domestic gas for Turkmen gas.

OPEC must be considered an affected party as the Caspian becomes established. The oil cartel will face an interesting dilemma should Caspian hydrocarbons rise to prominence. Would OPEC abandon its market dominance, as DeBeers has its cartel status for diamonds, to pursue strategies that reflect Caspian producers as new, aggressive entrants? This query both depends upon and would heavily affect oil and gas price outlooks.

Cycles

Experience in the Caspian these recent years has been instructive.

The region is, in many respects, emblematic of the ultimate challenges the global oil and gas industries face to bring remote resources to distant markets, with inadequate and costly-to-develop infrastructure and planning environments fraught with risk and uncertainty.

In a sense, activity has settled down to a set of logical investment projects coming to fruition and predictable positions for key players. But it is an unsure world, always subject to change and revision, and an industry notorious for volatile conditions and sharp business cycles.

Two lessons appear:

- It is clear that in a market-oriented, globalized, competitive world where capital, people, technology, and ideas flow to the best opportunities, host governments that provide the most transparent, economically sound policy and regulatory frameworks will benefit most in the longer term.

Capriciousness bears a high cost. Indeed, in the end, a host government's most effective weapon in achieving long-term goals and objectives is the framework it puts in place to support successful commercial ventures.

In this vein, there is still a great deal to be learned in the Caspian, and little time.

- 2. It is in the industry's benefit to push in a consolidated fashion for solid frameworks. These are crucial to long-term prospects in a region like the Caspian. A hallmark of the oil industry is a traditional willingness to "dance with the devil." That can bear a high cost as well.

References

- "Drowning in Oil," The Economist, Mar. 6, 1999.

- World Gas Intelligence, May 12, 2000, p. 12.

The authors-

Michelle Michot Foss is director of the Energy Institute at the University of Houston's College of Business Administration. She has 23 years' experience as an analyst of US and international energy, minerals, and environmental markets and policy. Michot Foss coordinated UH participation, through the institute, in the US Agency for International Development (AID)/Hagler Bailly consortium for technical support and training related to oil and gas development in Central Asia and Ukraine. She holds a BS in biology (geology minor) from the University of Southwestern Louisiana, Lafayette, an MS in mineral economics from Colorado School of Mines, Golden, and a PhD in political science from the University of Houston.

S. Gürcan Gülen is a research associate in the Energy Institute at the University of Houston's College of Business Administration. He participated in the US AID/Hagler Bailly Services consortium's training of oil and gas professionals in Central Asia. He currently works on gas/power convergence and industry restructuring developments in Europe, Latin America, and the Caucasus/Black Sea region.

Gülen holds a PhD in economics from Boston College and a BA in economics from Bogaziçi University, Istanbul.

Bhamy V. Shenoy is a manager at Hagler Bailly Services, Houston, for US AID-sponsored projects undertaken by Hagler Bailly. He is deputy project manager for Republic of Georgia oil and gas sector reform and task leader, Central Asian Republics: Regional Energy Sector Initiative.

Shenoy spent 21 years with Conoco Inc., in various positions. He holds a BTech in mechanical engineering, Indian Institute of Technology-Madras; an MS in industrial engineering, Illinois Institute of Technology-Chicago; a PhD in business administration, University of Houston; and has attended the Executive Program in Business Administration at Columbia University, New York City.