IEA: Oil markets lie amid tumultuous interplay of forces

Oil markets are being impacted by varous forces, with the potential for supply losses from new sanctions on Russia and Iran occurring amidst an increase in OPEC+ production and the prospect of increasingly bloated oil balances, the International Energy Agency (IEA) said in its latest Oil Market Monthly Report (OMR).

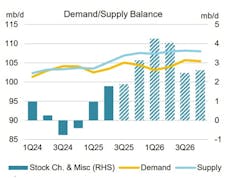

Oil demand

World oil demand is projected to rise by 740,000 b/d year-on-year(y-o-y) in 2025, the September report said, a slight increase from last month's report, as weaker oil prices and a somewhat improved economic outlook combine with firm reported deliveries in a number of advanced economies, according to IEA.

“Resilient OECD oil demand in the face of an uncertain macro climate has been a recurring theme all year and was corroborated by broadly robust actual and preliminary data for June, July and August in countries such as the US, Germany, Italy and Korea,” IEA said.

As a result, OECD demand growth of 80,000 b/d y-o-y in first-half 2025 has exceeded expectations, supported by lower oil prices, but is forecast to move into contraction in the remainder of the year, assuming a return to normal winter temperatures, leaving 2025 annual oil use broadly flat.

“Still, recent non-OECD consumption remains comparatively muted, exemplified by Chinese deliveries that undershot expectations in July, resulting in essentially flat y-o-y oil demand growth. As a result, the non-OECD accounts for the entirety of our 310,000 b/d downward revision to global oil demand growth since the start of the year,” IEA noted.

Oil supply

In August, global oil supply reached a record 106.9 million b/d as OPEC+ continued to roll back production cuts and non-OPEC+ supply hovered near all-time highs. Current projections indicate that world oil production will increase by 2.7 million b/d to 105.8 million b/d this year, and by an additional 2.1 million b/d to 107.9 million b/d next year. Of this growth, non-OPEC+ countries are expected to contribute 1.4 million b/d this year and just over 1 million b/d next year.

“The Group of 8 OPEC+ countries plans to raise its output target by 137,000 b/d in October. If continued at this pace, lifting the full 1.65 million b/d tranche of cuts would take 12 months, leaving the 22-member alliance with 2 million b/d of supply cuts still in place. The actual supply boost in October will be less than the target increase, as Iraq, the UAE, Kuwait and Kazakhstan already pump 1.1 million b/d above their quotas, while others, including Russia, are bumping up against capacity constraints, according to our estimates,” IEA said.

“As of September, OPEC+ will have ramped up actual crude output by 1.5 million b/d since first-quarter 2025, well below the announced target of 2.5 million b/d. The biggest increase has come from Saudi Arabia and other core Middle Eastern producers. However, tanker tracking data indicate that the majority of the additional volumes have been absorbed by regional refinery activity and power generation use rather than exported out of the region.”

Meantime, non-OPEC+ oil supply growth continues apace, with output from the US, Brazil, Canada, Guyana, and Argentina at or near all-time highs.

Refinery crude processing jumped by 400,000 b/d to an all-time high of 85.1 million b/d in August. However, it is projected to decline by 3.5 million b/d through October due to increased seasonal maintenance. Global refinery crude throughputs are expected to average 83.5 million b/d in 2025 and 84 million b/d in 2026, reflecting a slowdown in growth from 580,000 b/d to 540,000 b/d. Refining margins remain robust, as a significant drop in diesel crack spreads was partially balanced by improved gasoline profitability.

Observed global oil stocks rose by 26.5 million bbl in July, extending gains since start of the year to 187 million bbl. Inventories remained 67 million bbl below the 5-year average, despite a significant surplus built up in China in recent months. OECD industry stocks were up by 6.9 million bbl, in line with the seasonal trend. According to preliminary data for August, global oil stocks were largely unchanged as lower oil on water was offset by OECD builds.

Oil prices

Crude oil prices experienced a slight decline in August, with ICE Brent futures dropping about $2/bbl m-o-m to settle at $67/bbl. Geopolitical tensions escalated, fueled by diminishing expectations for a near-term peace deal between Russia and Ukraine. Meanwhile, concerns about a potential oversupply kept a lid on any upward price movement, leading to a persistently bearish sentiment among investors.

“China continues to stockpile crude oil, helping keep Brent crude futures in slight backwardation. Toughened sanctions on Iran and Russia have so far had a relatively modest impact on supply and trade flows, even as exports from both countries have been trending lower in recent months. The EU ban on imports of refined products derived from Russian crude oil from the start of 2026 may yet curb output and upend trade patterns in the coming months,” IEA said.