WoodMac: Global LNG market could split if EU carbon tax imposed on imports

The global LNG market could transform and potentially bifurcate if the European Union (EU) extends its carbon taxes to include LNG imports, according to a new Horizons report from Wood Mackenzie.

The EU has extended its Emissions Trading Scheme (ETS) to shipping, meaning that from 2024, LNG cargoes entering Europe will be subject to a carbon tax. If the trade bloc further tightens methane regulations or includes LNG in its Carbon Border Adjustment Mechanism (CBAM)–effectively placing an import duty on LNG at prevailing ETS carbon prices–the global LNG market would split, Wood Mackenzie said in the report.

“If the EU decides to apply these levies, then this will push European gas prices up but also bifurcate the global LNG market, creating a two-tier LNG market,” said Massimo Di Odoardo, vice-president of gas and LNG research at Wood Mackenzie. “If taxes were limited to the EU, or even extended to Japan and South Korea, trade flows would likely be optimized elsewhere to mitigate the impact.”

The environmental credentials of LNG are under increasing scrutiny, according to the report. Despite emitting about half the carbon dioxide (CO2) of coal when combusted, the LNG value chain remains highly carbon intensive and plagued by methane losses.

However, it adds that while LNG players are actively working to reduce the greenhouse gas (GHG) footprint of their projects, the reluctance from buyers to pay a premium for lower-emission LNG has so far curbed sellers’ appetite to commit to major investment to reduce carbon intensity.

US LNG, one of worst performers

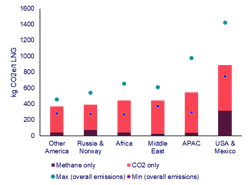

Not all LNG projects are equal. Measured in kg of CO2 equivalent (kg CO2e), methane accounts for 5-15% of overall carbon intensity in LNG projects outside the US, the report noted. But for LNG projects in the US, methane can account for as much as 25-40%. This largely due to higher levels of methane losses caused by extensive use of pneumatic devices and compressors associated with shale gas production.

“With a range of 800 to 1400 kg CO2 equivalent per tonne (CO2e/t) of LNG, the US has some of the world’s highest-emitting projects, with upstream reservoir type and pipeline distance to LNG plants adding to their high methane intensity,” said Di Odoardo.

He adds that projects with the lowest carbon emissions will gain from an import tax on emissions and targeting premium markets will boost trading profitability. However, proximity to premium markets will be key, with Qatar and Mozambique requiring high carbon prices to be lured away from proximate markets in emerging Asia, which are unlikely to introduce an import tax on emissions.

High carbon taxes needed to decarbonize LNG

Reducing methane emissions remains a low-hanging fruit, with progress being made in different countries, supported by tightening domestic methane regulations, the report said. A methane import tax will help provide additional economic incentives while limiting LNG price upside. In this scenario, exporting countries will also be encouraged to introduce domestic levies and retain taxed revenues, Di Odoardo continued.

However, Wood Mackenzie concludes that when it comes to overall carbon emissions, taxes imposed only in Europe will not achieve the required goal of large-scale decarbonization of LNG projects globally and a bifurcate LNG market would be instead the most likely outcome.

“If there is to be any material impact, a carbon price closer to $200/tonne CO2e will be required for LNG imports,” Di Odoardo said. “Additionally, this would have to be introduced on a global level for it to be truly effective in reducing carbon intensity and that is unlikely to happen. For now, all eyes will be on Europe to see what it does next.”