Rystad: Global E&P capex will reach 13-year low

Global capital expenditures (capex) of exploration and production companies are expected to fall by up to $100 billion in 2020, down about 17% from 2019, Rystad Energy predicts using its latest baseline scenario of $34/bbl in 2020 and $44/bbl in 2021.

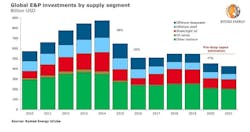

E&P capex in 2019 reached $546 billion, according to Rystad Energy estimates, having slightly recovered from a 2-year slump in 2015 and 2016 before diving to around $510 billion from 2014’s historical high of $880 billion.

Capex volumes in 2020 will be about $450 billion, the lowest in 13 years by Rystad Energy estimates. Estimates before the coronavirus pandemic indicated E&P would remain flat year-on-year.

“As April approaches, when OPEC+ producers are expected to flood the market with even more additional oil, Brent prices are now at nearly $25/bbl and are likely to decline even further.”

In a low case scenario, where Brent averages $25/bbl in 2020, global investments may plunge to around $380 billion this year, falling to almost $300 billion in 2021, a 14-year and a 15-year low, respectively.

“As companies are now losing solid oil market ground for a second time in recent years, it will be far more challenging to act quickly and reach the same high level of investment revision without taking a heavy toll on E&P’s performance,” said Rystad Energy upstream analyst Olga Savenkova.

The cuts will be achieved primarily through reduced US shale activity, delays to projects yet to reach the final investment decision (FID), deferred exploration activity, and cost cuts within development and production for conventional assets.

“As the most flexible of the supply segments in terms of cost reduction, US shale players are expected to reduce their investments by about 30% year-on-year. These measures will be quickly reflected in the oil market supply, with shale oil supply growth set to slow down in 2020.”

Majors’ E&P spending

Saudi Aramco cut its upstream capital expenditure by 20% to protect its balance sheet amid declining oil prices. However, despite the turbulent oil market, Rystad expects the company to go ahead with strategically important projects, having one of the lowest costs per bbl within the industry.

ExxonMobil is considering at least a 20% investment cut, but the plans have not yet been finalized. Considering the company’s underperformance, even deeper cuts may be required to meet most of its important operational targets; it posted weak numbers for the fourth quarter of 2019, announced $20 billion worth of divestments planned for 2020, and maintains big ambitions for exploration and development in Guyana.

Shell will embrace a 20% total cut strategy, but upstream budgets will likely only see reductions of about 14%. The company also is committed to a divestment program of more than $10 billion, which could prove challenging to conduct in the current market.

BP has announced potential plans for a 20% cost reduction. Even though the company holds a geographically diverse and resilient portfolio, its $15 billion asset-sale target might not be accomplished, Rystad said.