EIA STEO: Falling global inventories, demand growth seen lifting oil prices

Higher crude oil prices over the past month reflect declining global oil inventories, geopolitical events, and increasing expectations for global economic and oil demand growth, the US Energy Information Administration said in its October Short-Term Energy Outlook.

EIA estimates that global oil inventories fell 500,000 b/d in the third quarter, marking the third consecutive quarterly draw, the longest such stretch since 2013-14.

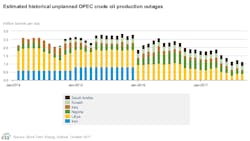

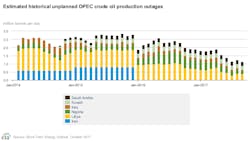

Contributing to the global withdrawals has been declining crude oil production from the Organization of Petroleum Exporting Countries, which in the third quarter averaged 32.9 million b/d, down from 33.4 million b/d in November 2016 when the group collectively pledged to reduce output by 1.2 million b/d.

Libya, which is exempt from any production reductions, increased its crude output in September, but a shutdown at Sharara oil fields at the beginning of October presents uncertainty about the country’s longer-term production potential, EIA said.

Total OPEC crude production in the fourth quarter is forecast to decline from the third quarter to 32.7 million b/d.

Although unplanned OPEC supply outages remain low, crude prices may have increased based in part on a Sept. 25 referendum in the Kurdistan Region of Iraq, where most people voted for independence. Turkey, which sided with Iraq’s central government in opposing the vote, threatened to disrupt pipeline flows of 500,000 b/d of crude produced in Kurdistan that is exported from the Turkish port of Ceyhan.

Stronger demand, prices possible

EIA noted that economic conditions appear to be strengthening globally, which could contribute to oil demand growth in 2018.

Manufacturing Purchasing Managers’ Indexes (PMI) in many countries continued to indicate expanding activity in September. The PMI is a leading indicator of economic activity, surveying purchasing managers in manufacturing businesses on expectations of output, new orders, employment, and other measures. An index level above 50 indicates expansion in manufacturing activity.

Among the 27 countries’ manufacturing PMI surveys in September—10 of which are from outside the Organization for Economic Cooperation and Development—25 countries had readings greater than 50, with the median at 53. Nine countries had survey readings greater than or equal to 55, and 2 had readings at 60 or higher.

Continued expansion of business activity in these countries could raise expectations for global gross domestic product growth in the fourth quarter and indicate higher consumption of crude and petroleum products, EIA explained.

Expanding manufacturing and economic activity is a particularly important source of growth in distillate fuel consumption. EIA forecasts global liquid fuels consumption to grow 1.6 million b/d in 2018 and to be more than 100 million b/d consistently by mid-2018.

EIA forecasts Brent crude spot prices to average $52/bbl in 2017 and $54/bbl in 2018, which is $1/bbl higher in 2017 and $2/bbl higher in 2018 compared with last month’s forecast. Brent spot prices averaged $56/bbl in September, an increase of $4/bbl from the average in August.

West Texas Intermediate average crude prices are forecast to be $3.50/bbl lower than Brent prices in 2018. New York Mercantile Exchange contract values for January 2018 delivery that traded during the 5-day period ending Oct. 5 suggest that a range of $40-65/bbl encompasses the market expectation for January WTI prices at the 95% confidence level.

US oil industry changes

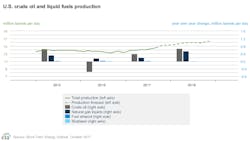

EIA estimates US crude production in September averaged 9.3 million b/d, an increase of 250,000 b/d from the August average. Following Hurricane Harvey, Gulf of Mexico crude production in September is estimated to have increased to 1.7 million b/d, up 70,000 b/d from the August level.

The agency forecasts total US crude production in 2017 to average 9.2 million b/d, down 100,000 b/d from last month’s forecast. It expects output in 2018 to average 9.9 million b/d, up 100,000 b/d from last month’s forecast.

The oil industry on the US Gulf Coast began to resume normal operations throughout September after refineries and ports were shut down in late August because of Hurricane Harvey. Gulf Coast refinery utilization reached 86% for the week ended Sept. 29, down 10% from the week ended Aug. 25 but only 5% below 5-year average utilization for this time of year.

Hurricane Irma, which made landfall in Florida on Sept. 10, did not significantly affect US crude supply or refining operations, but because of increased evacuation-related demand, tanker truck limitations, and power outages, many retail gasoline stations were out of service.

After reaching a 2-year high of $2.69/gal on Sept. 11, US regular gasoline retail prices fell to an average of $2.57/gal as of Oct. 2. EIA forecasts the US regular gasoline retail price will average $2.49/gal in October and fall to $2.33/gal in December.

US gas prices seen rising

The front-month futures price of gas for delivery at Henry Hub on Oct. 5 settled at $2.92/MMbtu, down 15¢ from Sept. 1. Futures prices declined in early September largely because of reduced demand related to Hurricane Irma.

Most electricity generation in Florida is gas-fired, and electricity generation in Florida on Sept. 11 was 41% lower than the average of the first 7 days of September. Injections of working gas into underground storage exceeded market expectations and historical averages for the first 3 weeks in September, which further contributed to lower prices.

The average Henry Hub spot price in September was $2.98/MMbtu, up 8¢ from the August level. Expected growth in gas exports and domestic gas consumption in 2018 contribute to the forecast Henry Hub price rising from an annual average of $3.03/MMbtu in 2017 to $3.19/MMbtu in 2018, EIA said.

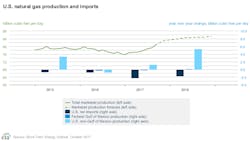

LNG export capacity is expected to increase with LNG exports projected to exceed 3 bcfd in 2018, 66% higher than in 2017. Increased takeaway capacity out of the Marcellus-Utica shale plays because of several new projects, including the Rover and Nexus Gas Transmission pipelines, also will help increase production.

US dry natural gas production in 2017 is forecast to average 73.6 bcfd, an 800-MMcfd increase from the 2016 level. Gas production in 2018 is forecast to be 4.9 bcfd higher than the 2017 level.

EIA forecasts that average household expenditures for all major home heating fuels will rise this winter mostly because of expected colder weather (OGJ Online, Oct. 11, 2017). Average increases vary by fuel, with gas expenditures forecast to rise by 12%, home heating oil by 17%, electricity by 8%, and propane by 18%.