BP Energy Outlook: Global energy demand to grow 30% to 2035

According to the 2017 edition of BP’s Energy Outlook, global energy demand will increase by around 30% to 2035, an average growth of 1.3%/year, driven by increasing prosperity in developing countries, partially offset by rapid gains in energy efficiency.

“The global energy landscape is changing,” said Bob Dudley, BP group chief executive. “Traditional centers of demand are being overtaken by fast-growing emerging markets. The energy mix is shifting, driven by technological improvements and environmental concerns. More than ever, our industry needs to adapt to meet those changing energy needs.”

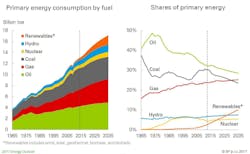

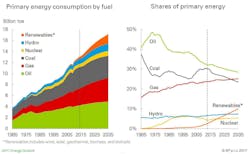

While non-fossil fuels are expected to account for half of the growth in energy supplies over the next 20 years, the outlook projects that oil and gas, together with coal, will remain the main source of energy powering the world economy, accounting for more than 75% of total energy supply in 2035, compared with 86% in 2015.

Products source oil demand growth

According to the outlook, oil demand grows at an average rate of 0.7%/year, although this is expected to slow gradually over the period. The transport sector continues to consume most of the world’s oil with its share of global demand remaining close to 60% in 2035. However, non-combusted use of oil, particularly in petrochemicals, takes over as the main source of growth for oil demand by the early 2030s.

“The possibility that the most important source of growth in oil demand in the 2030s won’t be to power cars or trucks or planes, but rather used as an input into other products, such as plastics and fabrics, is quite a change from the past,” said Spencer Dale, BP’s group chief economist.

The transport sector accounts for around two thirds of the growth in oil demand. Within that, oil demand for cars increases by around 4 million b/d, underpinned by a doubling in the global car fleet. The number of electric cars is assumed to increase from 1.2 million in 2015 to around 100 million in 2035, around 5% of the global car fleet.

The outlook constructs two illustrative scenarios to consider the impact of the broader mobility revolution affecting the car market, including autonomous cars, car sharing, and ride-pooling.

“The impact of electric cars, together with other aspects of the mobility revolution, such as self-driving cars, car sharing, and ride pooling, is one of the key uncertainties surrounding the long-term outlook for oil” said Dale.

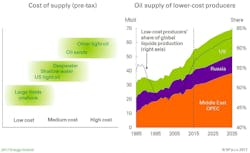

The slowing rate of oil demand growth is contrasted by the abundance of global oil resources. The outlook speculates that the abundance of oil may cause low-cost producers, such as Middle East OPEC, Russia, and the US, to use their competitive advantage to increase their market share at the expense of higher-cost producers.

The outlook also forecasts that all of the demand growth for oil in the period to 2035 comes from emerging markets, with China accounting for half.

Gas overtakes coal

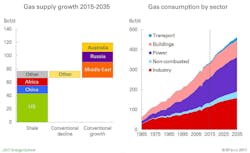

Gas grows more quickly than either oil or coal over the outlook, with demand growing an average 1.6%/year. Its share of primary energy overtakes coal to be the second-largest fuel source by 2035.

The main growth comes from China, Middle East, and the US. In China, growth in gas consumption outstrips domestic production, so that by 2035 imported gas comprises nearly 40% of total consumption, up from 30% in 2015. In Europe, the share of imports rises from around 50% in 2015 to more than 80% by 2035.

Shale gas production accounts for two thirds of the increase in gas supplies, led by growth in the US. LNG growth, driven by increasing supplies in Australia and the US, is expected to lead to a globally integrated gas market anchored by US gas prices.

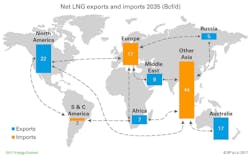

The outlook expects LNG supplies to grow rapidly to account for more than half of traded gas by 2035. This increase is led by supplies from the US, Australia, and Africa. Around a third of this growth occurs over the next 4 years as series of projects currently under development come on-stream.

China pushes renewable growth

Coal consumption is projected to peak in the mid-2020s, largely driven by China’s move towards cleaner, lower-carbon fuels. India is the largest growth market for coal, with its share of world coal demand doubling from around 10% in 2015 to 20% in 2035.

Renewables are projected to be the fastest growing fuel source, growing at an average rate of 7.6%/year, quadrupling over the outlook, driven by increasing competitiveness of both solar and wind.

China is the largest source of growth for renewables over the next 20 years, adding more renewable power than the EU and US combined.

Carbon emissions growth slows

Carbon emissions are projected to grow at less than a third of the rate seen in the past 20 years, by an average of 0.6%/year vs. 2.1%/year, reflecting gains in energy efficiency and the changing fuel mix.

If achieved, it would be the slowest rate of emissions growth for any 20-year period since records began in 1965. However, carbon emissions from energy use in the base case are still projected to grow throughout the period, by about 13%. This is far in excess of the International Energy Agency’s 450 Scenario, which suggests that carbon emissions need to fall by around 30% by 2035 to have a good chance of achieving the goals set out in Paris.