IOCs recorded high reserve replacement, low F&D costs in 2018, analysis shows

With 2018s 10-Ks and 20-Fs now filed to the US Securities and Exchange Commission, details on integrated oil companies (IOCs)’ reserve replacement and finding and development costs (F&D) have been displayed.

According to an analysis by Simmons Energy, an energy investment banking firm, major themes from 2018 data include impressive organic reserve replacement (a group average of 153%), leading to F&D costs of $8.20/boe, a multi-year low. The related companies include ExxonMobil, ConocoPhillips, Chevon, Equinor, BP, Shell, and Total.

“We believe the downward move in F&D of late should be indicative of future depreciation, depletion and amortization (DD&A) trends,” Simmons Energy said.

According to Simmons Energy, strong reserve replacement (153%) is underpinned by a combination of factors including improving economics vis-a-vis increasing oil prices, sustainably lower cost structure, expanding US shale presence leading to reserve extensions, slightly higher FID activity, diminished PSC exposure compared to previous cycles and re-booking of previously removed oil sands bbls.

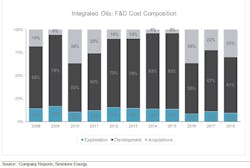

Spending allocations

Notable spending allocation trends of IOCs include a sustained reduction in exploration spending the past few years. Exploration is typically one of the first and easiest areas to reduce spending. The proliferation of shale and backlogged project queue (reduced FID activity) alleviates the need for wildcat exploration in the short-term.

Conversely, acquisitions have increased as a percentage of total spend the past few years. This includes bolt-on opportunities in shale, re-loading the portfolio with discovered but undeveloped resources and re-allocating assets toward the highest margin areas. Clearly the Chevron acquisition of Anadarko will sustain this trend of higher acquisitions into 2019.

IOCs have emerged into a uniquely advantaged landscape with excess free cash flow, E&P valuations that have languished, lack of competition in major global projects and excess capacity in US private equity. “The combination of these factors leads us to believe the M&A market will remain a healthy avenue to grow resources in the near-term,” Simmons Energy said.

“Peak oil demand concerns have somewhat diminished the focus on reserve life for some companies and investors. That said, we feel it’s still a healthy gauge of the industry’s future running room and indicator of M&A / exploration needs. With strong reserve replacement the past couple of years, reserve life for the group has inflected from a trough in 2016. While we expect ongoing reserve bookings, strong production growth near-term should work to mitigate the strong bookings witnessed the past couple of years,” Simmons Energy said.

Company outliers

ExxonMobil had strong organic reserve replacement of 316% last year. This was a function of US bookings (including Permian), Guyana and Brazil coupled with lackluster production growth in the year. Strong upward revisions in Canadian oil sands were partially offset by a downward revision at the Groningen field related to a Dutch government decision.

Equinor also had strong organic reserve replacement of 181% last year. The large majority of the increase came from revisions and additions in the Norwegian Continental Shelf (NCS). Many existing producing fields were revised upward due to pricing impacts, improved recovery and extended economic lives. The major new reserve additions were from Troll phase 3, Johan Sverdrup phase 2, and Vito field in the Gulf of Mexico.

Shell was a clear standout on the downside relative to peers with 67% replacement last year. The main driver was the Dutch government decision on Groningen, which removed around 600 MMboe. Excluding this, RRR would have been 110%. Another factor is Shell's portfolio approach to LNG where reserve cannot be booked without sales contracts in place (i.e. LNG Canada). Shell holds a portfolio of offshore assets without nearby comps/analogous projects thereby precluding large reserve bookings (i.e. Brazil).