The emergence of Mexico's upstream players

Ivan Sandrea

Sierra Oil & Gas

Mexico City

The future is not what it used to be for Mexico's energy industry. The energy sector is fully open and, in oil and gas, the Mexican regulators, Petroleos Mexicanos (Pemex), and the private sector must learn to work with each other and create value under a common and transparent set of rules for years to come. Prior to the reform, the regulatory experience in upstream was only with Pemex and in a closed environment whilst Mexico's private sector experienced the combination of specialist management and technical teams, access to capital, and governance did not exist.

Today more than 60 companies, from all sizes and nationalities, including more than 30 from Mexico, have entered the upstream sector since Round 1.1 was held in July 2015. More than 90 licenses-production-sharing contracts, royalty licenses, and Pemex farmouts-have been offered and 70 awarded, with a 75% success rate. The awarded licenses have received on average 4.6 bids and in some cases cash tie-breakers have been needed resulting in more than $950 million of cumulative signature bonuses.

Looking at seismic activity, private service companies are responsible for more than 45 new 2D and 3D surveys in the Mexican Gulf of Mexico and onshore at a cost of more than $2 billion. In drilling, the winners of licenses have committed more than 100 wells in the Mexican Western Pacific at a cost more than $1.5 billion with 25% of the wells offshore and 75% onshore. To guarantee all of this, it is estimated that the Mexican government has received more than $1.2 billion in letters of credit (LC) to guarantee work programs from the private sector, of which about $900 million is for offshore and $300 million is for onshore activity.

According to Mexico's Energy Ministry (SENER), more than $60 billion could be deployed in the coming years in Mexico. An impressive result given that just 3 years ago, Mexico was closed for private sector investment, the government did not have regulatory experience, oil prices have been at recent historical lows, and there were no private Mexican upstream players other than oil services companies and some international upstream companies with service contracts.

For companies to prequalify and thus participate, the Mexican regulator (CNH) has established, among others, well-defined financial and technical requirements for all operators and non-operators, and a highly transparent process. To be an operator, the financial requirement for offshore projects ranges from $600 million to $2 billion in shareholder's capital, and for onshore projects it starts at a minimum of $5 million. In addition, the technical prequalification for offshore operators includes a comprehensive set such as track record, assets, and production levels with 5 years of history.

For onshore operators, the minimum technical requirements allow newly formed companies interested in some types of projects to prequalify with the certification of the technical team, key health, safety, and environmental processes, and a risk-management system. The need to have a track record, assets, and production history is not a mandatory requirement for certain types of onshore projects, representing the only path for new Mexican players to begin the journey of operatorship.

Looking at non-operators, the financial requirements start at $250 million in the offshore and $2 million in onshore, and there are no technical requirements.

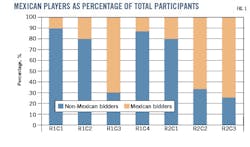

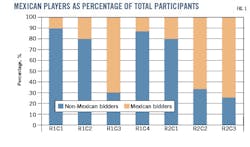

One of the core objectives of the reform is to develop the Mexican private oil and gas sector. Given the rules, no new company with less than 5 years old from Mexico (or the world) has been able to prequalify as operator in the offshore, but in the onshore 12 new companies have been able to prequalify, and win. In terms of non-operators, only five new companies from Mexico have participated in the offshore: Sierra Oil & Gas, CITLA, Diavaz, Petrobal, and Carso. Only one, Sierra, has participated in the deep water so far. However, there is no doubt that participation of Mexican players has been increasing (Fig. 1).

A logical first step for Mexico's newly formed upstream companies to play involved mixing local and international expertise, select ex-Pemex staff, consultants, and local graduates. Today is it a fact that most of the Mexican players are doing some if not all the above. In oil and gas, it is the norm to have multicultural and multidisciplinary teams, especially in technical and operations areas; even Saudi Aramco or Pemex are not excluded from this norm. Despite the logic, finding and maintaining the right talent and mix is one of the hardest parts for an oil company to get right. There is no doubt that the private sector and the government have much to do in the area of human capital development, but in Mexico we have a strong base from which to build from and many actions are already being taken.

In terms of access to capital, given the size, attractiveness, and openness of the Mexican economy, and fundamentally the new regulatory rules, Mexico offers a range of potential funding options to the newly formed companies, such as local pensions funds via development capital certificates (CKD) funded by local pension funds, multilateral development institutions, private capital, funding from publicly listed industrials and conglomerates, and international capital. However, historically the local market has not had the experience in providing risk capital to the upstream sector and in some cases the rules do not allow substantial institutional capital to participate in high-risk ventures, but this is already changing. Post energy reform, the market also has developed new options such as Fibra E (a form of master limited partnership as in the US) but is not suitable for upstream and more recently a SPAC (a special purpose vehicle listed in the Mexican Exchange), which has been used already for one new upstream player: Vista Oil & Gas.

Based on public data, the newly formed Mexican upstream companies that have participated in recent rounds have raised at least $1.8 billion from local and international institutional sources. But given that there are several private companies with licenses that have chosen not to disclose how much capital they have, the ultimate amount raised by the Mexican private sector so far is likely to be larger, perhaps $2.7 billion. This excludes the recent SPAC of Vista Oil & Gas, which raised $650 million and is expected to be active in Latin American rather than focused on Mexico.

Despite this success, for many newly formed Mexican companies, access to capital remains a major challenge, especially long-term institutional capital. It appears that only the most financially strong and sophisticated institutions are providing capital to the sector in this early stage. In addition to expertise, some aspects of the regulation such as administrative rescission clause, difficulty in permitting, social issues, high cost or lack of access to infrastructure, and uncertainty about estimating environmental liabilities among others are holding back institutional investors from being more active in the onshore whilst in the offshore the risk are technically higher in general.

Using a combination of publicly announced capital raised, number of bids, minimum work programs, and LC commitments, the most important and active Mexican new upstream players include the following companies: Sierra, Jaguar, CITLA, Diavaz, and Petrobal (Table 1). These companies represent most of the capital and activity so far. It is important to note that Diavaz has several other assets due to its participation in the pre-reform service contracts. Of these, only Sierra and CITLA have publicly available information regarding funding and ownership structure, and Sierra is the only one that has Mexican institutional capital from two CKDs, providing the opportunity to millions of Mexican workers to invest indirectly, and benefit directly. Sierra is also among the largest private equity-backed oil and gas companies in Latin America, according to market data.

In terms of activity, these Mexican companies have made 69 bids and won 24 licenses covering more than 10,000 sq km. More than 35 wells have been committed, of which about 10 will be offshore. No doubt that the onshore is receiving significant attention and capital from Mexican companies, but the harder-to-reach offshore is also an important part of the sector. Sierra, CITLA, and Petrobal are the only ones active in shallow water, whilst Sierra is the only one in deepwater so far. However, Sierra is the leader in total blocks offshore and acreage in the Sureste Super basin. And today we are proud to say that, together with our partners, we have also made the first important discovery-Zama-by the private sector since 1938.

The newly formed Mexican upstream companies now have a visible footprint in Mexico's new energy map. Based on CNH data, contracts held by Mexican companies have 183 million boe of 2P reserves, more than 2,000 boe/d of oil and gas production, and 3.88 billion boe of prospective production-and more if one includes "migration" assets. In addition, the Zama discovery holds more than 2 billion bbl OOIP and Sierra participates with 40% working interest as well in two other blocks-5 and 11-that today form a part of the Zama play.

As a sector, this important market position comes with demanding commitments and responsibilities to the government, society, investors, and in the millions of pensioners that are participating in the sector via CKDs and public markets. In fact, for some states, the new Mexican upstream companies have the potential to contribute the most to the long-term economic success of the state, the reform, and ultimately of Mexico growing economy. Equally, the Mexican government and political parties, would do well by continuing to recognize in the future the risk taken, often with partial or incomplete regulation, and long-term commitment that is being made by the private sector. The interest of the private sector and the state are clearly aligned.

The author

Ivan Sandrea, founding member and chief executive officer of Sierra Oil & Gas, has more than 20 years of executive and technical experience in oil and gas and has been active in Mexico for more than a decade. Prior to Sierra, Sandrea was co-head of the global oil and gas emerging markets practice for EY, president of Energy Intelligence Group, vice-president of upstream strategy and business development at Statoil, board member of Pan Andean Resources, officer at the Organization of Petroleum Exporting Countries, investment banker at Merrill Lynch, and exploration/operations geologist at BP PLC. He is an active member of the Oxford Institute for Energy Studies, and the Energy Policy Research Foundation in Washington, DC. Sandrea's academic activities include co-founder and guest lecturer at the Executive Energy MBA program at Wirtschaftsuniversitat in Vienna, lecturer at the Executive Energy program at Mexico's ITAM University, as well as authorship of over 15 leading research papers. He holds a BSc in Geology from Baylor University, an MSc and MBA from Edinburgh University, and attended the Berkeley Executive Leadership Program in Stanford.