EIA cuts 2016 crude oil price forecasts in latest STEO

The US Energy Information Administration has sharply cut its crude oil price forecasts through 2016 in its Short-Term Energy Outlook for January, which is the first to include a forecast for 2017. The cut is because of the continuing threat of a prolonged oversupply of crude as well as global inventory builds.

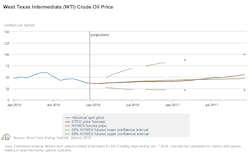

Forecast Brent prices in 2016 average $40/bbl compared with $56/bbl projected in last month’s STEO (OGJ Online, Dec. 9, 2015). EIA expects that the largest inventory builds will occur in this year’s first half, keeping Brent prices below $40/bbl through April. Brent crude prices are forecast to average $50/bbl in 2017, with upward price pressure concentrated in the latter part that year.

West Texas Intermediate crude oil prices are forecast to average $2/bbl lower than Brent in 2016 and $3/bbl lower in 2017. EIA had previously assumed the 2016 WTI discount to be $5/bbl. The lower forecast WTI discount to Brent is based on the relative storage availability in the US compared with other regions that encourages placing crude oil in the US market in a period of global oversupply.

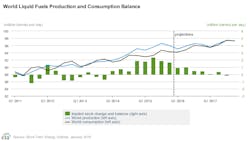

EIA forecasts that global oil inventories will rise by an additional 700,000 b/d in 2016 before the global oil market becomes relatively balanced in 2017. The first draw on global oil inventories in 15 consecutive quarters is expected in third-quarter 2017, EIA said.

Global oil market

In the most recent STEO, EIA estimates global consumption of petroleum and other liquid fuels rose 1.4 million b/d in 2015, averaging 93.8 million b/d for the year. EIA expects global oil consumption to rise 1.4 million b/d in both 2016 and 2017. Driven by an increase in US consumption, consumption by members of the Organization for Economic Cooperation and Development is expected to continue rising in 2016 and 2017 by respective rates of 300,000 b/d and 400,000 b/d, after a growth of 600,000 b/d in 2015.

EIA estimates that petroleum and other liquid fuels production in countries outside of the Organization of Petroleum Exporting Countries rose 1.3 million b/d in 2015, led by growth in North America. Non-OPEC production is forecast to decline 600,000 b/d in 2016, which would be the first decline since 2008. Most of the forecast decline in 2016 is expected to be in the US. Among other non-OPEC producers, the largest declines are to be in the North Sea and Russia. In 2017, non-OPEC production is forecast to decrease by an additional 100,000 b/d.

As of this STEO, EIA includes Indonesia’s crude oil and other liquids production in the OPEC total for both history and the forecast. According to EIA data, OPEC crude oil production averaged 31.6 million b/d in 2015, an increase of 900,000 b/d from 2014, led by Iraq and Saudi Arabia. OPEC crude oil production is forecast to rise 500,000 b/d in 2016, with Iran expected to increase production once international sanctions are lifted. EIA forecasts OPEC crude oil production to increase 600,000 b/d in 2017, with Iran accounting for most of the increase.

Iran’s crude oil production is forecast to rise 300,000 b/d in 2016 and 500,000 b/d in 2017, EIA said.

US oil market

Stimulated by continued growth in employment and the economy and lower petroleum product prices, total US liquid fuels consumption is forecast to rise 270,000 b/d, or 1.4%, in 2015, compared with a rise of 140,000 b/d in 2014. In 2016, total liquid fuels consumption is forecast to increase 160,000 b/d, or 0.8%, from the 2015 level. In 2017, total US consumption is projected to rise by an additional 270,000 b/d.

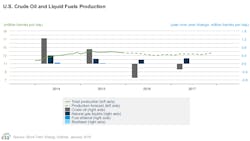

US crude oil production is projected to decrease from an average of 9.4 million b/d in 2015 to 8.7 million b/d in 2016 and to 8.5 million b/d in 2017 because of an extended decline in Lower 48 onshore production that is partially offset by growing production in the Gulf of Mexico.

“The expectation of reduced capital flows in 2016 and 2017 has prompted many companies to scale-back investment programs, deferring major new undertakings until a sustained price recovery occurs. The prospect of higher interest rates and tougher lending conditions will likely limit the availability of capital for many smaller producers, giving rise to distressed asset sales and consolidation of acreage holdings by more financially sound firms,” EIA said.