EIA: Latest STEO shows resilient oil output delaying market rebalance

In its latest Short-Term Energy Outlook, the US Energy Information Administration forecasts the price of Brent crude oil to average $34/bbl in 2016 compared with an earlier forecast of $37/bbl. In 2017, EIA forecasts Brent to average $40/bbl compared with $50/bbl in last month’s forecast.

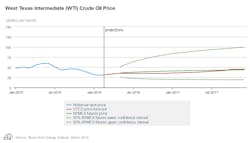

EIA expects the West Texas Intermediate crude price to average the same as Brent in both years.

“The lower forecast prices reflect oil production that has been more resilient than expected in a low-price environment and lower expectations for forecast oil demand growth,” EIA said.

Global liquids inventories are forecast to increase by an annual average of 1.6 million b/d in 2016 and by an additional 0.6 million b/d in 2017, according to the outlook in March.

“These inventory build are larger than previously expected, delaying the rebalancing of the oil market and contributing to lower forecast oil prices,” EIA said.

Compared with last month’s STEO, EIA has revised forecast supply growth higher for 2016 and revised forecast demand growth lower for both 2016 and 2017.

In this month’s STEO, EIA expects global oil consumption to grow by 1.1 million b/d in 2016 and by 1.2 million b/d in 2017, compared with a growth of 1.3 million b/d in 2015. Forecast consumption growth is 100,000 b/d and 200,000 b/d lower in 2016 and 2017, respectively, than in last month’s STEO because of lower expected growth in real gross domestic production (GDP) for the world.

Crude oil production from the Organization of the Petroleum Exporting Countries is forecast to increase by 700,000 b/d in 2016 and by 400,000 b/d in 2017, with Iran accounting for most of the increase. EIA estimates that OPEC crude oil production averaged 31.6 million b/d in 2014.

“The forecast does not assume a collaborative production cut among OPEC members and other major producers in the forecast period, as major OPEC producers continue the strategy to maintain market share,” EIA said.

Non-OPEC oil supply is forecast to decline by 400,000 b/d in 2016 and by 500,000 b/d in 2017, after an increase of 1.5 million b/d in 2015.

Changes in non-OPEC production are driven by changes in US tight oil production. However, increases in production of hydrocarbon gas liquids from natural gas plants and in crude oil production from the Gulf of Mexico partially offset lower tight oil production.

According to this month’s STEO, outside of the US, forecast non-OPEC production increases by 200,000 b/d in 2016 and then declines by 300,000 b/d in 2017. In last month’s STEO, EIA expected non-OPEC production to decline by 100,000 b/d in 2016 and by 300,000 b/d in 2017.

EIA explained, incoming data indicate production in these countries has also been more resilient than expected in a low oil price environment, which has prompted EIA to push forecast non-OPEC declines outside the US into 2017.

“Production is relatively resilient through the forecast period because of investments committed to projects when oil prices were higher. Although oil companies have reduced investments, most of the cuts have been in capital budgets that largely affect production levels beyond 2017. Additionally, recent strength in the US dollar and cost reductions have moderated the effects of declining oil revenues on production in some countries,” EIA said, citing Russia as one example of production exceeding expectations.